Create rsample cross validation sets for time series.

This function produces a sampling plan starting with the most recent

time series observations, rolling backwards. The sampling procedure

is similar to rsample::rolling_origin(), but places the focus

of the cross validation on the most recent time series data.

Usage

time_series_cv(

data,

date_var = NULL,

initial = 5,

assess = 1,

skip = 1,

lag = 0,

cumulative = FALSE,

slice_limit = n(),

point_forecast = FALSE,

...

)Arguments

- data

A data frame.

- date_var

A date or date-time variable.

- initial

The number of samples used for analysis/modeling in the initial resample.

- assess

The number of samples used for each assessment resample.

- skip

A integer indicating how many (if any) additional resamples to skip to thin the total amount of data points in the analysis resample. See the example below.

- lag

A value to include an lag between the assessment and analysis set. This is useful if lagged predictors will be used during training and testing.

- cumulative

A logical. Should the analysis resample grow beyond the size specified by

initialat each resample?.- slice_limit

The number of slices to return. Set to

dplyr::n(), which returns the maximum number of slices.- point_forecast

Whether or not to have the testing set be a single point forecast or to be a forecast horizon. The default is to be a forecast horizon. Default:

FALSE- ...

These dots are for future extensions and must be empty.

Value

An tibble with classes time_series_cv, rset, tbl_df, tbl,

and data.frame. The results include a column for the data split objects

and a column called id that has a character string with the resample

identifier.

Details

Time-Based Specification

The initial, assess, skip, and lag variables can be specified as:

Numeric:

initial = 24Time-Based Phrases:

initial = "2 years", if thedatacontains adate_var(date or datetime)

Initial (Training Set) and Assess (Testing Set)

The main options, initial and assess, control the number of

data points from the original data that are in the analysis (training set)

and the assessment (testing set), respectively.

Skip

skip enables the function to not use every data point in the resamples.

When skip = 1, the resampling data sets will increment by one position.

Example: Suppose that the rows of a data set are consecutive days. Using skip = 7

will make the analysis data set operate on weeks instead of days. The

assessment set size is not affected by this option.

Lag

The Lag parameter creates an overlap between the Testing set. This is needed when lagged predictors are used.

Cumulative vs Sliding Window

When cumulative = TRUE, the initial parameter is ignored and the

analysis (training) set will grow as

resampling continues while the assessment (testing) set size will always remain

static.

When cumulative = FALSE, the initial parameter fixes the analysis (training)

set and resampling occurs over a fixed window.

Slice Limit

This controls the number of slices. If slice_limit = 5, only the most recent

5 slices will be returned.

Point Forecast

A point forecast is sometimes desired such as if you want to forecast a value "4-weeks" into the future. You can do this by setting the following parameters:

assess = "4 weeks"

point_forecast = TRUE

Panel Data / Time Series Groups / Overlapping Timestamps

Overlapping timestamps occur when your data has more than one time series group. This is sometimes called Panel Data or Time Series Groups.

When timestamps are duplicated (as in the case of "Panel Data" or "Time Series Groups"),

the resample calculation applies a sliding window of

fixed length to the dataset. See the example using walmart_sales_weekly

dataset below.

See also

time_series_cv()andrsample::rolling_origin()- Functions used to create time series resample specifications.plot_time_series_cv_plan()- The plotting function used for visualizing the time series resample plan.time_series_split()- A convenience function to return a single time series split containing a training/testing sample.

Examples

library(dplyr)

# DATA ----

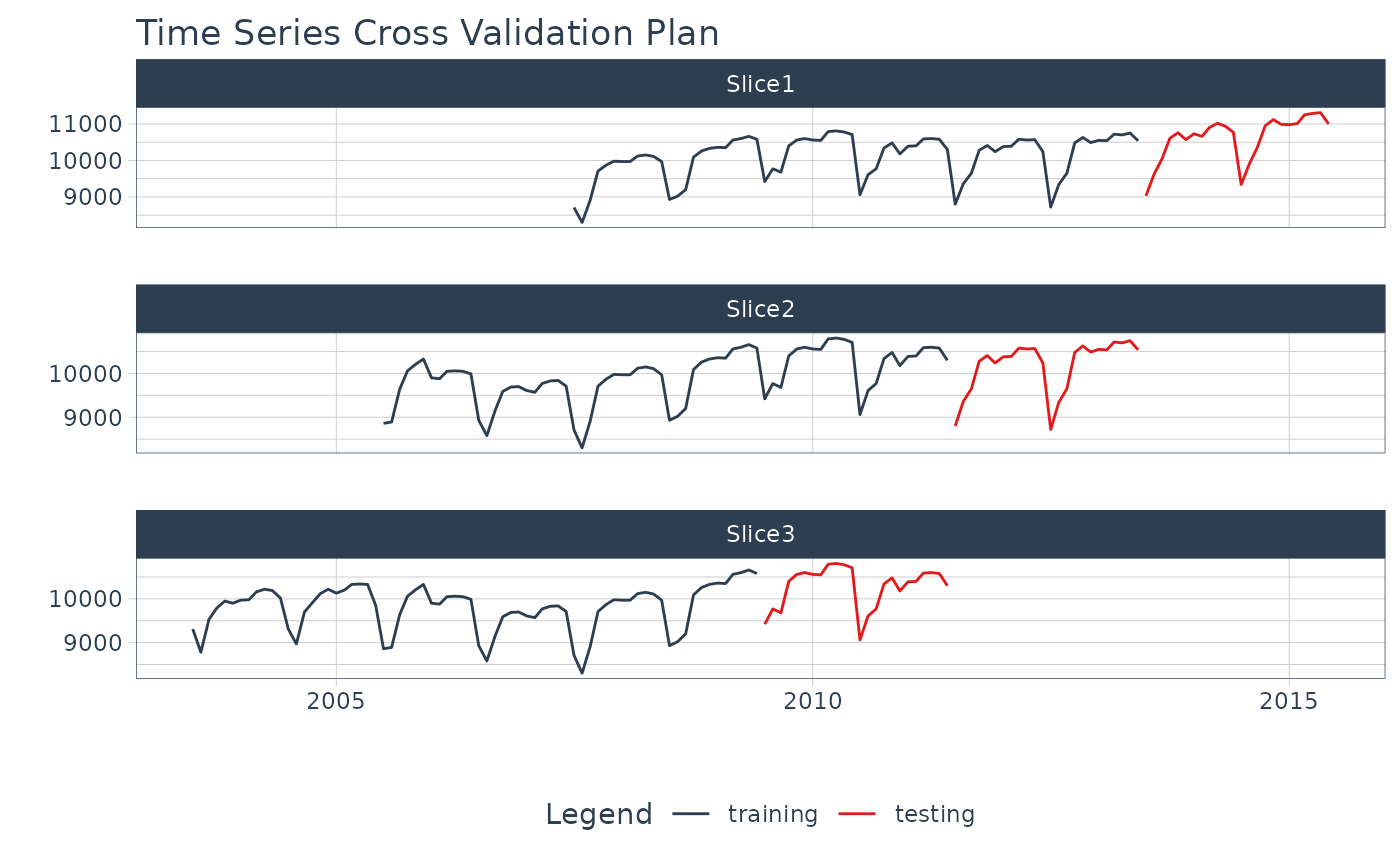

m750 <- m4_monthly %>% dplyr::filter(id == "M750")

# RESAMPLE SPEC ----

resample_spec <- time_series_cv(data = m750,

initial = "6 years",

assess = "24 months",

skip = "24 months",

cumulative = FALSE,

slice_limit = 3)

#> Using date_var: date

resample_spec

#> # Time Series Cross Validation Plan

#> # A tibble: 3 × 2

#> splits id

#> <list> <chr>

#> 1 <split [72/24]> Slice1

#> 2 <split [72/24]> Slice2

#> 3 <split [72/24]> Slice3

# VISUALIZE CV PLAN ----

# Select date and value columns from the tscv diagnostic tool

resample_spec %>% tk_time_series_cv_plan()

#> # A tibble: 288 × 5

#> .id .key id date value

#> <chr> <fct> <fct> <date> <dbl>

#> 1 Slice1 training M750 2007-07-01 8710

#> 2 Slice1 training M750 2007-08-01 8300

#> 3 Slice1 training M750 2007-09-01 8910

#> 4 Slice1 training M750 2007-10-01 9710

#> 5 Slice1 training M750 2007-11-01 9870

#> 6 Slice1 training M750 2007-12-01 9980

#> 7 Slice1 training M750 2008-01-01 9970

#> 8 Slice1 training M750 2008-02-01 9970

#> 9 Slice1 training M750 2008-03-01 10120

#> 10 Slice1 training M750 2008-04-01 10150

#> # ℹ 278 more rows

# Plot the date and value columns to see the CV Plan

resample_spec %>%

plot_time_series_cv_plan(date, value, .interactive = FALSE)

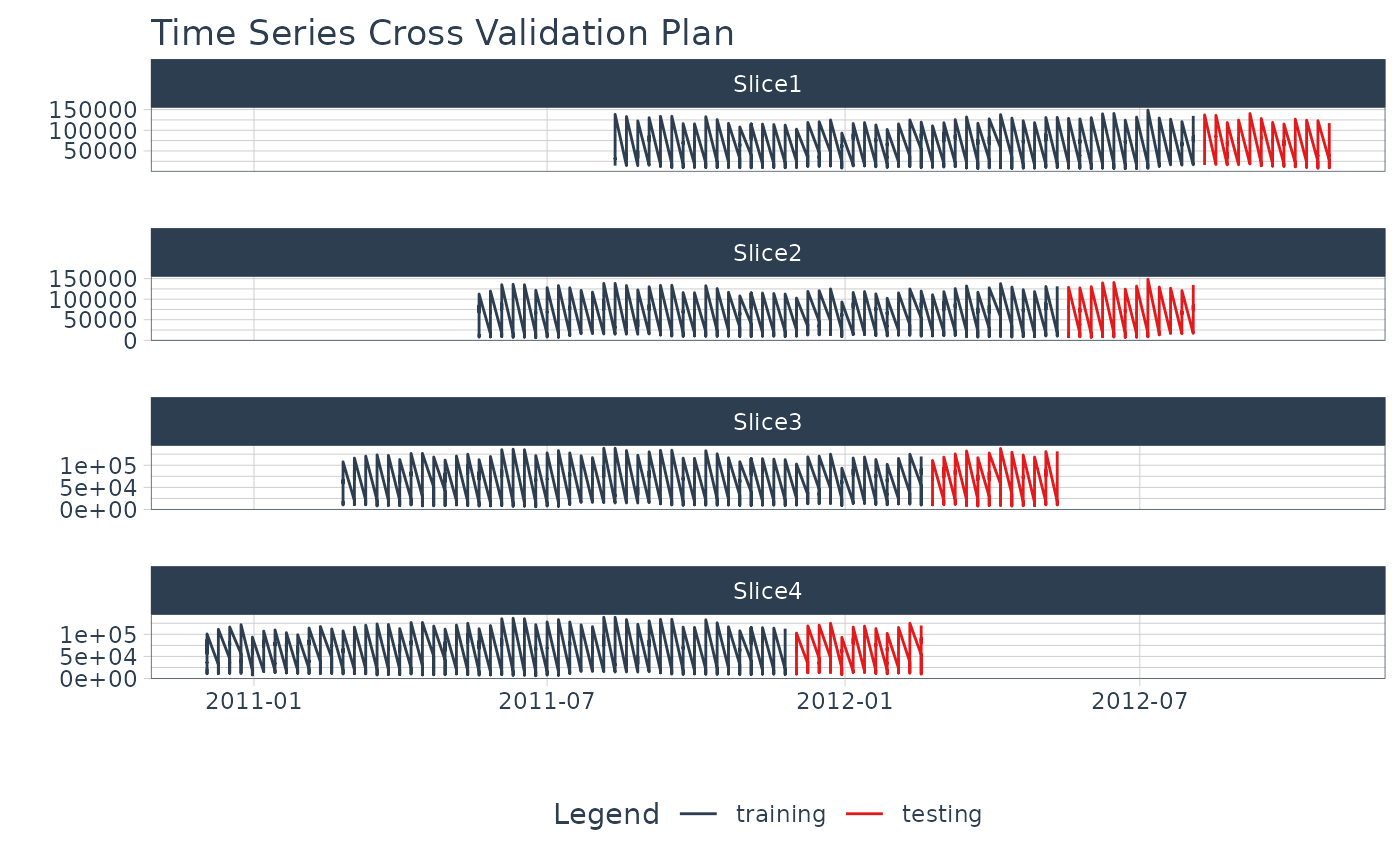

# PANEL DATA / TIME SERIES GROUPS ----

# - Time Series Groups are processed using an *ungrouped* data set

# - The data has sliding windows applied starting with the beginning of the series

# - The seven groups of weekly time series are

# processed together for <split [358/78]> dimensions

walmart_tscv <- walmart_sales_weekly %>%

time_series_cv(

date_var = Date,

initial = "12 months",

assess = "3 months",

skip = "3 months",

slice_limit = 4

)

#> Data is not ordered by the 'date_var'. Resamples will be arranged by `Date`.

#> Overlapping Timestamps Detected. Processing overlapping time series together using sliding windows.

walmart_tscv

#> # Time Series Cross Validation Plan

#> # A tibble: 4 × 2

#> splits id

#> <list> <chr>

#> 1 <split [364/84]> Slice1

#> 2 <split [364/84]> Slice2

#> 3 <split [364/84]> Slice3

#> 4 <split [364/84]> Slice4

walmart_tscv %>%

plot_time_series_cv_plan(Date, Weekly_Sales, .interactive = FALSE)

# PANEL DATA / TIME SERIES GROUPS ----

# - Time Series Groups are processed using an *ungrouped* data set

# - The data has sliding windows applied starting with the beginning of the series

# - The seven groups of weekly time series are

# processed together for <split [358/78]> dimensions

walmart_tscv <- walmart_sales_weekly %>%

time_series_cv(

date_var = Date,

initial = "12 months",

assess = "3 months",

skip = "3 months",

slice_limit = 4

)

#> Data is not ordered by the 'date_var'. Resamples will be arranged by `Date`.

#> Overlapping Timestamps Detected. Processing overlapping time series together using sliding windows.

walmart_tscv

#> # Time Series Cross Validation Plan

#> # A tibble: 4 × 2

#> splits id

#> <list> <chr>

#> 1 <split [364/84]> Slice1

#> 2 <split [364/84]> Slice2

#> 3 <split [364/84]> Slice3

#> 4 <split [364/84]> Slice4

walmart_tscv %>%

plot_time_series_cv_plan(Date, Weekly_Sales, .interactive = FALSE)