Frequency and Trend Selection

Source:vignettes/TK06_Automatic_Frequency_And_Trend_Selection.Rmd

TK06_Automatic_Frequency_And_Trend_Selection.RmdFrequency and trend cycles are used in many time

series applications including Seasonal ARIMA (SARIMA) forecasting and

STL Decomposition. timetk includes functionality for

Automatic Frequency and Trend Selection. These tools

use only the the timestamp information to make logical guesses about the

frequency and trend.

Data

Daily Irregular Data

The daily stock prices of Facebook from 2013 to 2016. Note that trading days only occur on “business days” (non-weekends and non-business-holidays).

## # A tibble: 1,008 × 8

## symbol date open high low close volume adjusted

## <chr> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 FB 2013-01-02 27.4 28.2 27.4 28 69846400 28

## 2 FB 2013-01-03 27.9 28.5 27.6 27.8 63140600 27.8

## 3 FB 2013-01-04 28.0 28.9 27.8 28.8 72715400 28.8

## 4 FB 2013-01-07 28.7 29.8 28.6 29.4 83781800 29.4

## 5 FB 2013-01-08 29.5 29.6 28.9 29.1 45871300 29.1

## 6 FB 2013-01-09 29.7 30.6 29.5 30.6 104787700 30.6

## 7 FB 2013-01-10 30.6 31.5 30.3 31.3 95316400 31.3

## 8 FB 2013-01-11 31.3 32.0 31.1 31.7 89598000 31.7

## 9 FB 2013-01-14 32.1 32.2 30.6 31.0 98892800 31.0

## 10 FB 2013-01-15 30.6 31.7 29.9 30.1 173242600 30.1

## # ℹ 998 more rowsSub-Daily Data

Taylor’s Energy Demand data at a 30-minute timestamp interval.

taylor_30_min## # A tibble: 4,032 × 2

## date value

## <dttm> <dbl>

## 1 2000-06-05 00:00:00 22262

## 2 2000-06-05 00:30:00 21756

## 3 2000-06-05 01:00:00 22247

## 4 2000-06-05 01:30:00 22759

## 5 2000-06-05 02:00:00 22549

## 6 2000-06-05 02:30:00 22313

## 7 2000-06-05 03:00:00 22128

## 8 2000-06-05 03:30:00 21860

## 9 2000-06-05 04:00:00 21751

## 10 2000-06-05 04:30:00 21336

## # ℹ 4,022 more rowsApplications

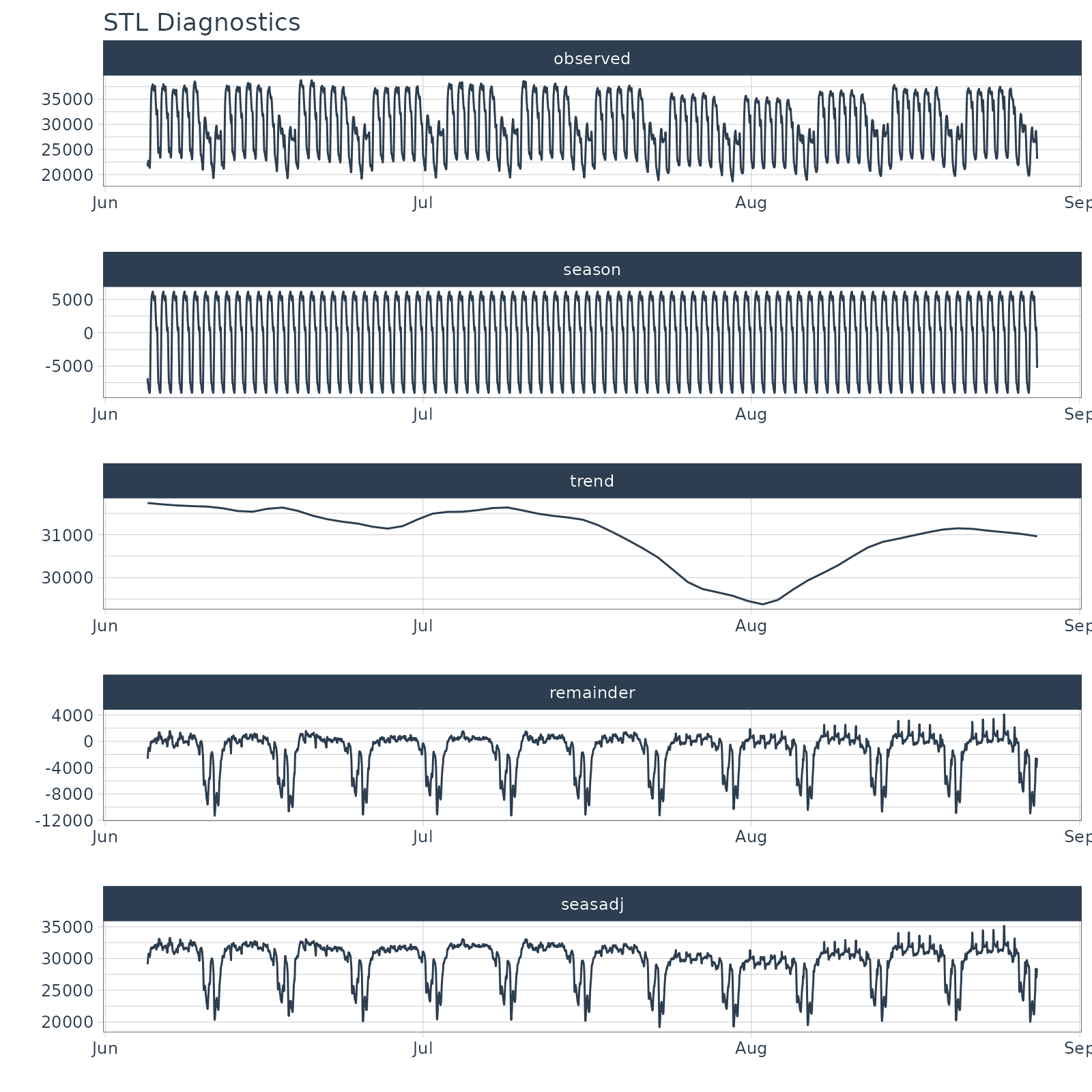

An example of where automatic frequency detection occurs is in the

plot_stl_diagnostics() function.

taylor_30_min %>%

plot_stl_diagnostics(date, value,

.frequency = "auto", .trend = "auto",

.interactive = FALSE)## frequency = 48 observations per 1 day## trend = 672 observations per 14 days

Automatic Frequency & Trend Selection

Specifying a Frequency or Trend

The period argument has three basic options for

returning a frequency. Options include:

- “auto”: A target frequency is determined using a pre-defined Time Scale Template (see below).

- time-based duration: (e.g. “7 days” or “2 quarters” per cycle)

- numeric number of observations: (e.g. 5 for 5 observations per cycle)

Frequency

A frequency is loosely defined as the number of observations that comprise a cycle in a data set.

Using tk_get_frequency(), we can pick a number of

observations that will roughly define a frequency for the series.

Daily Irregular Data

Because FB_tbl is irregular (weekends and holidays are

not present), the frequency selected is weekly but each week is only

5-days typically. So 5 is selected.

FB_tbl %>% tk_index() %>% tk_get_frequency(period = "auto")## frequency = 5 observations per 1 week## [1] 5Sub-Daily Data

This works as well for a sub-daily time series. Here we’ll use

taylor_30_min for a 30-minute timestamp series. The

frequency selected is 48 because there are 48 timestamps (observations)

in 1 day for the 30-minute cycle.

taylor_30_min %>% tk_index() %>% tk_get_frequency("1 day")## frequency = 48 observations per 1 day## [1] 48Trend

The trend is loosely defined as time span that can be aggregated across to visualize the central tendency of the data.

Using tk_get_trend(), we can pick a number of

observations that will help describe a trend for the data.

Daily Irregular Data

Because FB_tbl is irregular (weekends and holidays are

not present), the trend selected is 3 months but each week is only

5-days typically. So 64 observations is selected.

FB_tbl %>% tk_index() %>% tk_get_trend(period = "auto")## trend = 64 observations per 3 months## [1] 64Sub-Daily Data

A 14-day (2 week) interval is selected for the “30-minute” interval data.

taylor_30_min %>% tk_index() %>% tk_get_trend("auto")## trend = 672 observations per 14 days## [1] 672Time Scale Template

A Time-Scale Template is used to get and

set the time scale template, which is used by

tk_get_frequency() and tk_get_trend() when

period = "auto".

The predefined template is stored in a function

tk_time_scale_template(). This is the default used by

timetk.

Accessing the Default Template

You can access the current template with

get_tk_time_scale_template().

## # A tibble: 8 × 3

## time_scale frequency trend

## <chr> <chr> <chr>

## 1 second 1 hour 12 hours

## 2 minute 1 day 14 days

## 3 hour 1 day 1 month

## 4 day 1 week 3 months

## 5 week 1 quarter 1 year

## 6 month 1 year 5 years

## 7 quarter 1 year 10 years

## 8 year 5 years 30 yearsChanging the Default Template

You can modify the current template with

set_tk_time_scale_template().

Learning More

My Talk on High-Performance Time Series Forecasting

Time series is changing. Businesses now need 10,000+ time series forecasts every day.

High-Performance Forecasting Systems will save companies MILLIONS of dollars. Imagine what will happen to your career if you can provide your organization a “High-Performance Time Series Forecasting System” (HPTSF System).

I teach how to build a HPTFS System in my High-Performance Time Series Forecasting Course. If interested in learning Scalable High-Performance Forecasting Strategies then take my course. You will learn:

- Time Series Machine Learning (cutting-edge) with

Modeltime- 30+ Models (Prophet, ARIMA, XGBoost, Random Forest, & many more) - NEW - Deep Learning with

GluonTS(Competition Winners) - Time Series Preprocessing, Noise Reduction, & Anomaly Detection

- Feature engineering using lagged variables & external regressors

- Hyperparameter Tuning

- Time series cross-validation

- Ensembling Multiple Machine Learning & Univariate Modeling Techniques (Competition Winner)

- Scalable Forecasting - Forecast 1000+ time series in parallel

- and more.