Code

import pandas as pd

import numpy as np

import pytimetk as tk

from sklearn.ensemble import RandomForestRegressorTimetk enables you to generate features from the time column of your data very easily. This tutorial showcases how easy it is to perform time series forecasting with pytimetk. The specific methods we will be using are:

tk.augment_timeseries_signature(): Add 29 time series features to a DataFrame.tk.augment_lags(): Adds past values of a feature as a predictortk.augment_rolling(): Calculates rolling window aggregates of a feature.tk.plot_timeseries(): Creates time series plots using different plotting engines such as Plotnine, Matplotlib, and Plotly.tk.future_frame(): Extend a DataFrame or GroupBy object with future dates.Load the following packages before proceeding with this tutorial.

import pandas as pd

import numpy as np

import pytimetk as tk

from sklearn.ensemble import RandomForestRegressorThe tutorial is divided into three parts: We will first have a look at the Walmart dataset and perform some preprocessing. Secondly, we will create models based on different features, and see how the time features can be useful. Finally, we will solve the task of time series forecasting, using the features from augment_timeseries_signature, augment_lags, and augment_rolling, to predict future sales.

The first thing we want to do is to load the dataset. It is a subset of the Walmart sales prediction Kaggle competition. You can get more insights about the dataset by following this link: walmart_sales_weekly. The most important thing to know about the dataset is that you are provided with some features like the fuel price or whether the week contains holidays and you are expected to predict the weekly sales column for 7 different departments of a given store. Of course, you also have the date for each week, and that is what we can leverage to create additional features.

Let us start by loading the dataset and cleaning it. Note that we also removed some columns due to * duplication of data * 0 variance * No future data available in current dataset.

# We start by loading the dataset

# /walmart_sales_weekly.html

dset = tk.load_dataset('walmart_sales_weekly', parse_dates = ['Date'])

dset = dset.drop(columns=[

'id', # This column can be removed as it is equivalent to 'Dept'

'Store', # This column has only one possible value

'Type', # This column has only one possible value

'Size', # This column has only one possible value

'MarkDown1', 'MarkDown2', 'MarkDown3', 'MarkDown4', 'MarkDown5',

'IsHoliday', 'Temperature', 'Fuel_Price', 'CPI',

'Unemployment'])

dset.head()| Dept | Date | Weekly_Sales | |

|---|---|---|---|

| 0 | 1 | 2010-02-05 | 24924.50 |

| 1 | 1 | 2010-02-12 | 46039.49 |

| 2 | 1 | 2010-02-19 | 41595.55 |

| 3 | 1 | 2010-02-26 | 19403.54 |

| 4 | 1 | 2010-03-05 | 21827.90 |

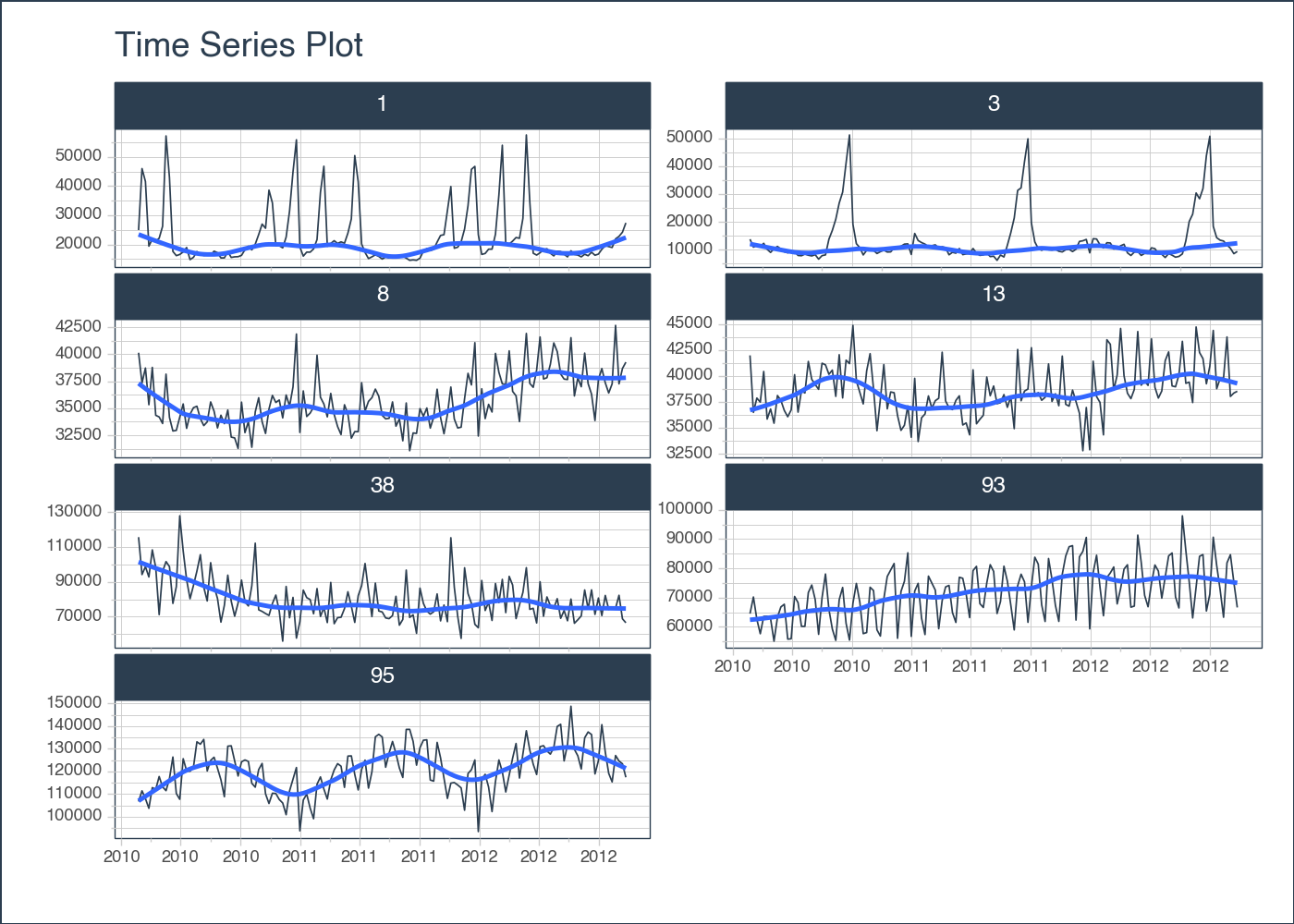

We can plot the values of each department to get an idea of how the data looks like. Using the plot_timeseries method with a groupby allows us to create multiple plots by group.

tk.plot_timeseries()

help(tk.plot_timeseries) to review additional helpful documentation.sales_df = dset

fig = sales_df.groupby('Dept').plot_timeseries(

date_column='Date',

value_column='Weekly_Sales',

facet_ncol = 2,

x_axis_date_labels = "%Y",

engine = 'plotly')

figfig = sales_df.groupby('Dept').plot_timeseries(

date_column='Date',

value_column='Weekly_Sales',

facet_ncol = 2,

x_axis_date_labels = "%Y",

engine = 'plotnine')

fig

<Figure Size: (700 x 500)>tk.future_frameWhen building machine learning models, we need to setup our dataframe to hold information about the future. This is the dataframe that will get passed to our model.predict() call. This is made easy with tk.future_frame().

tk.future_frame()

Curious about the various options it provides?

help(tk.future_frame) to review additional helpful documentation. And explore the plethora of possibilities!Notice this function adds 5 weeks to our dateset for each department and fills in weekly sales with nulls. Previously our max date was 2012-10-26.

print(sales_df.groupby('Dept').Date.max())Dept

1 2012-10-26

3 2012-10-26

8 2012-10-26

13 2012-10-26

38 2012-10-26

93 2012-10-26

95 2012-10-26

Name: Date, dtype: datetime64[ns]After applying our future frame, we can now see values 5 weeks in the future, and our dataframe has been extended to 2012-11-30 for all groups.

sales_df_with_futureframe = sales_df \

.groupby('Dept') \

.future_frame(

date_column = 'Date',

length_out = 5

)sales_df_with_futureframe.groupby('Dept').Date.max()Dept

1 2012-11-30

3 2012-11-30

8 2012-11-30

13 2012-11-30

38 2012-11-30

93 2012-11-30

95 2012-11-30

Name: Date, dtype: datetime64[ns]tk.augment_timeseries_signatureMachine Learning models generally cannot process raw date objects directly. Moreover, they lack an inherent understanding of the passage of time. This means that, without specific features, a model can’t differentiate between a January observation and a June one. To bridge this gap, the tk.augment_timeseries_signature function is invaluable. It generates 29 distinct date-oriented features suitable for model inputs.

tk.augment_timeseries_signature(),tk.augment_lags(), tk.augment_rolling()

help(tk.augment_timeseries_signature) help(tk.augment_lags) help(tk.augment_rolling) to review additional helpful documentation.It’s crucial, however, to align these features with the granularity of your dataset. Given the weekly granularity of the Walmart dataset, any date attributes finer than ‘week’ should be excluded for relevance and efficiency.

sales_df_dates = sales_df_with_futureframe.augment_timeseries_signature(date_column = 'Date')

sales_df_dates.head(10)| Dept | Date | Weekly_Sales | Date_index_num | Date_year | Date_year_iso | Date_yearstart | Date_yearend | Date_leapyear | Date_half | ... | Date_mday | Date_qday | Date_yday | Date_weekend | Date_hour | Date_minute | Date_second | Date_msecond | Date_nsecond | Date_am_pm | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 1 | 2010-02-05 | 24924.50 | 1265328000 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 5 | 36 | 36 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 1 | 1 | 2010-02-12 | 46039.49 | 1265932800 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 12 | 43 | 43 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 2 | 1 | 2010-02-19 | 41595.55 | 1266537600 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 19 | 50 | 50 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 3 | 1 | 2010-02-26 | 19403.54 | 1267142400 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 26 | 57 | 57 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 4 | 1 | 2010-03-05 | 21827.90 | 1267747200 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 5 | 64 | 64 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 5 | 1 | 2010-03-12 | 21043.39 | 1268352000 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 12 | 71 | 71 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 6 | 1 | 2010-03-19 | 22136.64 | 1268956800 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 19 | 78 | 78 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 7 | 1 | 2010-03-26 | 26229.21 | 1269561600 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 26 | 85 | 85 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 8 | 1 | 2010-04-02 | 57258.43 | 1270166400 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 2 | 2 | 92 | 0 | 0 | 0 | 0 | 0 | 0 | am |

| 9 | 1 | 2010-04-09 | 42960.91 | 1270771200 | 2010 | 2010 | 0 | 0 | 0 | 1 | ... | 9 | 9 | 99 | 0 | 0 | 0 | 0 | 0 | 0 | am |

10 rows × 32 columns

Upon reviewing the generated features, it’s evident that certain attributes don’t align with the granularity of our dataset. For optimal results, features exhibiting no variance—like “Date_hour” due to the weekly nature of our data—should be omitted. We also spot redundant features, such as “Date_Month” and “Date_month_lbl”; both convey month information, albeit in different formats. To enhance clarity and computational efficiency, we’ll refine our dataset to include only the most relevant columns.

Additionally, we’ve eliminated certain categorical columns, which, although compatible with models like LightGBM and Catboost, demand extra processing for many tree-based ML models. While 1-hot encoding is a popular method for managing categorical data, it’s not typically recommended for date attributes. Instead, leveraging numeric date features directly, combined with the integration of Fourier features, can effectively capture cyclical patterns.

sales_df_dates.glimpse()<class 'pandas.core.frame.DataFrame'>: 1036 rows of 32 columns

Dept: int64 [1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, ...

Date: datetime64[ns] [Timestamp('2010-02-05 00:00:00'), ...

Weekly_Sales: float64 [24924.5, 46039.49, 41595.55, 1940 ...

Date_index_num: int64 [1265328000, 1265932800, 126653760 ...

Date_year: int64 [2010, 2010, 2010, 2010, 2010, 201 ...

Date_year_iso: UInt32 [2010, 2010, 2010, 2010, 2010, 201 ...

Date_yearstart: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_yearend: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_leapyear: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_half: int64 [1, 1, 1, 1, 1, 1, 1, 1, 1, 1, 1, ...

Date_quarter: int64 [1, 1, 1, 1, 1, 1, 1, 1, 2, 2, 2, ...

Date_quarteryear: object ['2010Q1', '2010Q1', '2010Q1', '20 ...

Date_quarterstart: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_quarterend: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_month: int64 [2, 2, 2, 2, 3, 3, 3, 3, 4, 4, 4, ...

Date_month_lbl: object ['February', 'February', 'February ...

Date_monthstart: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_monthend: uint8 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_yweek: UInt32 [5, 6, 7, 8, 9, 10, 11, 12, 13, 14 ...

Date_mweek: int64 [1, 2, 3, 4, 1, 2, 3, 4, 1, 2, 3, ...

Date_wday: int64 [5, 5, 5, 5, 5, 5, 5, 5, 5, 5, 5, ...

Date_wday_lbl: object ['Friday', 'Friday', 'Friday', 'Fr ...

Date_mday: int64 [5, 12, 19, 26, 5, 12, 19, 26, 2, ...

Date_qday: int64 [36, 43, 50, 57, 64, 71, 78, 85, 2 ...

Date_yday: int64 [36, 43, 50, 57, 64, 71, 78, 85, 9 ...

Date_weekend: int64 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_hour: int64 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_minute: int64 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_second: int64 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_msecond: int64 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_nsecond: int64 [0, 0, 0, 0, 0, 0, 0, 0, 0, 0, 0, ...

Date_am_pm: object ['am', 'am', 'am', 'am', 'am', 'am ...sales_df_dates = sales_df_dates[[

'Date'

,'Dept'

, 'Weekly_Sales'

, 'Date_year'

, 'Date_month'

, 'Date_yweek'

, 'Date_mweek'

]]

sales_df_dates.tail(10)| Date | Dept | Weekly_Sales | Date_year | Date_month | Date_yweek | Date_mweek | |

|---|---|---|---|---|---|---|---|

| 1026 | 2012-11-02 | 93 | NaN | 2012 | 11 | 44 | 1 |

| 1027 | 2012-11-09 | 93 | NaN | 2012 | 11 | 45 | 2 |

| 1028 | 2012-11-16 | 93 | NaN | 2012 | 11 | 46 | 3 |

| 1029 | 2012-11-23 | 93 | NaN | 2012 | 11 | 47 | 4 |

| 1030 | 2012-11-30 | 93 | NaN | 2012 | 11 | 48 | 5 |

| 1031 | 2012-11-02 | 95 | NaN | 2012 | 11 | 44 | 1 |

| 1032 | 2012-11-09 | 95 | NaN | 2012 | 11 | 45 | 2 |

| 1033 | 2012-11-16 | 95 | NaN | 2012 | 11 | 46 | 3 |

| 1034 | 2012-11-23 | 95 | NaN | 2012 | 11 | 47 | 4 |

| 1035 | 2012-11-30 | 95 | NaN | 2012 | 11 | 48 | 5 |

tk.augment_lagsAs previously noted, it’s important to recognize that machine learning models lack inherent awareness of time, a vital consideration in time series modeling. Furthermore, these models operate under the assumption that each row is independent, meaning that the information from last month’s weekly sales is not inherently integrated into the prediction of next month’s sales target. To address this limitation, we incorporate additional features, such as lags, into the models to capture temporal dependencies. You can easily achieve this by employing the tk.augment_lags function.

df_with_lags = sales_df_dates \

.groupby('Dept') \

.augment_lags(

date_column = 'Date',

value_column = 'Weekly_Sales',

lags = [5,6,7,8,9]

)

df_with_lags.head(5)| Date | Dept | Weekly_Sales | Date_year | Date_month | Date_yweek | Date_mweek | Weekly_Sales_lag_5 | Weekly_Sales_lag_6 | Weekly_Sales_lag_7 | Weekly_Sales_lag_8 | Weekly_Sales_lag_9 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2010-02-05 | 1 | 24924.50 | 2010 | 2 | 5 | 1 | NaN | NaN | NaN | NaN | NaN |

| 1 | 2010-02-12 | 1 | 46039.49 | 2010 | 2 | 6 | 2 | NaN | NaN | NaN | NaN | NaN |

| 2 | 2010-02-19 | 1 | 41595.55 | 2010 | 2 | 7 | 3 | NaN | NaN | NaN | NaN | NaN |

| 3 | 2010-02-26 | 1 | 19403.54 | 2010 | 2 | 8 | 4 | NaN | NaN | NaN | NaN | NaN |

| 4 | 2010-03-05 | 1 | 21827.90 | 2010 | 3 | 9 | 1 | NaN | NaN | NaN | NaN | NaN |

tk.augment_rollingAnother pivotal aspect of time series analysis involves the utilization of rolling lags. These operations facilitate computations within a moving time window, enabling the use of functions such as “mean” and “std” on these rolling windows. This can be achieved by invoking the tk.augment_rolling() function on grouped time series data. To execute this, we will initially gather all columns containing ‘lag’ in their names. We then apply this function to the lag values, as opposed to the weekly sales, since we lack future weekly sales data. By applying these functions to the lag values, we ensure the prevention of data leakage and maintain the adaptability of our method to unforeseen future data.

lag_columns = [col for col in df_with_lags.columns if 'lag' in col]

df_with_rolling = df_with_lags \

.groupby('Dept') \

.augment_rolling(

date_column = 'Date',

value_column = lag_columns,

window = 4,

window_func = 'mean',

threads = 1 # Change to -1 to use all available cores

)

df_with_rolling[df_with_rolling.Dept ==1].head(10)| Date | Dept | Weekly_Sales | Date_year | Date_month | Date_yweek | Date_mweek | Weekly_Sales_lag_5 | Weekly_Sales_lag_6 | Weekly_Sales_lag_7 | Weekly_Sales_lag_8 | Weekly_Sales_lag_9 | Weekly_Sales_lag_5_rolling_mean_win_4 | Weekly_Sales_lag_6_rolling_mean_win_4 | Weekly_Sales_lag_7_rolling_mean_win_4 | Weekly_Sales_lag_8_rolling_mean_win_4 | Weekly_Sales_lag_9_rolling_mean_win_4 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2010-02-05 | 1 | 24924.50 | 2010 | 2 | 5 | 1 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 0 | 2010-02-05 | 1 | 24924.50 | 2010 | 2 | 5 | 1 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 0 | 2010-02-05 | 1 | 24924.50 | 2010 | 2 | 5 | 1 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 0 | 2010-02-05 | 1 | 24924.50 | 2010 | 2 | 5 | 1 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 0 | 2010-02-05 | 1 | 24924.50 | 2010 | 2 | 5 | 1 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 2010-02-12 | 1 | 46039.49 | 2010 | 2 | 6 | 2 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 2010-02-12 | 1 | 46039.49 | 2010 | 2 | 6 | 2 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 2010-02-12 | 1 | 46039.49 | 2010 | 2 | 6 | 2 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 2010-02-12 | 1 | 46039.49 | 2010 | 2 | 6 | 2 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 1 | 2010-02-12 | 1 | 46039.49 | 2010 | 2 | 6 | 2 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

Notice when we add lag values to our dataframe, this creates several NA values. This is because when using lags, there will be some data that is not available early in our dataset.Thus as a result, NA values are introduced.

To simplify and clean up the process, we will remove these rows entirely since we already extracted some meaningful information from them (ie. lags, rolling lags).

all_lag_columns = [col for col in df_with_rolling.columns if 'lag' in col]

df_no_nas = df_with_rolling \

.dropna(subset=all_lag_columns, inplace=False)

df_no_nas.head()| Date | Dept | Weekly_Sales | Date_year | Date_month | Date_yweek | Date_mweek | Weekly_Sales_lag_5 | Weekly_Sales_lag_6 | Weekly_Sales_lag_7 | Weekly_Sales_lag_8 | Weekly_Sales_lag_9 | Weekly_Sales_lag_5_rolling_mean_win_4 | Weekly_Sales_lag_6_rolling_mean_win_4 | Weekly_Sales_lag_7_rolling_mean_win_4 | Weekly_Sales_lag_8_rolling_mean_win_4 | Weekly_Sales_lag_9_rolling_mean_win_4 | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.9 | 19403.54 | 22809.285 | 21102.8675 | 25967.595 | 32216.62 | 32990.77 |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.9 | 19403.54 | 22809.285 | 21102.8675 | 25967.595 | 32216.62 | 32990.77 |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.9 | 19403.54 | 22809.285 | 21102.8675 | 25967.595 | 32216.62 | 32990.77 |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.9 | 19403.54 | 22809.285 | 21102.8675 | 25967.595 | 32216.62 | 32990.77 |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.9 | 19403.54 | 22809.285 | 21102.8675 | 25967.595 | 32216.62 | 32990.77 |

We can call tk.glimpse() again to quickly see what features we still have available.

df_no_nas.glimpse()<class 'pandas.core.frame.DataFrame'>: 4760 rows of 17 columns

Date: datetime64[ns] [Timestamp('20 ...

Dept: int64 [1, 1, 1, 1, 1 ...

Weekly_Sales: float64 [16555.11, 165 ...

Date_year: int64 [2010, 2010, 2 ...

Date_month: int64 [4, 4, 4, 4, 4 ...

Date_yweek: UInt32 [17, 17, 17, 1 ...

Date_mweek: int64 [5, 5, 5, 5, 5 ...

Weekly_Sales_lag_5: float64 [26229.21, 262 ...

Weekly_Sales_lag_6: float64 [22136.64, 221 ...

Weekly_Sales_lag_7: float64 [21043.39, 210 ...

Weekly_Sales_lag_8: float64 [21827.9, 2182 ...

Weekly_Sales_lag_9: float64 [19403.54, 194 ...

Weekly_Sales_lag_5_rolling_mean_win_4: float64 [22809.285, 22 ...

Weekly_Sales_lag_6_rolling_mean_win_4: float64 [21102.8675, 2 ...

Weekly_Sales_lag_7_rolling_mean_win_4: float64 [25967.595, 25 ...

Weekly_Sales_lag_8_rolling_mean_win_4: float64 [32216.6200000 ...

Weekly_Sales_lag_9_rolling_mean_win_4: float64 [32990.7700000 ...Now that we have our training set built, we can start to train our regressor. To do so, let’s first do some model cleanup.

Split our data in to train and future sets.

future = df_no_nas[df_no_nas.Weekly_Sales.isnull()]

train = df_no_nas[df_no_nas.Weekly_Sales.notnull()]We still have a datetime object in our training data. We will need to remove that before passing to our regressor. Let’s subset our column to just the features we want to use for modeling.

train_columns = [

'Dept'

, 'Date_year'

, 'Date_month'

, 'Date_yweek'

, 'Date_mweek'

, 'Weekly_Sales_lag_5'

, 'Weekly_Sales_lag_6'

, 'Weekly_Sales_lag_7'

, 'Weekly_Sales_lag_8'

, 'Weekly_Sales_lag_5_rolling_mean_win_4'

, 'Weekly_Sales_lag_6_rolling_mean_win_4'

, 'Weekly_Sales_lag_7_rolling_mean_win_4'

, 'Weekly_Sales_lag_8_rolling_mean_win_4'

]

X = train[train_columns]

y = train[['Weekly_Sales']]

model = RandomForestRegressor(random_state=123)

model = model.fit(X, y)Now that we have a trained model, we can pass in our future frame to predict weekly sales.

predicted_values = model.predict(future[train_columns])

future['y_pred'] = predicted_values

future.head(10)| Date | Dept | Weekly_Sales | Date_year | Date_month | Date_yweek | Date_mweek | Weekly_Sales_lag_5 | Weekly_Sales_lag_6 | Weekly_Sales_lag_7 | Weekly_Sales_lag_8 | Weekly_Sales_lag_9 | Weekly_Sales_lag_5_rolling_mean_win_4 | Weekly_Sales_lag_6_rolling_mean_win_4 | Weekly_Sales_lag_7_rolling_mean_win_4 | Weekly_Sales_lag_8_rolling_mean_win_4 | Weekly_Sales_lag_9_rolling_mean_win_4 | y_pred | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 1001 | 2012-11-02 | 1 | NaN | 2012 | 11 | 44 | 1 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 16680.24 | 19034.475 | 18467.5825 | 17726.3075 | 17154.9275 | 16604.3150 | 26627.7378 |

| 1001 | 2012-11-02 | 1 | NaN | 2012 | 11 | 44 | 1 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 16680.24 | 19034.475 | 18467.5825 | 17726.3075 | 17154.9275 | 16604.3150 | 26627.7378 |

| 1001 | 2012-11-02 | 1 | NaN | 2012 | 11 | 44 | 1 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 16680.24 | 19034.475 | 18467.5825 | 17726.3075 | 17154.9275 | 16604.3150 | 26627.7378 |

| 1001 | 2012-11-02 | 1 | NaN | 2012 | 11 | 44 | 1 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 16680.24 | 19034.475 | 18467.5825 | 17726.3075 | 17154.9275 | 16604.3150 | 26627.7378 |

| 1001 | 2012-11-02 | 1 | NaN | 2012 | 11 | 44 | 1 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 16680.24 | 19034.475 | 18467.5825 | 17726.3075 | 17154.9275 | 16604.3150 | 26627.7378 |

| 1002 | 2012-11-09 | 1 | NaN | 2012 | 11 | 45 | 2 | 21904.47 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 19930.000 | 19034.4750 | 18467.5825 | 17726.3075 | 17154.9275 | 20959.0553 |

| 1002 | 2012-11-09 | 1 | NaN | 2012 | 11 | 45 | 2 | 21904.47 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 19930.000 | 19034.4750 | 18467.5825 | 17726.3075 | 17154.9275 | 20959.0553 |

| 1002 | 2012-11-09 | 1 | NaN | 2012 | 11 | 45 | 2 | 21904.47 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 19930.000 | 19034.4750 | 18467.5825 | 17726.3075 | 17154.9275 | 20959.0553 |

| 1002 | 2012-11-09 | 1 | NaN | 2012 | 11 | 45 | 2 | 21904.47 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 19930.000 | 19034.4750 | 18467.5825 | 17726.3075 | 17154.9275 | 20959.0553 |

| 1002 | 2012-11-09 | 1 | NaN | 2012 | 11 | 45 | 2 | 21904.47 | 18947.81 | 19251.50 | 19616.22 | 18322.37 | 19930.000 | 19034.4750 | 18467.5825 | 17726.3075 | 17154.9275 | 20959.0553 |

Let’s create a label to split up our actuals from our prediction dataset before recombining.

train['type'] = 'actuals'

future['type'] = 'prediction'

full_df = pd.concat([train, future])

full_df.head(10)| Date | Dept | Weekly_Sales | Date_year | Date_month | Date_yweek | Date_mweek | Weekly_Sales_lag_5 | Weekly_Sales_lag_6 | Weekly_Sales_lag_7 | Weekly_Sales_lag_8 | Weekly_Sales_lag_9 | Weekly_Sales_lag_5_rolling_mean_win_4 | Weekly_Sales_lag_6_rolling_mean_win_4 | Weekly_Sales_lag_7_rolling_mean_win_4 | Weekly_Sales_lag_8_rolling_mean_win_4 | Weekly_Sales_lag_9_rolling_mean_win_4 | type | y_pred | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 19403.54 | 22809.2850 | 21102.8675 | 25967.5950 | 32216.620 | 32990.77 | actuals | NaN |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 19403.54 | 22809.2850 | 21102.8675 | 25967.5950 | 32216.620 | 32990.77 | actuals | NaN |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 19403.54 | 22809.2850 | 21102.8675 | 25967.5950 | 32216.620 | 32990.77 | actuals | NaN |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 19403.54 | 22809.2850 | 21102.8675 | 25967.5950 | 32216.620 | 32990.77 | actuals | NaN |

| 12 | 2010-04-30 | 1 | 16555.11 | 2010 | 4 | 17 | 5 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 19403.54 | 22809.2850 | 21102.8675 | 25967.5950 | 32216.620 | 32990.77 | actuals | NaN |

| 13 | 2010-05-07 | 1 | 17413.94 | 2010 | 5 | 18 | 1 | 57258.43 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 31666.9175 | 22809.2850 | 21102.8675 | 25967.595 | 32216.62 | actuals | NaN |

| 13 | 2010-05-07 | 1 | 17413.94 | 2010 | 5 | 18 | 1 | 57258.43 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 31666.9175 | 22809.2850 | 21102.8675 | 25967.595 | 32216.62 | actuals | NaN |

| 13 | 2010-05-07 | 1 | 17413.94 | 2010 | 5 | 18 | 1 | 57258.43 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 31666.9175 | 22809.2850 | 21102.8675 | 25967.595 | 32216.62 | actuals | NaN |

| 13 | 2010-05-07 | 1 | 17413.94 | 2010 | 5 | 18 | 1 | 57258.43 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 31666.9175 | 22809.2850 | 21102.8675 | 25967.595 | 32216.62 | actuals | NaN |

| 13 | 2010-05-07 | 1 | 17413.94 | 2010 | 5 | 18 | 1 | 57258.43 | 26229.21 | 22136.64 | 21043.39 | 21827.90 | 31666.9175 | 22809.2850 | 21102.8675 | 25967.595 | 32216.62 | actuals | NaN |

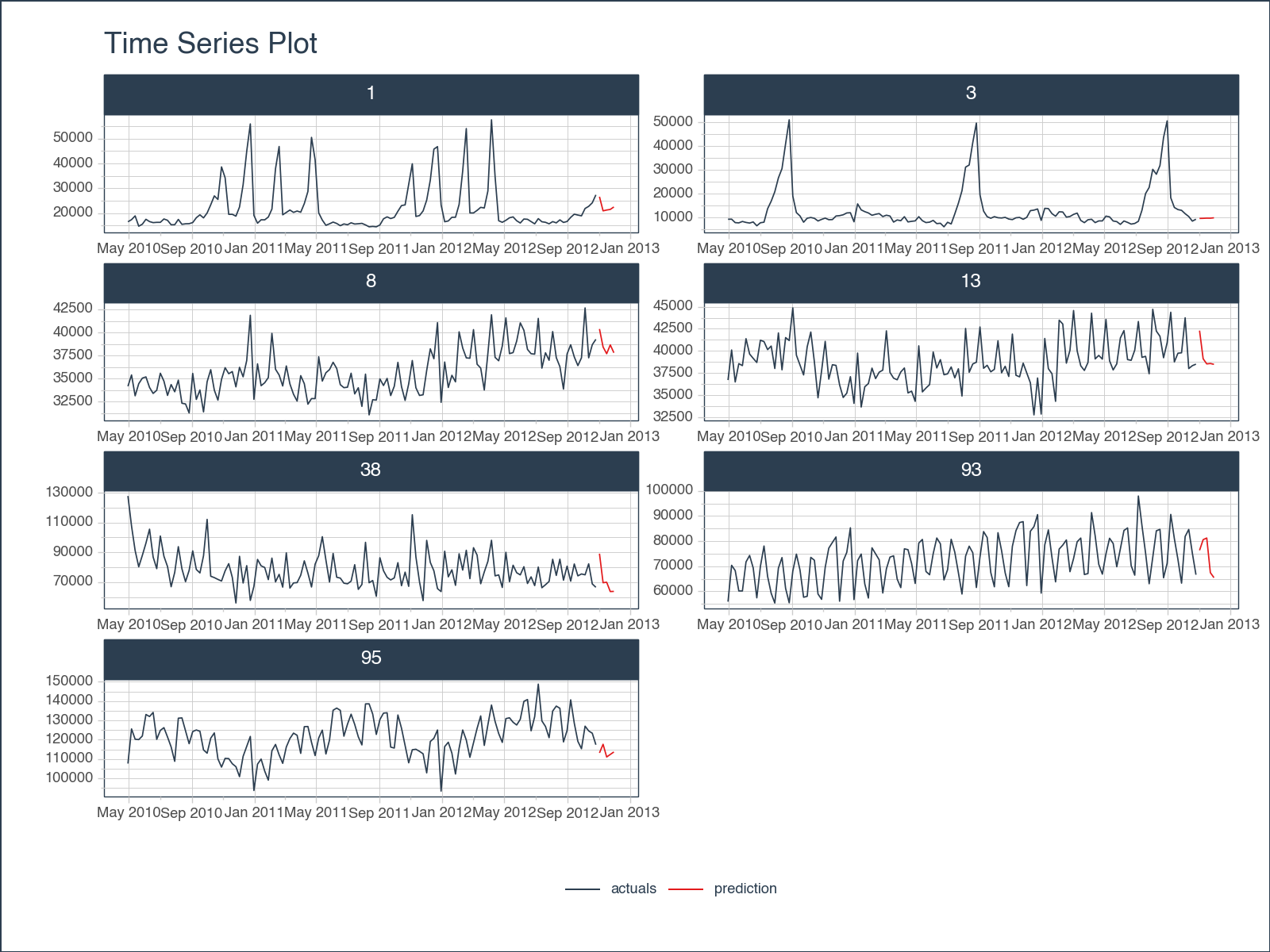

full_df['Weekly_Sales'] = np.where(full_df.type =='actuals', full_df.Weekly_Sales, full_df.y_pred)full_df \

.groupby('Dept') \

.plot_timeseries(

date_column = 'Date',

value_column = 'Weekly_Sales',

color_column = 'type',

smooth = False,

smooth_alpha = 0,

facet_ncol = 2,

facet_scales = "free",

y_intercept_color = tk.palette_timetk()['steel_blue'],

width = 800,

height = 600,

engine = 'plotly'

)full_df \

.groupby('Dept') \

.plot_timeseries(

date_column = 'Date',

value_column = 'Weekly_Sales',

color_column = 'type',

smooth = False,

smooth_alpha = 0,

facet_ncol = 2,

facet_scales = "free",

y_intercept_color = tk.palette_timetk()['steel_blue'],

width = 800,

height = 600,

engine = 'plotnine'

)

<Figure Size: (800 x 600)>Our weekly sales forecasts exhibit a noticeable alignment with historical trends, indicating that our models are effectively capturing essential data signals. It’s worth noting that with some additional feature engineering, we have the potential to further enhance the model’s performance.

Here are some additional techniques that can be explored to elevate its performance:

tk.augment_lags() function.tk.augment_rolling().tk.augment_fourier().These strategies hold promise for refining the model’s accuracy and predictive power

This exemplifies the remarkable capabilities of pytimetk in aiding Data Scientists in conducting comprehensive time series analysis for demand forecasting. Throughout this process, we employed various pytimetk functions and techniques to enhance our analytical approach:

tk.augment_time_signature() to generate a plethora of date features, enriching our dataset.tk.augment_lags() and tk.augment_rolling() from pytimetk played a pivotal role in our analysis, enabling us to create lag-based features and rolling calculations.tk.future_frame(), we constructed our prediction settk.plot_timeseries() to visualize our results.These pytimetk features provide incredibly powerful techniques with a very easy strcuture and minimal code. They were indispensable in crafting a high-quality sales forecast, seamlessly integrated with sklearn.

We are in the early stages of development. But it’s obvious the potential for pytimetk now in Python. 🐍