Autoregressive Forecasting with Recursive

Source:vignettes/recursive-forecasting.Rmd

recursive-forecasting.RmdTurn any

tidymodelinto an Autoregressive Forecasting Model

This short tutorial shows how you can use recursive()

to:

Make a Recursive Forecast Model for forecasting with short-term lags (i.e. Lag Size < Forecast Horizon).

Perform Recursive Panel Forecasting, which is when you have a single autoregressive model that predicts forecasts for multiple time series.

Recursive Panel Forecast with XGBoost

Forecasting with Recursive Ensembles

We have a separate modeltime.ensemble package that

includes support for recursive(). Making recursive

ensembles is covered in the “Forecasting

with Recursive Ensembles” article.

What is a Recursive Model?

A recursive model uses predictions to generate new values for independent features. These features are typically lags used in autoregressive models.

Why is Recursive needed for Autoregressive Models?

It’s important to understand that a recursive model is only needed

when using lagged features with a Lag Size < Forecast

Horizon. When the lag length is less than the forecast horizon,

a problem exists were missing values (NA) are generated in

the future data.

A solution that recursive() implements is to iteratively

fill these missing values in with values generated from predictions.

This technique can be used for:

Single time series predictions - Effectively turning any

tidymodelsmodel into an Autoregressive (AR) modelPanel time series predictions - In many situations we need to forecast more than one time series. We can batch-process these with 1 model by processing time series groups as panels. This technique can be extended to recursive forecasting for scalable models (1 model that predicts many time series).

Make a Recursive Forecast Model

We’ll start with the simplest example, turning a Linear Regresion into an Autoregressive model.

Data Visualization

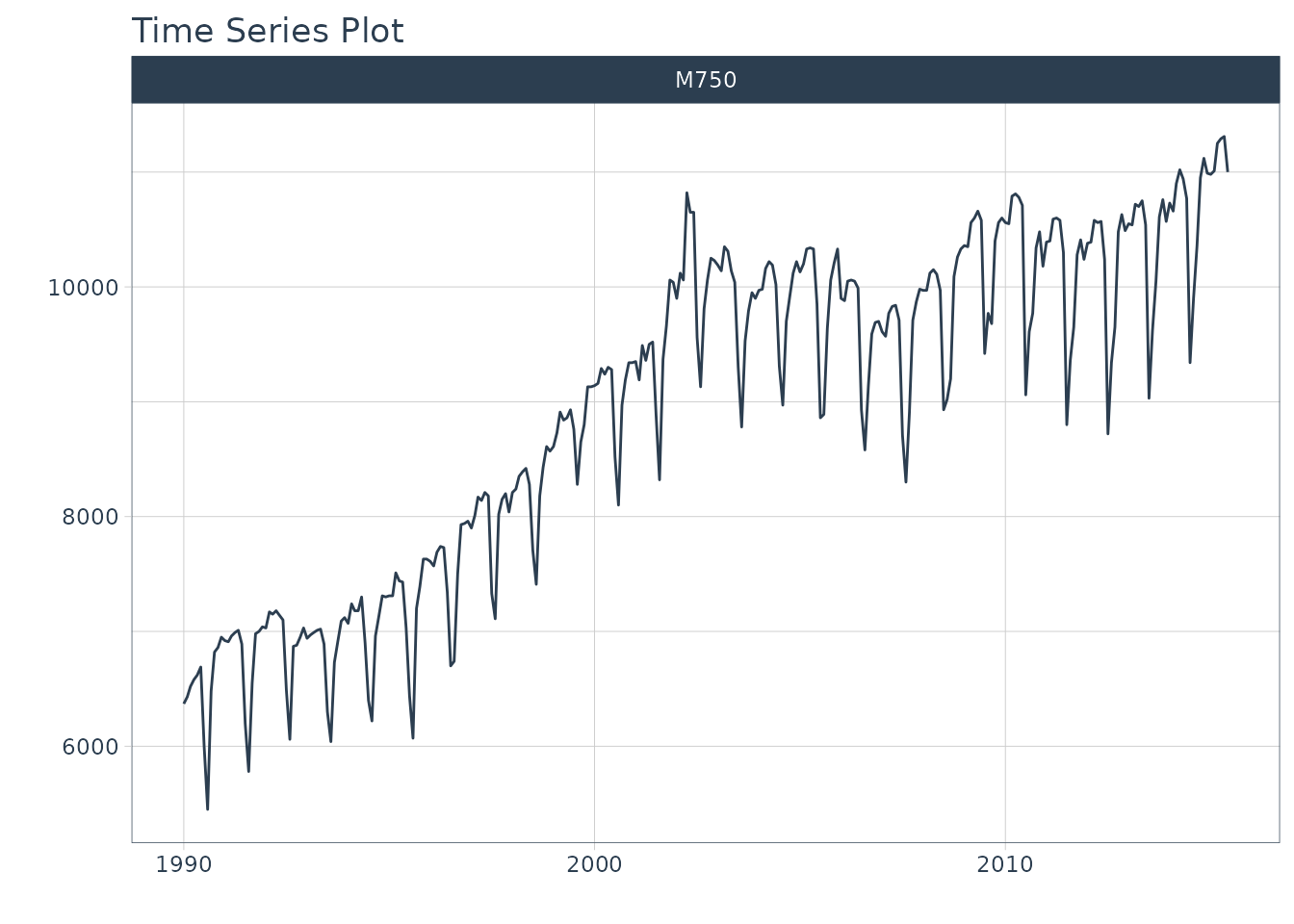

Let’s start with the m750 dataset.

m750

#> # A tibble: 306 × 3

#> id date value

#> <fct> <date> <dbl>

#> 1 M750 1990-01-01 6370

#> 2 M750 1990-02-01 6430

#> 3 M750 1990-03-01 6520

#> 4 M750 1990-04-01 6580

#> 5 M750 1990-05-01 6620

#> 6 M750 1990-06-01 6690

#> 7 M750 1990-07-01 6000

#> 8 M750 1990-08-01 5450

#> 9 M750 1990-09-01 6480

#> 10 M750 1990-10-01 6820

#> # ℹ 296 more rowsWe can visualize the data with plot_time_series().

m750 %>%

plot_time_series(

.date_var = date,

.value = value,

.facet_var = id,

.smooth = FALSE,

.interactive = FALSE

)

Data Preparation

Let’s establish a forecast horizon and extend the dataset to create a forecast region.

Transform Function

We’ll use short-term lags, lags with a size that are

smaller than the forecast horizon. Here we create a custom function,

lag_roll_transformer() that takes a dataset and adds lags 1

through 12 and a rolling mean using lag 12. Each of the features this

function use lags less than our forecast horizon of 24 months, which

means we need to use recursive().

lag_roll_transformer <- function(data){

data %>%

tk_augment_lags(value, .lags = 1:FORECAST_HORIZON) %>%

tk_augment_slidify(

contains("lag12"),

.f = ~mean(.x, na.rm = TRUE),

.period = 12,

.partial = TRUE

)

}Apply the Transform Function

When we apply the lag roll transformation to our extended data set, we can see the effect.

m750_rolling <- m750_extended %>%

lag_roll_transformer() %>%

select(-id)

m750_rolling

#> # A tibble: 330 × 27

#> date value value_lag1 value_lag2 value_lag3 value_lag4 value_lag5

#> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1990-01-01 6370 NA NA NA NA NA

#> 2 1990-02-01 6430 6370 NA NA NA NA

#> 3 1990-03-01 6520 6430 6370 NA NA NA

#> 4 1990-04-01 6580 6520 6430 6370 NA NA

#> 5 1990-05-01 6620 6580 6520 6430 6370 NA

#> 6 1990-06-01 6690 6620 6580 6520 6430 6370

#> 7 1990-07-01 6000 6690 6620 6580 6520 6430

#> 8 1990-08-01 5450 6000 6690 6620 6580 6520

#> 9 1990-09-01 6480 5450 6000 6690 6620 6580

#> 10 1990-10-01 6820 6480 5450 6000 6690 6620

#> # ℹ 320 more rows

#> # ℹ 20 more variables: value_lag6 <dbl>, value_lag7 <dbl>, value_lag8 <dbl>,

#> # value_lag9 <dbl>, value_lag10 <dbl>, value_lag11 <dbl>, value_lag12 <dbl>,

#> # value_lag13 <dbl>, value_lag14 <dbl>, value_lag15 <dbl>, value_lag16 <dbl>,

#> # value_lag17 <dbl>, value_lag18 <dbl>, value_lag19 <dbl>, value_lag20 <dbl>,

#> # value_lag21 <dbl>, value_lag22 <dbl>, value_lag23 <dbl>, value_lag24 <dbl>,

#> # value_lag12_roll_12 <dbl>Split into Training and Future Data

The training data needs to be completely filled in.

We remove any rows with NA.

train_data <- m750_rolling %>%

drop_na()

train_data

#> # A tibble: 282 × 27

#> date value value_lag1 value_lag2 value_lag3 value_lag4 value_lag5

#> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 1992-01-01 7030 7040 7000 6980 6550 5780

#> 2 1992-02-01 7170 7030 7040 7000 6980 6550

#> 3 1992-03-01 7150 7170 7030 7040 7000 6980

#> 4 1992-04-01 7180 7150 7170 7030 7040 7000

#> 5 1992-05-01 7140 7180 7150 7170 7030 7040

#> 6 1992-06-01 7100 7140 7180 7150 7170 7030

#> 7 1992-07-01 6490 7100 7140 7180 7150 7170

#> 8 1992-08-01 6060 6490 7100 7140 7180 7150

#> 9 1992-09-01 6870 6060 6490 7100 7140 7180

#> 10 1992-10-01 6880 6870 6060 6490 7100 7140

#> # ℹ 272 more rows

#> # ℹ 20 more variables: value_lag6 <dbl>, value_lag7 <dbl>, value_lag8 <dbl>,

#> # value_lag9 <dbl>, value_lag10 <dbl>, value_lag11 <dbl>, value_lag12 <dbl>,

#> # value_lag13 <dbl>, value_lag14 <dbl>, value_lag15 <dbl>, value_lag16 <dbl>,

#> # value_lag17 <dbl>, value_lag18 <dbl>, value_lag19 <dbl>, value_lag20 <dbl>,

#> # value_lag21 <dbl>, value_lag22 <dbl>, value_lag23 <dbl>, value_lag24 <dbl>,

#> # value_lag12_roll_12 <dbl>The future data has missing values in the “value”

column. We isolate these. Our autoregressive algorithm will predict

these. Notice that the lags have missing data, this is OK - and why we

are going to use recursive() to fill these missing values

in with predictions.

future_data <- m750_rolling %>%

filter(is.na(value))

future_data

#> # A tibble: 24 × 27

#> date value value_lag1 value_lag2 value_lag3 value_lag4 value_lag5

#> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 2015-07-01 NA 11000 11310 11290 11250 11010

#> 2 2015-08-01 NA NA 11000 11310 11290 11250

#> 3 2015-09-01 NA NA NA 11000 11310 11290

#> 4 2015-10-01 NA NA NA NA 11000 11310

#> 5 2015-11-01 NA NA NA NA NA 11000

#> 6 2015-12-01 NA NA NA NA NA NA

#> 7 2016-01-01 NA NA NA NA NA NA

#> 8 2016-02-01 NA NA NA NA NA NA

#> 9 2016-03-01 NA NA NA NA NA NA

#> 10 2016-04-01 NA NA NA NA NA NA

#> # ℹ 14 more rows

#> # ℹ 20 more variables: value_lag6 <dbl>, value_lag7 <dbl>, value_lag8 <dbl>,

#> # value_lag9 <dbl>, value_lag10 <dbl>, value_lag11 <dbl>, value_lag12 <dbl>,

#> # value_lag13 <dbl>, value_lag14 <dbl>, value_lag15 <dbl>, value_lag16 <dbl>,

#> # value_lag17 <dbl>, value_lag18 <dbl>, value_lag19 <dbl>, value_lag20 <dbl>,

#> # value_lag21 <dbl>, value_lag22 <dbl>, value_lag23 <dbl>, value_lag24 <dbl>,

#> # value_lag12_roll_12 <dbl>Modeling

We’ll make 2 models for comparison purposes:

- Straight-Line Forecast Model using Linear Regression with the Date feature

- Autoregressive Forecast Model using Linear Regression with the Date feature, Lags 1-12, and Rolling Mean Lag 12

Model 1 (Baseline): Straight-Line Forecast Model

A straight-line forecast is just to illustrate the effect of no autoregressive features. Consider this a NAIVE modeling approach. The only feature that is used as a dependent variable is the “date” column.

model_fit_lm <- linear_reg() %>%

set_engine("lm") %>%

fit(value ~ date, data = train_data)

model_fit_lm

#> parsnip model object

#>

#>

#> Call:

#> stats::lm(formula = value ~ date, data = data)

#>

#> Coefficients:

#> (Intercept) date

#> 3356.7208 0.4712Model 2: Autoregressive Forecast Model

The autoregressive forecast model is simply a parsnip

model with one additional step: using recursive(). The key

components are:

transform: A transformation function. We use the function previously made that generated Lags 1 to 12 and the Rolling Mean Lag 12 features.-

train_tail: The tail of the training data, which must be as large as the lags used in the transform function (i.e. lag 12).- Train tail can be larger than the lag size used. Notice that we use the Forecast Horizon, which is size 24.

- For Panel Data, we need to include the tail for each group. We have

provided a convenient

panel_tail()function.

id(Optional): This is used to identify groups for Recursive Panel Data.

# Autoregressive Forecast

model_fit_lm_recursive <- linear_reg() %>%

set_engine("lm") %>%

fit(value ~ ., data = train_data) %>%

# One additional step - use recursive()

recursive(

transform = lag_roll_transformer,

train_tail = tail(train_data, FORECAST_HORIZON)

)

model_fit_lm_recursive

#> Recursive [parsnip model]

#>

#> parsnip model object

#>

#>

#> Call:

#> stats::lm(formula = value ~ ., data = data)

#>

#> Coefficients:

#> (Intercept) date value_lag1

#> 164.14732 0.00677 0.61244

#> value_lag2 value_lag3 value_lag4

#> 0.18402 -0.07128 0.12089

#> value_lag5 value_lag6 value_lag7

#> -0.01750 0.07095 0.09785

#> value_lag8 value_lag9 value_lag10

#> -0.08053 0.04887 0.03030

#> value_lag11 value_lag12 value_lag13

#> -0.01755 0.73318 -0.52958

#> value_lag14 value_lag15 value_lag16

#> -0.21410 0.07734 -0.13879

#> value_lag17 value_lag18 value_lag19

#> 0.04351 -0.08894 -0.08732

#> value_lag20 value_lag21 value_lag22

#> 0.06641 -0.05737 -0.02331

#> value_lag23 value_lag24 value_lag12_roll_12

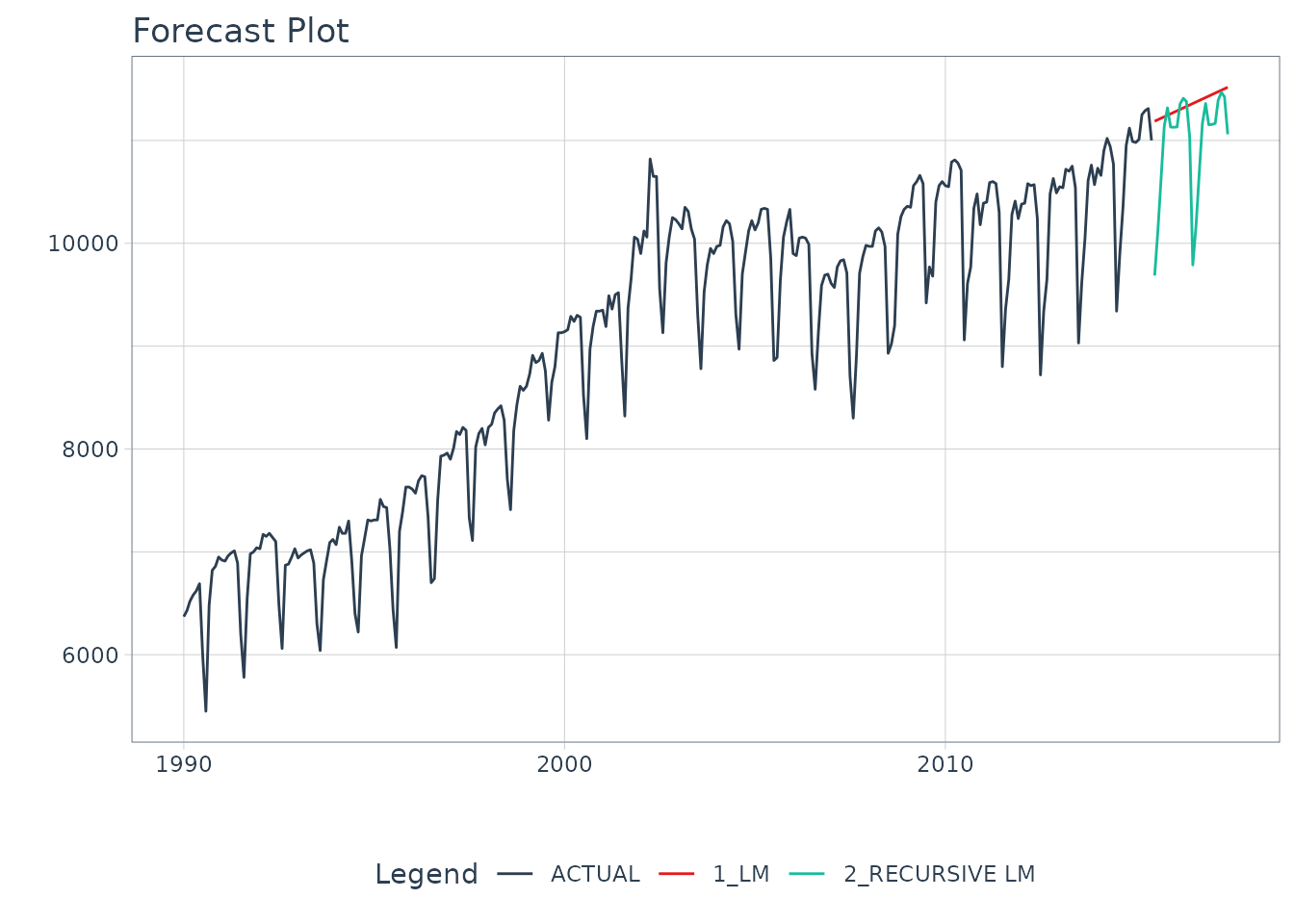

#> 0.05754 0.15960 NAModeltime Forecasting Workflow

Once we have our fitted model, we can follow the Modeltime Workflow (note we are skipping calibration and refitting, but this can be performed to get confidence intervals):

First, we add fitted models to a Model Table using

modeltime_table(). (Note - If your model description says

“LM”, install the development version of modeltime, which

has improved model descriptions for recursive models).

model_tbl <- modeltime_table(

model_fit_lm,

model_fit_lm_recursive

)

model_tbl

#> # Modeltime Table

#> # A tibble: 2 × 3

#> .model_id .model .model_desc

#> <int> <list> <chr>

#> 1 1 <fit[+]> LM

#> 2 2 <fit[+]> RECURSIVE LMNext, we perform Forecast Evaluation using

modeltime_forecast() and

plot_modeltime_forecast().

model_tbl %>%

# Forecast using future data

modeltime_forecast(

new_data = future_data,

actual_data = m750

) %>%

# Visualize the forecast

plot_modeltime_forecast(

.interactive = FALSE,

.conf_interval_show = FALSE

)

We can see the benefit of autoregressive features.

Recursive Forecasting with Panel Models

We can take this further by extending what we’ve learned here to panel data:

Panel Data:

- Grouped transformation functions:

lag_roll_transformer_grouped() -

recursive(): Usingidand thepanel_tail()function

More sophisticated algorithms:

- Instead of using a simple Linear Regression

- We use

xgboostto forecast multiple time series

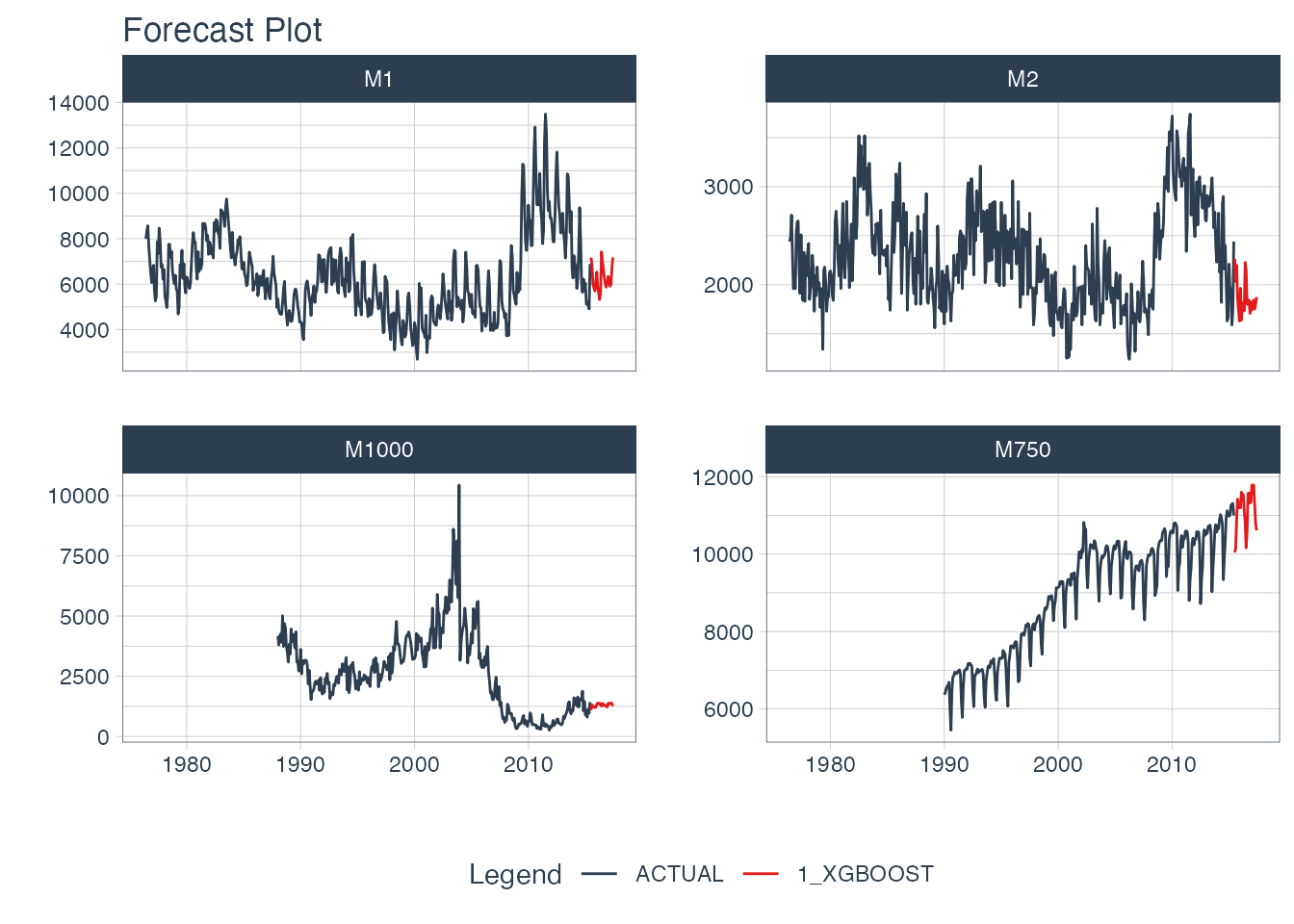

Data Visualization

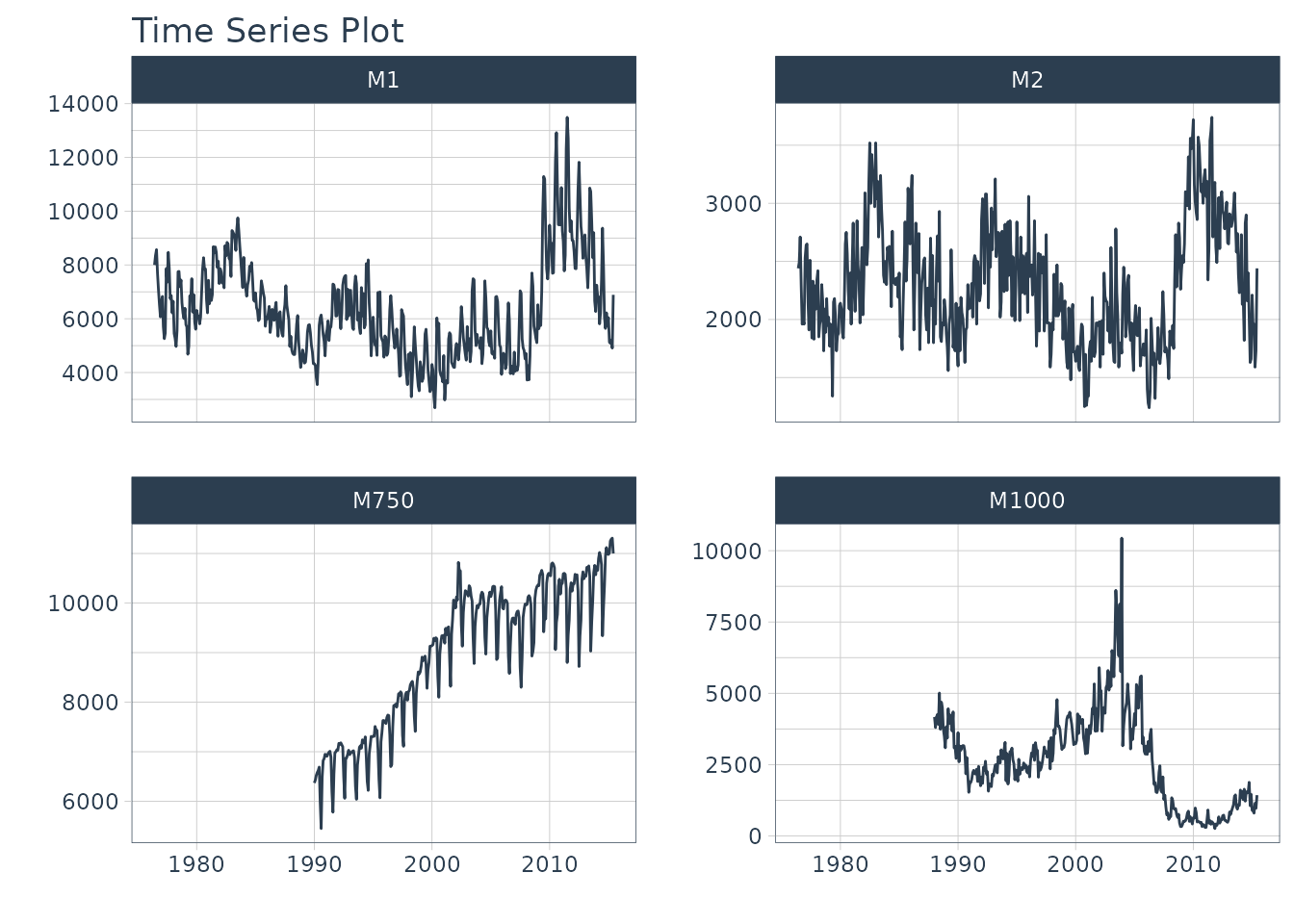

Now we have 4 time series that we will forecast.

m4_monthly %>%

plot_time_series(

.date_var = date,

.value = value,

.facet_var = id,

.facet_ncol = 2,

.smooth = FALSE,

.interactive = FALSE

)

Data Preparation

We use timetk::future_frame() to project each series

forward by the forecast horizon. This sets up an extended data set with

each series extended by 24 time stamps.

Apply the Transform Function

We apply the groupwise lag transformation to the extended data set. This adds autoregressive features.

m4_lags <- m4_extended %>%

lag_roll_transformer_grouped()

m4_lags

#> # A tibble: 1,670 × 28

#> id date value value_lag1 value_lag2 value_lag3 value_lag4 value_lag5

#> <fct> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 M1 1976-06-01 8000 NA NA NA NA NA

#> 2 M1 1976-07-01 8350 8000 NA NA NA NA

#> 3 M1 1976-08-01 8570 8350 8000 NA NA NA

#> 4 M1 1976-09-01 7700 8570 8350 8000 NA NA

#> 5 M1 1976-10-01 7080 7700 8570 8350 8000 NA

#> 6 M1 1976-11-01 6520 7080 7700 8570 8350 8000

#> 7 M1 1976-12-01 6070 6520 7080 7700 8570 8350

#> 8 M1 1977-01-01 6650 6070 6520 7080 7700 8570

#> 9 M1 1977-02-01 6830 6650 6070 6520 7080 7700

#> 10 M1 1977-03-01 5710 6830 6650 6070 6520 7080

#> # ℹ 1,660 more rows

#> # ℹ 20 more variables: value_lag6 <dbl>, value_lag7 <dbl>, value_lag8 <dbl>,

#> # value_lag9 <dbl>, value_lag10 <dbl>, value_lag11 <dbl>, value_lag12 <dbl>,

#> # value_lag13 <dbl>, value_lag14 <dbl>, value_lag15 <dbl>, value_lag16 <dbl>,

#> # value_lag17 <dbl>, value_lag18 <dbl>, value_lag19 <dbl>, value_lag20 <dbl>,

#> # value_lag21 <dbl>, value_lag22 <dbl>, value_lag23 <dbl>, value_lag24 <dbl>,

#> # value_lag12_roll_12 <dbl>Split into Training and Future Data

Just like the single case, we split into future and training data.

Modeling

We’ll use a more sophisticated algorithm xgboost to

develop an autoregressive model.

# Modeling Autoregressive Panel Data

set.seed(123)

model_fit_xgb_recursive <- boost_tree(

mode = "regression",

learn_rate = 0.35

) %>%

set_engine("xgboost") %>%

fit(

value ~ .

+ month(date, label = TRUE)

+ as.numeric(date)

- date,

data = train_data

) %>%

recursive(

id = "id", # We add an id = "id" to specify the groups

transform = lag_roll_transformer_grouped,

# We use panel_tail() to grab tail by groups

train_tail = panel_tail(train_data, id, FORECAST_HORIZON)

)

model_fit_xgb_recursive

#> Recursive [parsnip model]

#>

#> parsnip model object

#>

#> ##### xgb.Booster

#> call:

#> xgboost::xgb.train(params = list(eta = 0.35, max_depth = 6, gamma = 0,

#> colsample_bytree = 1, colsample_bynode = 1, min_child_weight = 1,

#> subsample = 1, nthread = 1, objective = "reg:squarederror"),

#> data = x$data, nrounds = 15, evals = x$watchlist, verbose = 0)

#> # of features: 41

#> # of rounds: 15

#> callbacks:

#> evaluation_log

#> evaluation_log:

#> iter training_rmse

#> <num> <num>

#> 1 2020.6031

#> 2 1363.6807

#> --- ---

#> 14 185.7499

#> 15 178.4500Modeltime Forecasting Workflow

First, create a Modeltime Table. Note - If your model description

says “XGBOOST”, install the development version of

modeltime, which has improved model descriptions for

recursive models).

model_tbl <- modeltime_table(

model_fit_xgb_recursive

)

model_tbl

#> # Modeltime Table

#> # A tibble: 1 × 3

#> .model_id .model .model_desc

#> <int> <list> <chr>

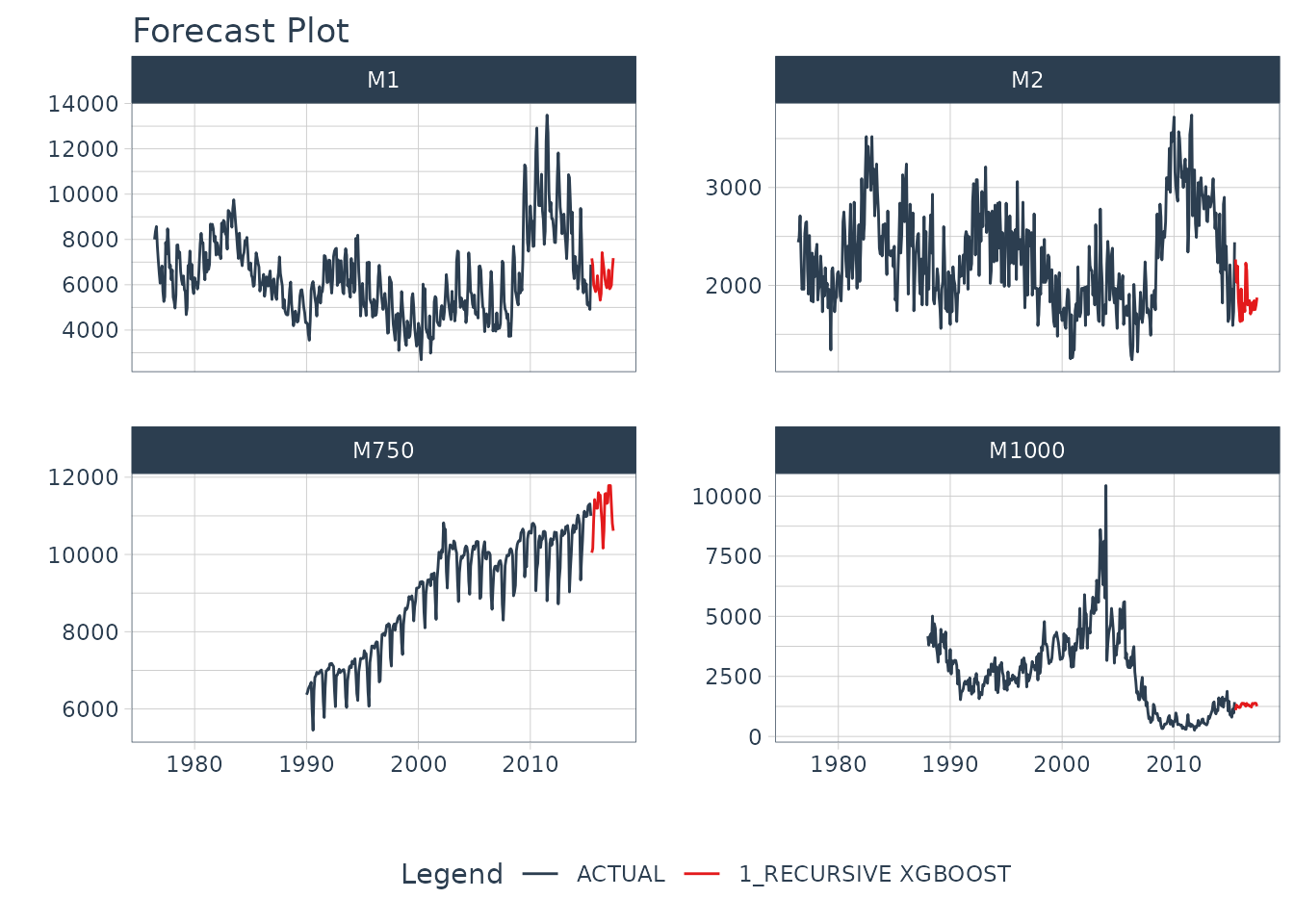

#> 1 1 <fit[+]> RECURSIVE XGBOOSTNext, we can forecast the results.

model_tbl %>%

modeltime_forecast(

new_data = future_data,

actual_data = m4_monthly,

keep_data = TRUE

) %>%

group_by(id) %>%

plot_modeltime_forecast(

.interactive = FALSE,

.conf_interval_show = FALSE,

.facet_ncol = 2

)

Summary

We just showcased Recursive Forecasting. But this is a simple problem. And, there’s a lot more to learning time series.

- Many more algorithms

- Ensembling

- Machine Learning

- Deep Learning

- Scalable Modeling: 10,000+ time series

Your probably thinking how am I ever going to learn time series forecasting. Here’s the solution that will save you years of struggling.

Take the High-Performance Forecasting Course

Become the forecasting expert for your organization

High-Performance Time Series Course

Time Series is Changing

Time series is changing. Businesses now need 10,000+ time series forecasts every day. This is what I call a High-Performance Time Series Forecasting System (HPTSF) - Accurate, Robust, and Scalable Forecasting.

High-Performance Forecasting Systems will save companies by improving accuracy and scalability. Imagine what will happen to your career if you can provide your organization a “High-Performance Time Series Forecasting System” (HPTSF System).

How to Learn High-Performance Time Series Forecasting

I teach how to build a HPTFS System in my High-Performance Time Series Forecasting Course. You will learn:

-

Time Series Machine Learning (cutting-edge) with

Modeltime- 30+ Models (Prophet, ARIMA, XGBoost, Random Forest, & many more) -

Deep Learning with

GluonTS(Competition Winners) - Time Series Preprocessing, Noise Reduction, & Anomaly Detection

- Feature engineering using lagged variables & external regressors

- Hyperparameter Tuning

- Time series cross-validation

- Ensembling Multiple Machine Learning & Univariate Modeling Techniques (Competition Winner)

- Scalable Forecasting - Forecast 1000+ time series in parallel

- and more.

Become the Time Series Expert for your organization.