This guide covers speed and performance comparisons using the polars backend.

Beginning in version 0.2.0 of pytimetk, we introduced new polars engines to many of our functions. This is aimed at leveraging the speed benefits of polars without requiring you (the user) to learn a new data manipulation framework.

1 Pytimetk Speed Result Summary

It’s typical to see 2X to 15X speedups just by using the polars engine. Speedups of 500X to 3500X are possible by using efficient functions (e.g. staying away from lambdas).

Features/Properties

polars

pandas

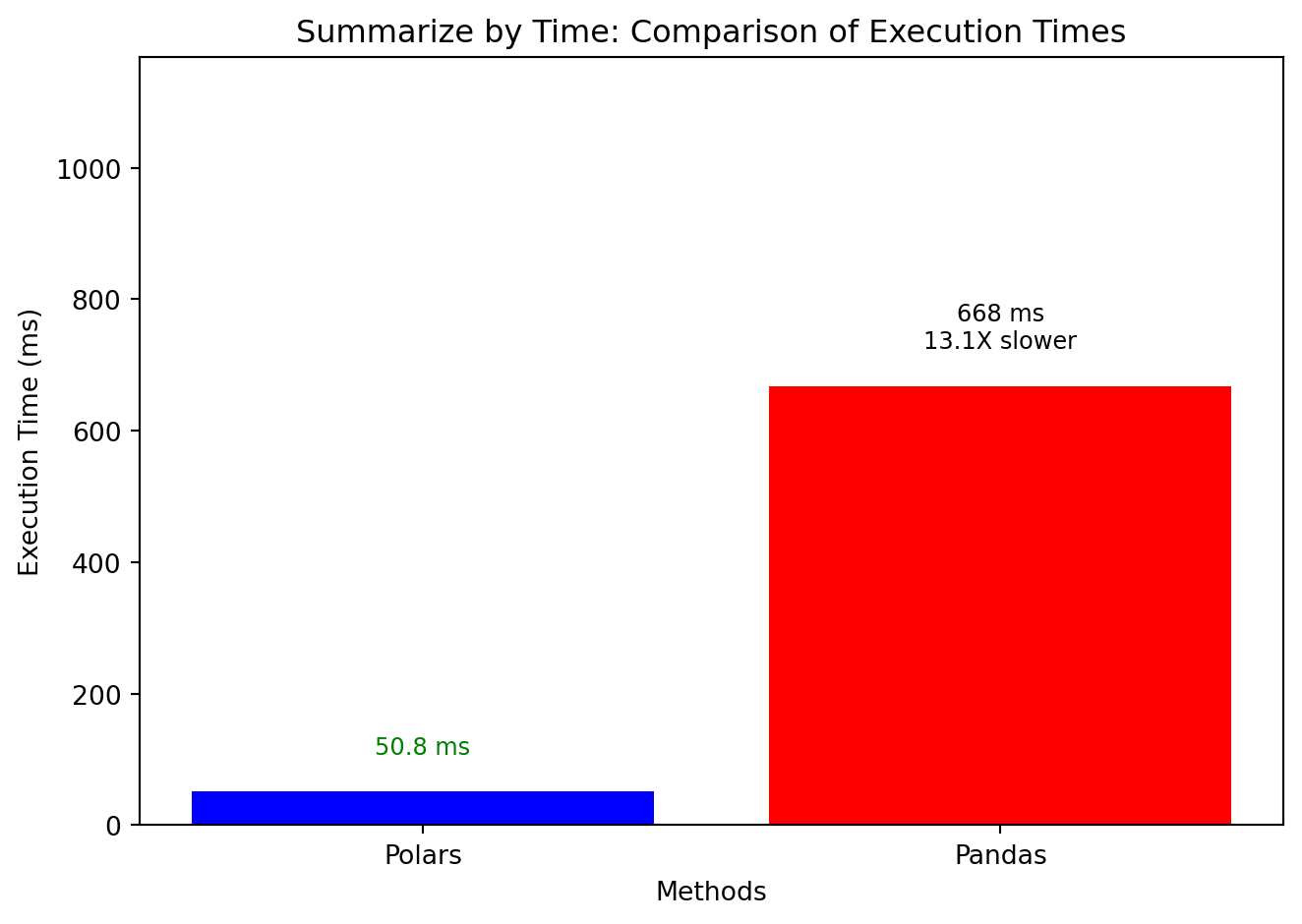

summarize_by_time()

🚀 13X Faster

🐢 Standard

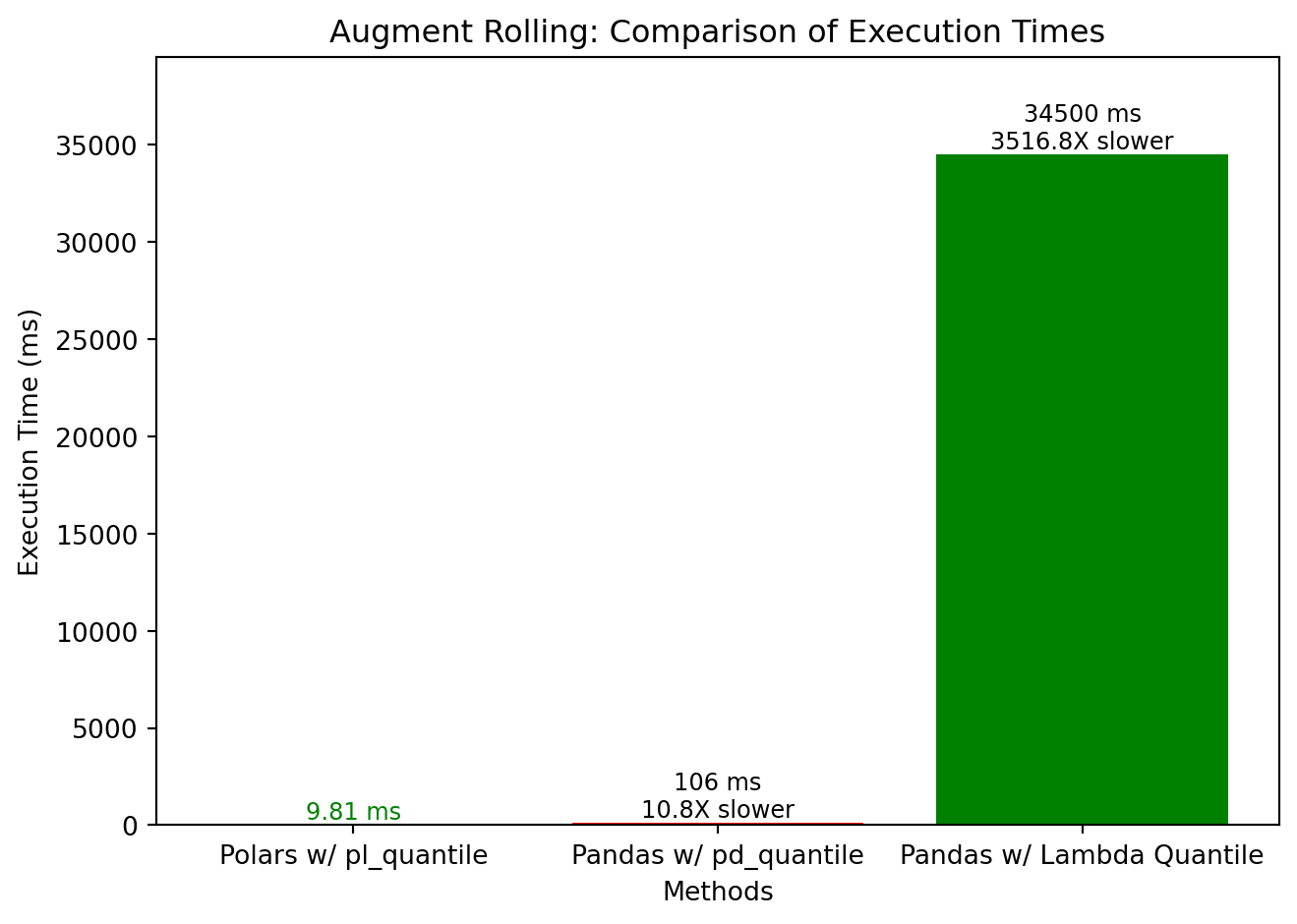

augment_rolling()

🚀 10X to 3500X Faster

🐢 Standard

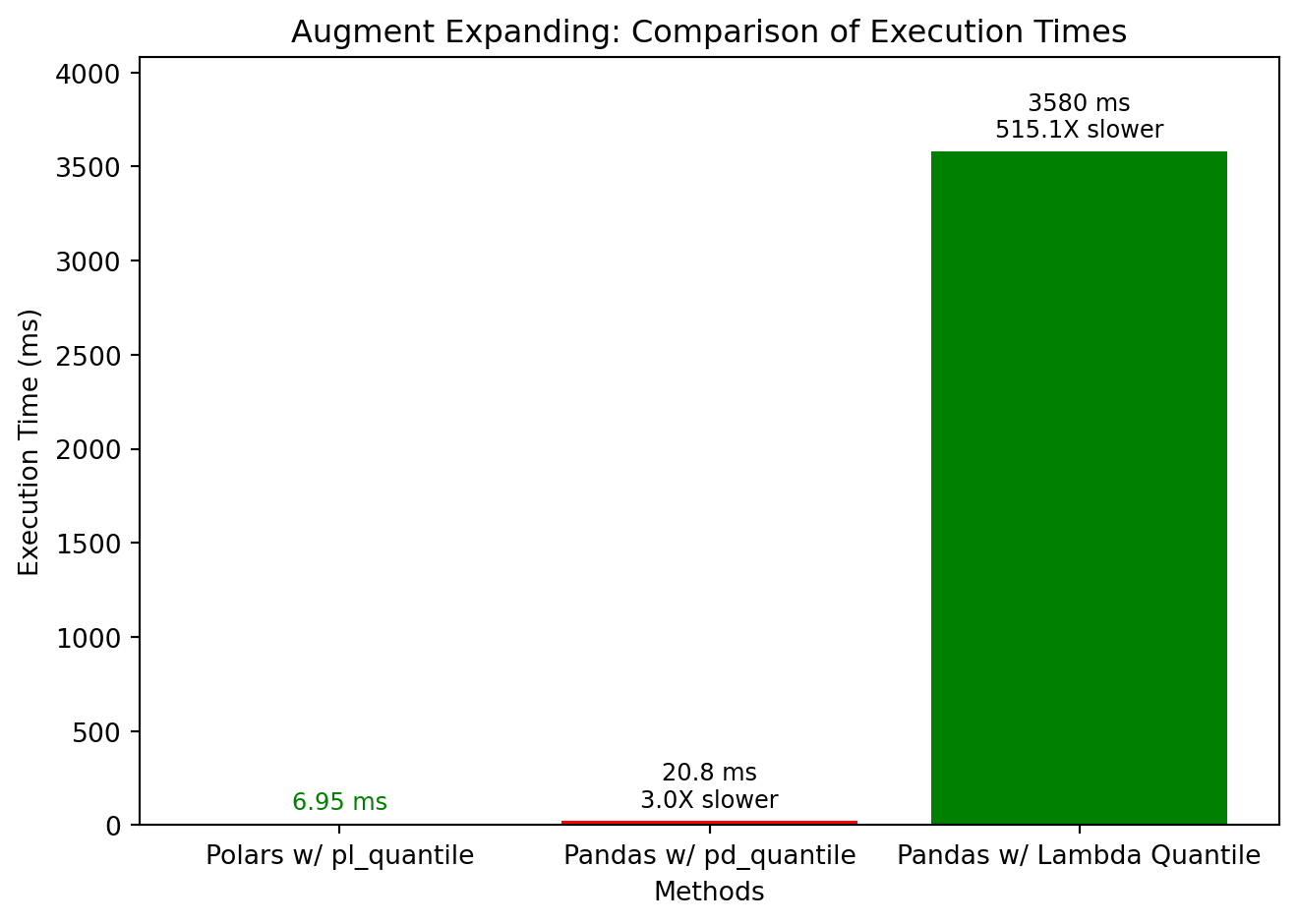

augment_expanding()

🚀 3X to 500X Faster

🐢 Standard

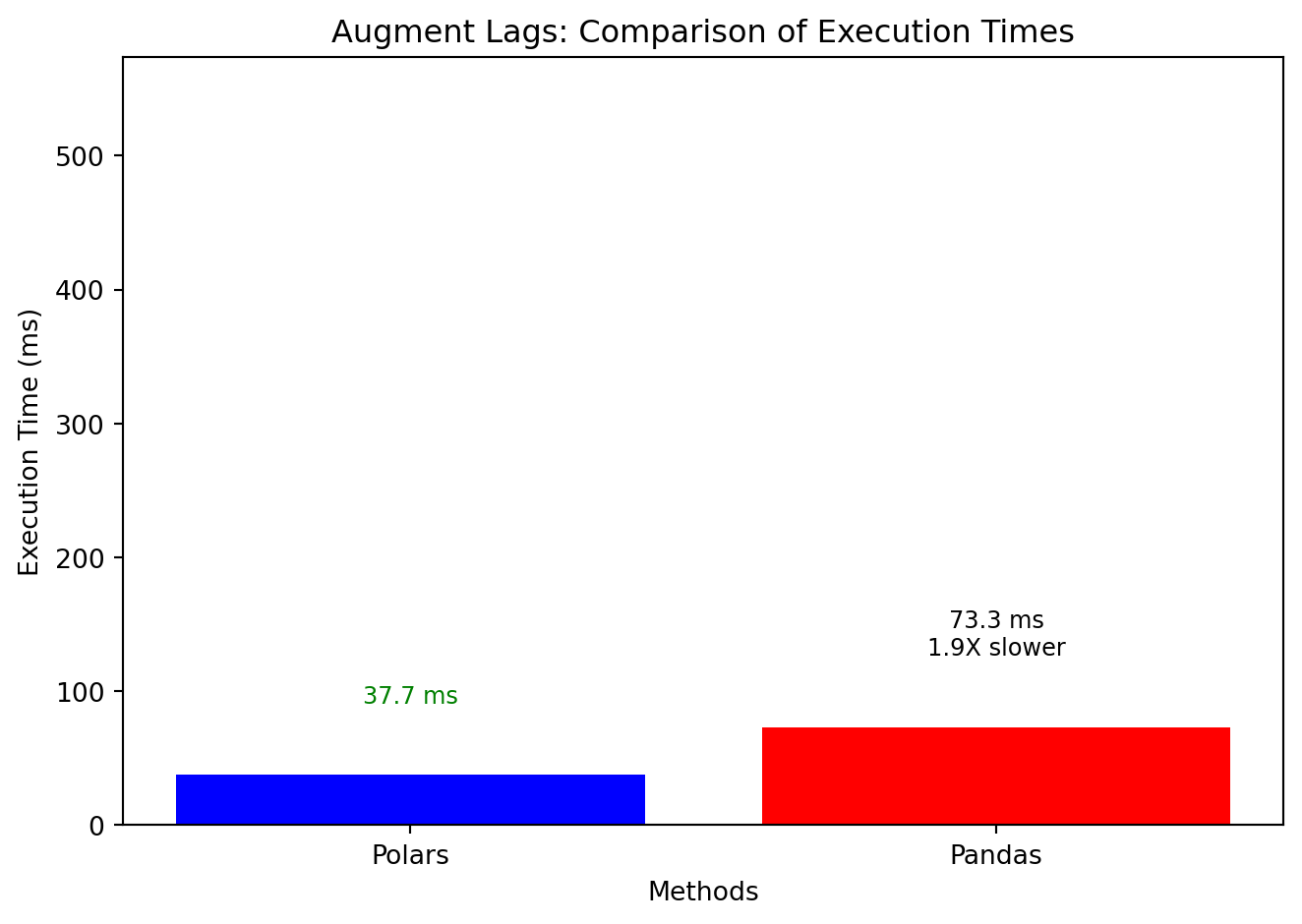

augment_lags()

🚀 2X to 20X Faster

🐢 Standard

2 About Performance

In time series, data is often large (<100M Rows), and contains many groups. Bbecause of this, computational efficiency is paramount. Beginning in pytimetk 0.2.0 we began introducing a new, polars backend to help improve the speed.

2.1 Key benefits:

You can get between 2X and 500X speed boost on many common time series operations

You don’t need to know how to use polars to gain massive speed boosts

Simply turn engine = 'polars' to get the speed boost.

2.2 What affects speed?

Many factors can affect speed. Things that are known to slow performance down:

Using non-optimized “lambda” functions. Lambda Functions are created at runtime. This process is flexible but extremely inefficient. Where possible use “built-in” or “configurable” functions instead.

Not using polars. Polars is built on top of Rust, which is a low-level language known for performance and optimized for speed. Using polars usually speeds up computation versus Pandas.

3 Speed Tests and Conclusions

Load the packages and datasets needed to replicate the speed tests (Click to Expand):

Code

# Librariesimport pytimetk as tkimport pandas as pdimport numpy as npimport matplotlib.pyplot as pltfrom pytimetk.utils.polars_helpers import pl_quantilefrom pytimetk.utils.pandas_helpers import pd_quantile# Datasetsexpedia_df = tk.load_dataset("expedia", parse_dates = ['date_time'])m4_daily_df = tk.load_dataset("m4_daily", parse_dates = ['date'])stocks_daily_df = tk.load_dataset('stocks_daily', parse_dates=['date'])# Plotting utilitydef make_time_comparison_plot(title, methods, times, height_spacer=500):""" Create a bar chart comparing execution times of different methods. Args: - title (str): Title for the plot. - methods (list of str): Names of the methods being compared. - times (list of float): Execution times corresponding to the methods. - height_spacer (int, optional): Additional space above the tallest bar. Defaults to 5000. Returns: - None. Displays the plot. """# Calculate how many times slower each method is relative to the fastest method min_time =min(times) times_slower = [time / min_time for time in times]# Create the bar chart bars = plt.bar(methods, times, color=['blue', 'red', 'green', 'orange'])# Add title and labels plt.title(f'{title}: Comparison of Execution Times') plt.ylabel('Execution Time (ms)') plt.xlabel('Methods')# Display the execution times and how many times slower on top of the barsfor bar, v, multiplier inzip(bars, times, times_slower): height = bar.get_height() plt.text(bar.get_x() + bar.get_width() /2, height +50, f"{v} ms\n{multiplier:.1f}X slower"if multiplier !=1elsef"{v} ms", ha='center', va='bottom', fontsize=9, color='black'if multiplier !=1else'green')# Adjust y-axis limit to make sure all labels fit plt.ylim(0, max(times) + height_spacer)# Display the plot plt.tight_layout()return plt

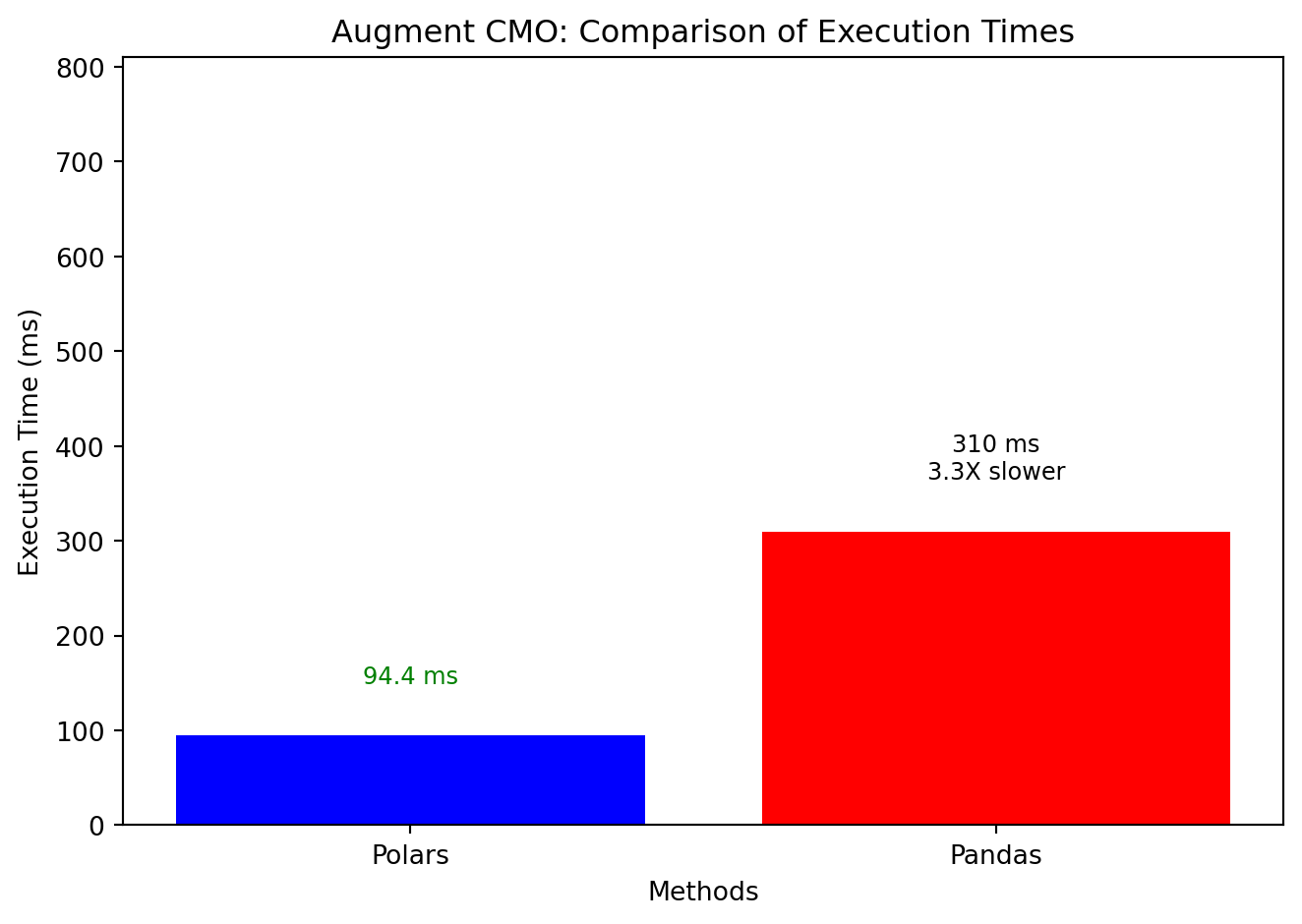

4 Feature Engineering Performance Comparisons

This section includes performance comparisons are common Time Series Feature Engineering tasks.

%%timeit -n 25df = ( stocks_daily_df .groupby('symbol') .augment_cmo( date_column ='date', value_column ='adjusted', periods = (5,30), engine ='polars', ))# 94.4 ms ± 3.24 ms per loop (mean ± std. dev. of 7 runs, 25 loops each)

Code

%%timeit -n 25df = ( stocks_daily_df .groupby('symbol') .augment_cmo( date_column ='date', value_column ='adjusted', periods = (5,30), engine ='pandas', ))# 73.3 ms ± 3.29 ms per loop (mean ± std. dev. of 7 runs, 25 loops each)

6 Conclusions

In general, when speed and performance is needed, which is quite often the case in large-scale time series databases (e.g. finance, customer analytics), the polars engine can be a substantial performance enhancer. Almost every function has experienced a performance increase with the new polars engine. We’ve seen many functions gain 10X increases and beyond.

7 More Coming Soon…

We are in the early stages of development. But it’s obvious the potential for pytimetk now in Python. 🐍

Please ⭐ us on GitHub (it takes 2-seconds and means a lot).