Create a Recursive Time Series Model from a Parsnip or Workflow Regression Model

Source:R/modeltime-recursive.R

recursive.RdCreate a Recursive Time Series Model from a Parsnip or Workflow Regression Model

Arguments

- object

An object of

model_fitor a fittedworkflowclass- transform

A transformation performed on

new_dataafter each step of recursive algorithm.Transformation Function: Must have one argument

data(see examples)

- train_tail

A tibble with tail of training data set. In most cases it'll be required to create some variables based on dependent variable.

- id

(Optional) An identifier that can be provided to perform a panel forecast. A single quoted column name (e.g.

id = "id").- chunk_size

The size of the smallest lag used in

transform. If the smallest lag necessary is n, the forecasts can be computed in chunks of n, which can dramatically improve performance. Defaults to 1. Non-integers are coerced to integer, e.g.chunk_size = 3.5will be coerced to integer viaas.integer().- ...

Not currently used.

Details

What is a Recursive Model?

A recursive model uses predictions to generate new values for independent features. These features are typically lags used in autoregressive models. It's important to understand that a recursive model is only needed when the Lag Size < Forecast Horizon.

Why is Recursive needed for Autoregressive Models with Lag Size < Forecast Horizon?

When the lag length is less than the forecast horizon,

a problem exists were missing values (NA) are

generated in the future data. A solution that recursive() implements

is to iteratively fill these missing values in with values generated

from predictions.

Recursive Process

When producing forecast, the following steps are performed:

Computing forecast for first row of new data. The first row cannot contain NA in any required column.

Filling i-th place of the dependent variable column with already computed forecast.

Computing missing features for next step, based on already calculated prediction. These features are computed with on a tibble object made from binded

train_tail(i.e. tail of training data set) andnew_data(which is an argument of predict function).Jumping into point 2., and repeating rest of steps till the for-loop is ended.

Recursion for Panel Data

Panel data is time series data with multiple groups identified by an ID column.

The recursive() function can be used for Panel Data with the following modifications:

Supply an

idcolumn as a quoted column nameReplace

tail()withpanel_tail()to use tails for each time series group.

See also

panel_tail()- Used to generate tails for multiple time series groups.

Examples

# \donttest{

# Libraries & Setup ----

library(tidymodels)

library(dplyr)

library(tidyr)

library(timetk)

library(slider)

# ---- SINGLE TIME SERIES (NON-PANEL) -----

m750

#> # A tibble: 306 × 3

#> id date value

#> <fct> <date> <dbl>

#> 1 M750 1990-01-01 6370

#> 2 M750 1990-02-01 6430

#> 3 M750 1990-03-01 6520

#> 4 M750 1990-04-01 6580

#> 5 M750 1990-05-01 6620

#> 6 M750 1990-06-01 6690

#> 7 M750 1990-07-01 6000

#> 8 M750 1990-08-01 5450

#> 9 M750 1990-09-01 6480

#> 10 M750 1990-10-01 6820

#> # ℹ 296 more rows

FORECAST_HORIZON <- 24

m750_extended <- m750 %>%

group_by(id) %>%

future_frame(

.length_out = FORECAST_HORIZON,

.bind_data = TRUE

) %>%

ungroup()

#> .date_var is missing. Using: date

# TRANSFORM FUNCTION ----

# - Function runs recursively that updates the forecasted dataset

lag_roll_transformer <- function(data){

data %>%

# Lags

tk_augment_lags(value, .lags = 1:12) %>%

# Rolling Features

mutate(rolling_mean_12 = lag(slide_dbl(

value, .f = mean, .before = 12, .complete = FALSE

), 1))

}

# Data Preparation

m750_rolling <- m750_extended %>%

lag_roll_transformer() %>%

select(-id)

train_data <- m750_rolling %>%

drop_na()

future_data <- m750_rolling %>%

filter(is.na(value))

# Modeling

# Straight-Line Forecast

model_fit_lm <- linear_reg() %>%

set_engine("lm") %>%

# Use only date feature as regressor

fit(value ~ date, data = train_data)

# Autoregressive Forecast

model_fit_lm_recursive <- linear_reg() %>%

set_engine("lm") %>%

# Use date plus all lagged features

fit(value ~ ., data = train_data) %>%

# Add recursive() w/ transformer and train_tail

recursive(

transform = lag_roll_transformer,

train_tail = tail(train_data, FORECAST_HORIZON)

)

model_fit_lm_recursive

#> Recursive [parsnip model]

#>

#> parsnip model object

#>

#>

#> Call:

#> stats::lm(formula = value ~ ., data = data)

#>

#> Coefficients:

#> (Intercept) date value_lag1 value_lag2

#> 147.32008 0.01273 1.59298 0.76666

#> value_lag3 value_lag4 value_lag5 value_lag6

#> 0.73081 0.76950 0.76871 0.74755

#> value_lag7 value_lag8 value_lag9 value_lag10

#> 0.77872 0.72985 0.75257 0.76582

#> value_lag11 value_lag12 rolling_mean_12

#> 0.79979 1.62469 -9.85822

#>

# Forecasting

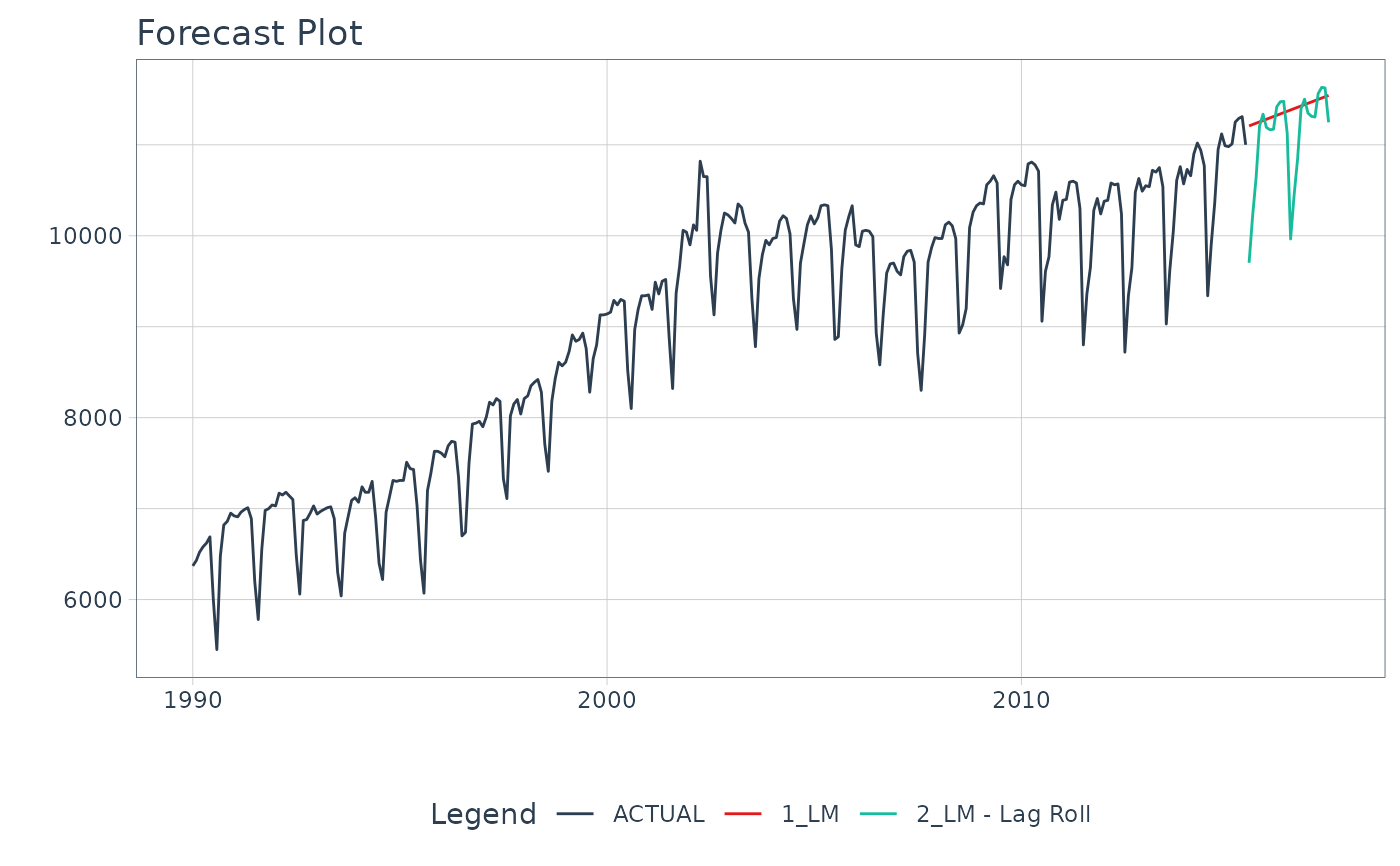

modeltime_table(

model_fit_lm,

model_fit_lm_recursive

) %>%

update_model_description(2, "LM - Lag Roll") %>%

modeltime_forecast(

new_data = future_data,

actual_data = m750

) %>%

plot_modeltime_forecast(

.interactive = FALSE,

.conf_interval_show = FALSE

)

# MULTIPLE TIME SERIES (PANEL DATA) -----

m4_monthly

#> # A tibble: 1,574 × 3

#> id date value

#> <fct> <date> <dbl>

#> 1 M1 1976-06-01 8000

#> 2 M1 1976-07-01 8350

#> 3 M1 1976-08-01 8570

#> 4 M1 1976-09-01 7700

#> 5 M1 1976-10-01 7080

#> 6 M1 1976-11-01 6520

#> 7 M1 1976-12-01 6070

#> 8 M1 1977-01-01 6650

#> 9 M1 1977-02-01 6830

#> 10 M1 1977-03-01 5710

#> # ℹ 1,564 more rows

FORECAST_HORIZON <- 24

m4_extended <- m4_monthly %>%

group_by(id) %>%

future_frame(

.length_out = FORECAST_HORIZON,

.bind_data = TRUE

) %>%

ungroup()

#> .date_var is missing. Using: date

# TRANSFORM FUNCTION ----

# - NOTE - We create lags by group

lag_transformer_grouped <- function(data){

data %>%

group_by(id) %>%

tk_augment_lags(value, .lags = 1:FORECAST_HORIZON) %>%

ungroup()

}

m4_lags <- m4_extended %>%

lag_transformer_grouped()

train_data <- m4_lags %>%

drop_na()

future_data <- m4_lags %>%

filter(is.na(value))

# Modeling Autoregressive Panel Data

model_fit_lm_recursive <- linear_reg() %>%

set_engine("lm") %>%

fit(value ~ ., data = train_data) %>%

recursive(

id = "id", # We add an id = "id" to specify the groups

transform = lag_transformer_grouped,

# We use panel_tail() to grab tail by groups

train_tail = panel_tail(train_data, id, FORECAST_HORIZON)

)

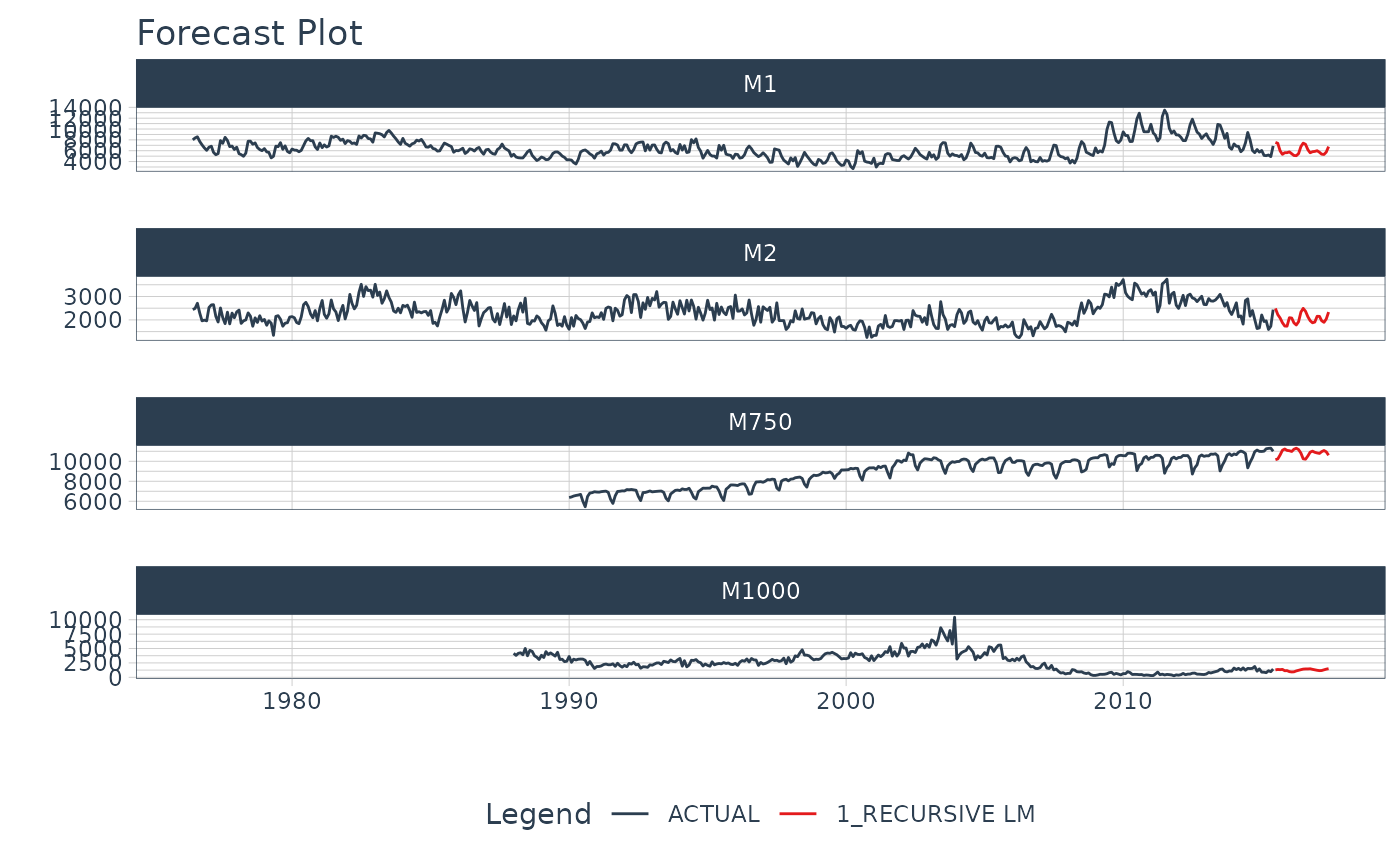

modeltime_table(

model_fit_lm_recursive

) %>%

modeltime_forecast(

new_data = future_data,

actual_data = m4_monthly,

keep_data = TRUE

) %>%

group_by(id) %>%

plot_modeltime_forecast(

.interactive = FALSE,

.conf_interval_show = FALSE

)

# MULTIPLE TIME SERIES (PANEL DATA) -----

m4_monthly

#> # A tibble: 1,574 × 3

#> id date value

#> <fct> <date> <dbl>

#> 1 M1 1976-06-01 8000

#> 2 M1 1976-07-01 8350

#> 3 M1 1976-08-01 8570

#> 4 M1 1976-09-01 7700

#> 5 M1 1976-10-01 7080

#> 6 M1 1976-11-01 6520

#> 7 M1 1976-12-01 6070

#> 8 M1 1977-01-01 6650

#> 9 M1 1977-02-01 6830

#> 10 M1 1977-03-01 5710

#> # ℹ 1,564 more rows

FORECAST_HORIZON <- 24

m4_extended <- m4_monthly %>%

group_by(id) %>%

future_frame(

.length_out = FORECAST_HORIZON,

.bind_data = TRUE

) %>%

ungroup()

#> .date_var is missing. Using: date

# TRANSFORM FUNCTION ----

# - NOTE - We create lags by group

lag_transformer_grouped <- function(data){

data %>%

group_by(id) %>%

tk_augment_lags(value, .lags = 1:FORECAST_HORIZON) %>%

ungroup()

}

m4_lags <- m4_extended %>%

lag_transformer_grouped()

train_data <- m4_lags %>%

drop_na()

future_data <- m4_lags %>%

filter(is.na(value))

# Modeling Autoregressive Panel Data

model_fit_lm_recursive <- linear_reg() %>%

set_engine("lm") %>%

fit(value ~ ., data = train_data) %>%

recursive(

id = "id", # We add an id = "id" to specify the groups

transform = lag_transformer_grouped,

# We use panel_tail() to grab tail by groups

train_tail = panel_tail(train_data, id, FORECAST_HORIZON)

)

modeltime_table(

model_fit_lm_recursive

) %>%

modeltime_forecast(

new_data = future_data,

actual_data = m4_monthly,

keep_data = TRUE

) %>%

group_by(id) %>%

plot_modeltime_forecast(

.interactive = FALSE,

.conf_interval_show = FALSE

)

# }

# }