Performance Analysis with tidyquant

Matt Dancho

2026-08-01

Source:vignettes/TQ05-performance-analysis-with-tidyquant.Rmd

TQ05-performance-analysis-with-tidyquant.RmdTidy analysis of stock and portfolio return performance with

PerformanceAnalytics

Overview

Financial asset (individual stocks, securities, etc) and portfolio

(groups of stocks, securities, etc) performance analysis is a deep field

with a wide range of theories and methods for analyzing risk versus

reward. The PerformanceAnalytics package consolidates

functions to compute many of the most widely used performance metrics.

tidyquant integrates this functionality so it can be used

at scale using the split, apply, combine framework within the

tidyverse. Two primary functions integrate the performance

analysis functionality:

-

tq_performanceimplements the performance analysis functions in a tidy way, enabling scaling analysis using the split, apply, combine framework. -

tq_portfolioprovides a useful tool set for aggregating a group of individual asset returns into one or many portfolios.

This vignette aims to cover three aspects of performance analysis:

The general workflow to go from start to finish on both an asset and a portfolio level

Some of the available techniques to implement once the workflow is implemented

How to customize

tq_portfolioandtq_performanceusing the...parameter

1.0 Key Concepts

An important concept is that performance analysis is based on the

statistical properties of returns (not prices). As a

result, this package uses inputs of time-based returns as

opposed to stock prices. The arguments change to

Ra for the asset returns and Rb for the

baseline returns. We’ll go over how to get returns in the Workflow section.

Another important concept is the baseline. The

baseline is what you are measuring performance against. A baseline can

be anything, but in many cases it’s a representative average of how an

investment might perform with little or no effort. Often indexes such as

the S&P500 are used for general market performance. Other times more

specific Exchange Traded Funds (ETFs) are used such as the SPDR

Technology ETF (XLK). The important concept here is that you measure the

asset performance (Ra) against the baseline

(Rb).

Now for a quick tutorial to show off the

PerformanceAnalytics package integration.

2.0 Quick Example

One of the most widely used risk to return metrics is the Capital Asset Pricing Model (CAPM). According to Investopedia:

The capital asset pricing model (CAPM) is a model that describes the relationship between systematic risk and expected return for assets, particularly stocks. CAPM is widely used throughout finance for the pricing of risky securities, generating expected returns for assets given the risk of those assets and calculating costs of capital.

We’ll use the PerformanceAnalytics function,

table.CAPM, to evaluate the returns of several technology

stocks against the SPDR Technology ETF (XLK).

First, load the tidyquant package.

Second, get the stock returns for the stocks we wish to evaluate. We

use tq_get to get stock prices from Yahoo Finance,

group_by to group the stock prices related to each symbol,

and tq_transmute to retrieve period returns in a monthly

periodicity using the “adjusted” stock prices (adjusted for stock

splits, which can throw off returns, affecting the performance

analysis). Review the output and see that there are three groups of

symbols indicating the data has been grouped appropriately.

Ra <- c("AAPL", "GOOG", "NFLX") %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31") %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Ra")

Ra## # A tibble: 216 × 3

## # Groups: symbol [3]

## symbol date Ra

## <chr> <date> <dbl>

## 1 AAPL 2010-01-29 -0.103

## 2 AAPL 2010-02-26 0.0654

## 3 AAPL 2010-03-31 0.148

## 4 AAPL 2010-04-30 0.111

## 5 AAPL 2010-05-28 -0.0161

## 6 AAPL 2010-06-30 -0.0208

## 7 AAPL 2010-07-30 0.0227

## 8 AAPL 2010-08-31 -0.0550

## 9 AAPL 2010-09-30 0.167

## 10 AAPL 2010-10-29 0.0607

## # ℹ 206 more rowsNext, we get the baseline prices. We’ll use the XLK. Note that there is no need to group because we are just getting one data set.

Rb <- "XLK" %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31") %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Rb")

Rb## # A tibble: 72 × 2

## date Rb

## <date> <dbl>

## 1 2010-01-29 -0.0993

## 2 2010-02-26 0.0348

## 3 2010-03-31 0.0684

## 4 2010-04-30 0.0126

## 5 2010-05-28 -0.0748

## 6 2010-06-30 -0.0540

## 7 2010-07-30 0.0745

## 8 2010-08-31 -0.0561

## 9 2010-09-30 0.117

## 10 2010-10-29 0.0578

## # ℹ 62 more rowsNow, we combine the two data sets using the “date” field using

left_join from the dplyr package. Review the

results and see that we still have three groups of returns, and columns

“Ra” and “Rb” are side-by-side.

## # A tibble: 216 × 4

## # Groups: symbol [3]

## symbol date Ra Rb

## <chr> <date> <dbl> <dbl>

## 1 AAPL 2010-01-29 -0.103 -0.0993

## 2 AAPL 2010-02-26 0.0654 0.0348

## 3 AAPL 2010-03-31 0.148 0.0684

## 4 AAPL 2010-04-30 0.111 0.0126

## 5 AAPL 2010-05-28 -0.0161 -0.0748

## 6 AAPL 2010-06-30 -0.0208 -0.0540

## 7 AAPL 2010-07-30 0.0227 0.0745

## 8 AAPL 2010-08-31 -0.0550 -0.0561

## 9 AAPL 2010-09-30 0.167 0.117

## 10 AAPL 2010-10-29 0.0607 0.0578

## # ℹ 206 more rowsFinally, we can retrieve the performance metrics using

tq_performance(). You can use

tq_performance_fun_options() to see the full list of

compatible performance functions.

RaRb_capm <- RaRb %>%

tq_performance(Ra = Ra,

Rb = Rb,

performance_fun = table.CAPM)

RaRb_capm## # A tibble: 3 × 18

## # Groups: symbol [3]

## symbol ActivePremium Alpha AlphaRobust AnnualizedAlpha Beta `Beta-`

## <chr> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 AAPL 0.119 0.0089 0.0095 0.112 1.11 0.578

## 2 GOOG 0.034 0.0028 -0.0005 0.034 1.14 1.39

## 3 NFLX 0.447 0.053 0.0439 0.859 0.384 -1.52

## # ℹ 11 more variables: `Beta-Robust` <dbl>, `Beta+` <dbl>, `Beta+Robust` <dbl>,

## # BetaRobust <dbl>, Correlation <dbl>, `Correlationp-value` <dbl>,

## # InformationRatio <dbl>, `R-squared` <dbl>, `R-squaredRobust` <dbl>,

## # TrackingError <dbl>, TreynorRatio <dbl>We can quickly isolate attributes, such as alpha, the measure of growth, and beta, the measure of risk.

## # A tibble: 3 × 3

## # Groups: symbol [3]

## symbol Alpha Beta

## <chr> <dbl> <dbl>

## 1 AAPL 0.0089 1.11

## 2 GOOG 0.0028 1.14

## 3 NFLX 0.053 0.384With tidyquant it’s efficient and easy to get the CAPM

information! And, that’s just one of 129 available functions to analyze

stock and portfolio return performance. Just use

tq_performance_fun_options() to see the full list.

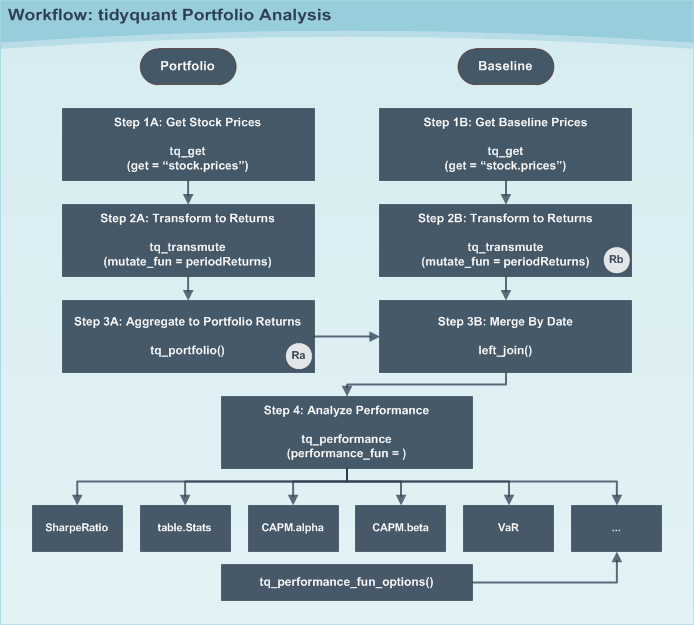

3.0 Workflow

The general workflow is shown in the diagram below. We’ll step through the workflow first with a group of individual assets (stocks) and then with portfolios of stocks.

3.1 Individual Assets

Individual assets are the simplest form of analysis because there is no portfolio aggregation (Step 3A). We’ll re-do the “Quick Example” this time getting the Sharpe Ratio, a measure of reward-to-risk.

Before we get started let’s find the performance function we want to

use from PerformanceAnalytics. Searching

tq_performance_fun_options, we can see that

SharpeRatio is available. Type ?SharpeRatio,

and we can see that the arguments are:

args(SharpeRatio)## function (R, Rf = 0, p = 0.95, FUN = c("StdDev", "VaR", "ES",

## "SemiSD"), weights = NULL, annualize = FALSE, geometric = FALSE,

## SE = FALSE, SE.control = NULL, ...)

## NULLWe can actually skip the baseline path because the function does not

require Rb. The function takes R, which is

passed using Ra in

tq_performance(Ra, Rb, performance_fun, ...). A little bit

of foresight saves us some work.

Step 1A: Get stock prices

Use tq_get() to get stock prices.

stock_prices <- c("AAPL", "GOOG", "NFLX") %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31")

stock_prices## # A tibble: 4,527 × 8

## symbol date open high low close volume adjusted

## <chr> <date> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 AAPL 2010-01-04 7.62 7.66 7.59 7.64 493729600 6.41

## 2 AAPL 2010-01-05 7.66 7.70 7.62 7.66 601904800 6.42

## 3 AAPL 2010-01-06 7.66 7.69 7.53 7.53 552160000 6.32

## 4 AAPL 2010-01-07 7.56 7.57 7.47 7.52 477131200 6.30

## 5 AAPL 2010-01-08 7.51 7.57 7.47 7.57 447610800 6.35

## 6 AAPL 2010-01-11 7.60 7.61 7.44 7.50 462229600 6.29

## 7 AAPL 2010-01-12 7.47 7.49 7.37 7.42 594459600 6.22

## 8 AAPL 2010-01-13 7.42 7.53 7.29 7.52 605892000 6.31

## 9 AAPL 2010-01-14 7.50 7.52 7.47 7.48 432894000 6.27

## 10 AAPL 2010-01-15 7.53 7.56 7.35 7.35 594067600 6.16

## # ℹ 4,517 more rowsStep 2A: Mutate to returns

Using the tidyverse split, apply, combine framework, we

can mutate groups of stocks by first “grouping” with

group_by and then applying a mutating function using

tq_transmute. We use the quantmod function

periodReturn as the mutating function. We pass along the

arguments period = "monthly" to return the results in

monthly periodicity. Last, we use the col_rename argument

to rename the output column.

stock_returns_monthly <- stock_prices %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Ra")

stock_returns_monthly## # A tibble: 216 × 3

## # Groups: symbol [3]

## symbol date Ra

## <chr> <date> <dbl>

## 1 AAPL 2010-01-29 -0.103

## 2 AAPL 2010-02-26 0.0654

## 3 AAPL 2010-03-31 0.148

## 4 AAPL 2010-04-30 0.111

## 5 AAPL 2010-05-28 -0.0161

## 6 AAPL 2010-06-30 -0.0208

## 7 AAPL 2010-07-30 0.0227

## 8 AAPL 2010-08-31 -0.0550

## 9 AAPL 2010-09-30 0.167

## 10 AAPL 2010-10-29 0.0607

## # ℹ 206 more rowsStep 3A: Aggregate to Portfolio Returns (Skipped)

Step 3A can be skipped because we are only interested in the Sharpe Ratio for individual stocks (not a portfolio).

Step 3B can also be skipped because the SharpeRatio

function from PerformanceAnalytics does not require a

baseline.

Step 4: Analyze Performance

The last step is to apply the SharpeRatio function to

our groups of stock returns. We do this using

tq_performance() with the arguments Ra = Ra,

Rb = NULL (not required), and

performance_fun = SharpeRatio. We can also pass other

arguments of the SharpeRatio function such as

Rf, p, FUN, and

annualize. We will just use the defaults for this

example.

stock_returns_monthly %>%

tq_performance(

Ra = Ra,

Rb = NULL,

performance_fun = SharpeRatio

)## # A tibble: 3 × 2

## # Groups: symbol [3]

## symbol `SharpeRatio(Rf=0%,p=95%)`

## <chr> <dbl>

## 1 AAPL 0.292

## 2 GOOG 0.203

## 3 NFLX 0.284Now we have the Sharpe Ratio for each of the three stocks. What if we want to adjust the parameters of the function? We can just add on the arguments of the underlying function.

stock_returns_monthly %>%

tq_performance(

Ra = Ra,

Rb = NULL,

performance_fun = SharpeRatio,

Rf = 0.03 / 12,

p = 0.99

)## # A tibble: 3 × 2

## # Groups: symbol [3]

## symbol `SharpeRatio(Rf=0.2%,p=99%)`

## <chr> <dbl>

## 1 AAPL 0.258

## 2 GOOG 0.170

## 3 NFLX 0.2723.2 Portfolios (Asset Groups)

Portfolios are slightly more complicated because we are now dealing

with groups of assets versus individual stocks, and we need to aggregate

weighted returns. Fortunately, this is only one extra step with

tidyquant using tq_portfolio().

Single Portfolio

Let’s recreate the CAPM analysis in the “Quick Example” this time comparing a portfolio of technology stocks to the SPDR Technology ETF (XLK).

Steps 1A and 2A: Asset Period Returns

This is the same as what we did previously to get the monthly returns

for groups of individual stock prices. We use the split, apply, combine

framework using the workflow of tq_get,

group_by, and tq_transmute.

stock_returns_monthly <- c("AAPL", "GOOG", "NFLX") %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31") %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Ra")

stock_returns_monthly## # A tibble: 216 × 3

## # Groups: symbol [3]

## symbol date Ra

## <chr> <date> <dbl>

## 1 AAPL 2010-01-29 -0.103

## 2 AAPL 2010-02-26 0.0654

## 3 AAPL 2010-03-31 0.148

## 4 AAPL 2010-04-30 0.111

## 5 AAPL 2010-05-28 -0.0161

## 6 AAPL 2010-06-30 -0.0208

## 7 AAPL 2010-07-30 0.0227

## 8 AAPL 2010-08-31 -0.0550

## 9 AAPL 2010-09-30 0.167

## 10 AAPL 2010-10-29 0.0607

## # ℹ 206 more rowsSteps 1B and 2B: Baseline Period Returns

This was also done previously.

baseline_returns_monthly <- "XLK" %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31") %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Rb")

baseline_returns_monthly## # A tibble: 72 × 2

## date Rb

## <date> <dbl>

## 1 2010-01-29 -0.0993

## 2 2010-02-26 0.0348

## 3 2010-03-31 0.0684

## 4 2010-04-30 0.0126

## 5 2010-05-28 -0.0748

## 6 2010-06-30 -0.0540

## 7 2010-07-30 0.0745

## 8 2010-08-31 -0.0561

## 9 2010-09-30 0.117

## 10 2010-10-29 0.0578

## # ℹ 62 more rowsStep 3A: Aggregate to Portfolio Period Returns

The tidyquant function, tq_portfolio()

aggregates a group of individual assets into a single return using a

weighted composition of the underlying assets. To do this we need to

first develop portfolio weights. There are two ways to do this for a

single portfolio:

- Supplying a vector of weights

- Supplying a two column tidy data frame (tibble) with stock symbols in the first column and weights to map in the second.

Suppose we want to split our portfolio evenly between AAPL and NFLX. We’ll show this using both methods.

Method 1: Aggregating a Portfolio using Vector of Weights

We’ll use the weight vector, c(0.5, 0, 0.5). Two

important aspects to supplying a numeric vector of weights: First,

notice that the length (3) is equal to the number of assets (3). This is

a requirement. Second, notice that the sum of the weighting vector is

equal to 1. This is not “required”, but is best practice. If the sum is

not 1, the weights will be distributed accordingly by scaling the vector

to 1, and a warning message will appear.

wts <- c(0.5, 0.0, 0.5)

portfolio_returns_monthly <- stock_returns_monthly %>%

tq_portfolio(assets_col = symbol,

returns_col = Ra,

weights = wts,

col_rename = "Ra")

portfolio_returns_monthly## # A tibble: 72 × 2

## date Ra

## <date> <dbl>

## 1 2010-01-29 0.0307

## 2 2010-02-26 0.0629

## 3 2010-03-31 0.130

## 4 2010-04-30 0.239

## 5 2010-05-28 0.0682

## 6 2010-06-30 -0.0219

## 7 2010-07-30 -0.0272

## 8 2010-08-31 0.116

## 9 2010-09-30 0.251

## 10 2010-10-29 0.0674

## # ℹ 62 more rowsWe now have an aggregated portfolio that is a 50/50 blend of AAPL and NFLX.

You may be asking why didn’t we use GOOG? The important thing to understand is that all of the assets from the asset returns don’t need to be used when creating the portfolio! This enables us to scale individual stock returns and then vary weights to optimize the portfolio (this will be a further subject that we address in the future!)

Method 2: Aggregating a Portfolio using Two Column tibble with Symbols and Weights

A possibly more useful method of aggregating returns is using a tibble of symbols and weights that are mapped to the portfolio. We’ll recreate the previous portfolio example using mapped weights.

## # A tibble: 2 × 2

## symbols weights

## <chr> <dbl>

## 1 AAPL 0.5

## 2 NFLX 0.5Next, supply this two column tibble, with symbols in the first column

and weights in the second, to the weights argument in

tq_performance().

stock_returns_monthly %>%

tq_portfolio(assets_col = symbol,

returns_col = Ra,

weights = wts_map,

col_rename = "Ra_using_wts_map")## # A tibble: 72 × 2

## date Ra_using_wts_map

## <date> <dbl>

## 1 2010-01-29 0.0307

## 2 2010-02-26 0.0629

## 3 2010-03-31 0.130

## 4 2010-04-30 0.239

## 5 2010-05-28 0.0682

## 6 2010-06-30 -0.0219

## 7 2010-07-30 -0.0272

## 8 2010-08-31 0.116

## 9 2010-09-30 0.251

## 10 2010-10-29 0.0674

## # ℹ 62 more rowsThe aggregated returns are exactly the same. The advantage with this method is that not all symbols need to be specified. Any symbol not specified by default gets a weight of zero.

Now, imagine if you had an entire index, such as the Russell 2000, of 2000 individual stock returns in a nice tidy data frame. It would be very easy to adjust portfolios and compute blended returns, and you only need to supply the symbols that you want to blend. All other symbols default to zero!

Step 3B: Merging Ra and Rb

Now that we have the aggregated portfolio returns (“Ra”) from Step 3A and the baseline returns (“Rb”) from Step 2B, we can merge to get our consolidated table of asset and baseline returns. Nothing new here.

RaRb_single_portfolio <- left_join(portfolio_returns_monthly,

baseline_returns_monthly,

by = "date")

RaRb_single_portfolio## # A tibble: 72 × 3

## date Ra Rb

## <date> <dbl> <dbl>

## 1 2010-01-29 0.0307 -0.0993

## 2 2010-02-26 0.0629 0.0348

## 3 2010-03-31 0.130 0.0684

## 4 2010-04-30 0.239 0.0126

## 5 2010-05-28 0.0682 -0.0748

## 6 2010-06-30 -0.0219 -0.0540

## 7 2010-07-30 -0.0272 0.0745

## 8 2010-08-31 0.116 -0.0561

## 9 2010-09-30 0.251 0.117

## 10 2010-10-29 0.0674 0.0578

## # ℹ 62 more rowsStep 4: Computing the CAPM Table

The CAPM table is computed with the function table.CAPM

from PerformanceAnalytics. We just perform the same task

that we performed in the “Quick Example”.

RaRb_single_portfolio %>%

tq_performance(Ra = Ra, Rb = Rb, performance_fun = table.CAPM)## # A tibble: 1 × 17

## ActivePremium Alpha AlphaRobust AnnualizedAlpha Beta `Beta-` `Beta-Robust`

## <dbl> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 0.327 0.0299 0.0335 0.425 0.754 -0.243 -0.203

## # ℹ 10 more variables: `Beta+` <dbl>, `Beta+Robust` <dbl>, BetaRobust <dbl>,

## # Correlation <dbl>, `Correlationp-value` <dbl>, InformationRatio <dbl>,

## # `R-squared` <dbl>, `R-squaredRobust` <dbl>, TrackingError <dbl>,

## # TreynorRatio <dbl>Now we have the CAPM performance metrics for a portfolio! While this is cool, it’s cooler to do multiple portfolios. Let’s see how.

Multiple Portfolios

Once you understand the process for a single portfolio using Step 3A, Method 2 (aggregating weights by mapping), scaling to multiple portfolios is just building on this concept. Let’s recreate the same example from the “Single Portfolio” Example this time with three portfolios:

- 50% AAPL, 25% GOOG, 25% NFLX

- 25% AAPL, 50% GOOG, 25% NFLX

- 25% AAPL, 25% GOOG, 50% NFLX

Steps 1 and 2 are the Exact Same as the Single Portfolio Example

First, get individual asset returns grouped by asset, which is the exact same as Steps 1A and 1B from the Single Portfolio example.

stock_returns_monthly <- c("AAPL", "GOOG", "NFLX") %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31") %>%

group_by(symbol) %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Ra")Second, get baseline asset returns, which is the exact same as Steps 1B and 2B from the Single Portfolio example.

baseline_returns_monthly <- "XLK" %>%

tq_get(get = "stock.prices",

from = "2010-01-01",

to = "2015-12-31") %>%

tq_transmute(select = adjusted,

mutate_fun = periodReturn,

period = "monthly",

col_rename = "Rb")Step 3A: Aggregate Portfolio Returns for Multiple Portfolios

This is where it gets fun. If you picked up on Single Portfolio, Step3A, Method 2 (mapping weights), this is just an extension for multiple portfolios.

First, we need to grow our portfolios. tidyquant has a

handy, albeit simple, function, tq_repeat_df(), for scaling

a single portfolio to many. It takes a data frame, and the number of

repeats, n, and the index_col_name, which adds

a sequential index. Let’s see how it works for our example. We need

three portfolios:

stock_returns_monthly_multi <- stock_returns_monthly %>%

tq_repeat_df(n = 3)

stock_returns_monthly_multi## # A tibble: 648 × 4

## # Groups: portfolio [3]

## portfolio symbol date Ra

## <int> <chr> <date> <dbl>

## 1 1 AAPL 2010-01-29 -0.103

## 2 1 AAPL 2010-02-26 0.0654

## 3 1 AAPL 2010-03-31 0.148

## 4 1 AAPL 2010-04-30 0.111

## 5 1 AAPL 2010-05-28 -0.0161

## 6 1 AAPL 2010-06-30 -0.0208

## 7 1 AAPL 2010-07-30 0.0227

## 8 1 AAPL 2010-08-31 -0.0550

## 9 1 AAPL 2010-09-30 0.167

## 10 1 AAPL 2010-10-29 0.0607

## # ℹ 638 more rowsExamining the results, we can see that a few things happened:

- The length (number of rows) has tripled. This is the essence of

tq_repeat_df: it grows the data frame length-wise, repeating the data framentimes. In our case,n = 3. - Our data frame, which was grouped by symbol, was ungrouped. This is

needed to prevent

tq_portfoliofrom blending on the individual stocks.tq_portfolioonly works on groups of stocks. - We have a new column, named “portfolio”. The “portfolio” column name

is a key that tells

tq_portfoliothat multiple groups exist to analyze. Just note that for multiple portfolio analysis, the “portfolio” column name is required. - We have three groups of portfolios. This is what

tq_portfoliowill split, apply (aggregate), then combine on.

Now the tricky part: We need a new table of weights to map on. There’s a few requirements:

- We must supply a three column tibble with the following columns: “portfolio”, asset, and weight in that order.

- The “portfolio” column must be named “portfolio” since this is a key name for mapping.

- The tibble must be grouped by the portfolio column.

Here’s what the weights table should look like for our example:

weights <- c(

0.50, 0.25, 0.25,

0.25, 0.50, 0.25,

0.25, 0.25, 0.50

)

stocks <- c("AAPL", "GOOG", "NFLX")

weights_table <- tibble(stocks) %>%

tq_repeat_df(n = 3) %>%

bind_cols(tibble(weights)) %>%

group_by(portfolio)

weights_table## # A tibble: 9 × 3

## # Groups: portfolio [3]

## portfolio stocks weights

## <int> <chr> <dbl>

## 1 1 AAPL 0.5

## 2 1 GOOG 0.25

## 3 1 NFLX 0.25

## 4 2 AAPL 0.25

## 5 2 GOOG 0.5

## 6 2 NFLX 0.25

## 7 3 AAPL 0.25

## 8 3 GOOG 0.25

## 9 3 NFLX 0.5Now just pass the expanded stock_returns_monthly_multi

and the weights_table to tq_portfolio for

portfolio aggregation.

portfolio_returns_monthly_multi <- stock_returns_monthly_multi %>%

tq_portfolio(assets_col = symbol,

returns_col = Ra,

weights = weights_table,

col_rename = "Ra")

portfolio_returns_monthly_multi## # A tibble: 216 × 3

## # Groups: portfolio [3]

## portfolio date Ra

## <int> <date> <dbl>

## 1 1 2010-01-29 -0.0489

## 2 1 2010-02-26 0.0482

## 3 1 2010-03-31 0.123

## 4 1 2010-04-30 0.145

## 5 1 2010-05-28 0.0245

## 6 1 2010-06-30 -0.0308

## 7 1 2010-07-30 0.000600

## 8 1 2010-08-31 0.0474

## 9 1 2010-09-30 0.222

## 10 1 2010-10-29 0.0789

## # ℹ 206 more rowsLet’s assess the output. We now have a single, “long” format data

frame of portfolio returns. It has three groups with the aggregated

portfolios blended by mapping the weights_table.

Steps 3B and 4: Merging and Assessing Performance

These steps are the exact same as the Single Portfolio example.

First, we merge with the baseline using “date” as the key.

RaRb_multiple_portfolio <- left_join(portfolio_returns_monthly_multi,

baseline_returns_monthly,

by = "date")

RaRb_multiple_portfolio## # A tibble: 216 × 4

## # Groups: portfolio [3]

## portfolio date Ra Rb

## <int> <date> <dbl> <dbl>

## 1 1 2010-01-29 -0.0489 -0.0993

## 2 1 2010-02-26 0.0482 0.0348

## 3 1 2010-03-31 0.123 0.0684

## 4 1 2010-04-30 0.145 0.0126

## 5 1 2010-05-28 0.0245 -0.0748

## 6 1 2010-06-30 -0.0308 -0.0540

## 7 1 2010-07-30 0.000600 0.0745

## 8 1 2010-08-31 0.0474 -0.0561

## 9 1 2010-09-30 0.222 0.117

## 10 1 2010-10-29 0.0789 0.0578

## # ℹ 206 more rowsFinally, we calculate the performance of each of the portfolios using

tq_performance. Make sure the data frame is grouped on

“portfolio”.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = Rb, performance_fun = table.CAPM)## # A tibble: 3 × 18

## # Groups: portfolio [3]

## portfolio ActivePremium Alpha AlphaRobust AnnualizedAlpha Beta `Beta-`

## <int> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1 0.231 0.0193 0.0237 0.258 0.908 0.312

## 2 2 0.219 0.0192 0.0244 0.256 0.886 0.436

## 3 3 0.319 0.0308 0.0335 0.439 0.721 -0.179

## # ℹ 11 more variables: `Beta-Robust` <dbl>, `Beta+` <dbl>, `Beta+Robust` <dbl>,

## # BetaRobust <dbl>, Correlation <dbl>, `Correlationp-value` <dbl>,

## # InformationRatio <dbl>, `R-squared` <dbl>, `R-squaredRobust` <dbl>,

## # TrackingError <dbl>, TreynorRatio <dbl>Inspecting the results, we now have a multiple portfolio comparison

of the CAPM table from PerformanceAnalytics. We can do the

same thing with SharpeRatio as well.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = SharpeRatio)## # A tibble: 3 × 2

## # Groups: portfolio [3]

## portfolio `SharpeRatio(Rf=0%,p=95%)`

## <int> <dbl>

## 1 1 0.355

## 2 2 0.334

## 3 3 0.3174.0 Available Functions

We’ve only scratched the surface of the analysis functions available

through PerformanceAnalytics. The list below includes all

of the compatible functions grouped by function type. The table

functions are the most useful to get a cross section of metrics. We’ll

touch on a few. We’ll also go over VaR and

SharpeRatio as these are very commonly used as performance

measures.

## $table.funs

## [1] "table.AnnualizedReturns" "table.Arbitrary"

## [3] "table.Autocorrelation" "table.CAPM"

## [5] "table.CaptureRatios" "table.Correlation"

## [7] "table.Distributions" "table.DownsideRisk"

## [9] "table.DownsideRiskRatio" "table.DrawdownsRatio"

## [11] "table.HigherMoments" "table.InformationRatio"

## [13] "table.RollingPeriods" "table.SFM"

## [15] "table.SpecificRisk" "table.Stats"

## [17] "table.TrailingPeriods" "table.UpDownRatios"

## [19] "table.Variability"

##

## $CAPM.funs

## [1] "CAPM.alpha" "CAPM.beta" "CAPM.beta.bear" "CAPM.beta.bull"

## [5] "CAPM.CML" "CAPM.CML.slope" "CAPM.dynamic" "CAPM.epsilon"

## [9] "CAPM.jensenAlpha" "CAPM.RiskPremium" "CAPM.SML.slope" "TimingRatio"

## [13] "MarketTiming"

##

## $SFM.funs

## [1] "SFM.alpha" "SFM.beta" "SFM.CML" "SFM.CML.slope"

## [5] "SFM.dynamic" "SFM.epsilon" "SFM.jensenAlpha"

##

## $descriptive.funs

## [1] "mean" "sd" "min" "max"

## [5] "cor" "mean.geometric" "mean.stderr" "mean.LCL"

## [9] "mean.UCL"

##

## $annualized.funs

## [1] "Return.annualized" "Return.annualized.excess"

## [3] "sd.annualized" "SharpeRatio.annualized"

##

## $VaR.funs

## [1] "VaR" "ES" "ETL" "CDD" "CVaR"

##

## $moment.funs

## [1] "var" "cov" "skewness" "kurtosis"

## [5] "CoVariance" "CoSkewness" "CoSkewnessMatrix" "CoKurtosis"

## [9] "CoKurtosisMatrix" "M3.MM" "M4.MM" "BetaCoVariance"

## [13] "BetaCoSkewness" "BetaCoKurtosis"

##

## $drawdown.funs

## [1] "AverageDrawdown" "AverageLength" "AverageRecovery"

## [4] "DrawdownDeviation" "DrawdownPeak" "maxDrawdown"

##

## $Bacon.risk.funs

## [1] "MeanAbsoluteDeviation" "Frequency" "SharpeRatio"

## [4] "MSquared" "MSquaredExcess" "HurstIndex"

##

## $Bacon.regression.funs

## [1] "CAPM.alpha" "CAPM.beta" "CAPM.epsilon" "CAPM.jensenAlpha"

## [5] "SystematicRisk" "SpecificRisk" "TotalRisk" "TreynorRatio"

## [9] "AppraisalRatio" "FamaBeta" "Selectivity" "NetSelectivity"

##

## $Bacon.relative.risk.funs

## [1] "ActivePremium" "ActiveReturn" "TrackingError" "InformationRatio"

##

## $Bacon.drawdown.funs

## [1] "PainIndex" "PainRatio" "CalmarRatio" "SterlingRatio"

## [5] "BurkeRatio" "MartinRatio" "UlcerIndex"

##

## $Bacon.downside.risk.funs

## [1] "DownsideDeviation" "DownsidePotential" "DownsideFrequency"

## [4] "SemiDeviation" "SemiVariance" "UpsideRisk"

## [7] "UpsidePotentialRatio" "UpsideFrequency" "BernardoLedoitRatio"

## [10] "DRatio" "Omega" "OmegaSharpeRatio"

## [13] "OmegaExcessReturn" "SortinoRatio" "M2Sortino"

## [16] "Kappa" "VolatilitySkewness" "AdjustedSharpeRatio"

## [19] "SkewnessKurtosisRatio" "ProspectRatio"

##

## $misc.funs

## [1] "KellyRatio" "Modigliani" "UpDownRatios"4.1 table.Stats

Returns a basic set of statistics that match the period of the data passed in (e.g., monthly returns will get monthly statistics, daily will be daily stats, and so on).

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = table.Stats)## # A tibble: 3 × 17

## # Groups: portfolio [3]

## portfolio ArithmeticMean GeometricMean Kurtosis `LCLMean(0.95)` Maximum Median

## <int> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1 0.0293 0.0259 1.14 0.0099 0.222 0.0307

## 2 2 0.029 0.0252 1.65 0.0086 0.227 0.037

## 3 3 0.0388 0.0313 1.81 0.01 0.370 0.046

## # ℹ 10 more variables: Minimum <dbl>, NAs <dbl>, Observations <dbl>,

## # Quartile1 <dbl>, Quartile3 <dbl>, SEMean <dbl>, Skewness <dbl>,

## # Stdev <dbl>, `UCLMean(0.95)` <dbl>, Variance <dbl>4.2 table.CAPM

Takes a set of returns and relates them to a benchmark return. Provides a set of measures related to an excess return single factor model, or CAPM.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = Rb, performance_fun = table.CAPM)## # A tibble: 3 × 18

## # Groups: portfolio [3]

## portfolio ActivePremium Alpha AlphaRobust AnnualizedAlpha Beta `Beta-`

## <int> <dbl> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1 0.231 0.0193 0.0237 0.258 0.908 0.312

## 2 2 0.219 0.0192 0.0244 0.256 0.886 0.436

## 3 3 0.319 0.0308 0.0335 0.439 0.721 -0.179

## # ℹ 11 more variables: `Beta-Robust` <dbl>, `Beta+` <dbl>, `Beta+Robust` <dbl>,

## # BetaRobust <dbl>, Correlation <dbl>, `Correlationp-value` <dbl>,

## # InformationRatio <dbl>, `R-squared` <dbl>, `R-squaredRobust` <dbl>,

## # TrackingError <dbl>, TreynorRatio <dbl>4.3 table.AnnualizedReturns

Table of Annualized Return, Annualized Std Dev, and Annualized Sharpe.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = table.AnnualizedReturns)## # A tibble: 3 × 4

## # Groups: portfolio [3]

## portfolio AnnualizedReturn `AnnualizedSharpe(Rf=0%)` AnnualizedStdDev

## <int> <dbl> <dbl> <dbl>

## 1 1 0.360 1.26 0.286

## 2 2 0.348 1.16 0.301

## 3 3 0.448 1.06 0.4244.4 table.Correlation

This is a wrapper for calculating correlation and significance against each column of the data provided.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = Rb, performance_fun = table.Correlation)## # A tibble: 3 × 5

## # Groups: portfolio [3]

## portfolio `p-value` `Lower CI` `Upper CI` to.Rb

## <int> <dbl> <dbl> <dbl> <dbl>

## 1 1 0.0000284 0.270 0.634 0.472

## 2 2 0.000122 0.229 0.608 0.438

## 3 3 0.0325 0.0220 0.457 0.2524.5 table.DownsideRisk

Creates a table of estimates of downside risk measures for comparison across multiple instruments or funds.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = table.DownsideRisk)## # A tibble: 3 × 12

## # Groups: portfolio [3]

## portfolio DownsideDeviation(0%…¹ DownsideDeviation(MA…² DownsideDeviation(Rf…³

## <int> <dbl> <dbl> <dbl>

## 1 1 0.045 0.0488 0.045

## 2 2 0.0501 0.0538 0.0501

## 3 3 0.0684 0.0721 0.0684

## # ℹ abbreviated names: ¹`DownsideDeviation(0%)`, ²`DownsideDeviation(MAR=10%)`,

## # ³`DownsideDeviation(Rf=0%)`

## # ℹ 8 more variables: GainDeviation <dbl>, `HistoricalES(95%)` <dbl>,

## # `HistoricalVaR(95%)` <dbl>, LossDeviation <dbl>, MaximumDrawdown <dbl>,

## # `ModifiedES(95%)` <dbl>, `ModifiedVaR(95%)` <dbl>, SemiDeviation <dbl>4.6 table.DownsideRiskRatio

Table of Monthly downside risk, Annualized downside risk, Downside potential, Omega, Sortino ratio, Upside potential, Upside potential ratio and Omega-Sharpe ratio.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = table.DownsideRiskRatio)## # A tibble: 3 × 9

## # Groups: portfolio [3]

## portfolio Annualiseddownsiderisk Downsidepotential monthlydownsiderisk Omega

## <int> <dbl> <dbl> <dbl> <dbl>

## 1 1 0.156 0.0198 0.045 2.48

## 2 2 0.173 0.0217 0.0501 2.34

## 3 3 0.237 0.0294 0.0684 2.32

## # ℹ 4 more variables: `Omega-sharperatio` <dbl>, Sortinoratio <dbl>,

## # Upsidepotential <dbl>, Upsidepotentialratio <dbl>4.7 table.HigherMoments

Summary of the higher moments and Co-Moments of the return distribution. Used to determine diversification potential. Also called “systematic” moments by several papers.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = Rb, performance_fun = table.HigherMoments)## # A tibble: 3 × 6

## # Groups: portfolio [3]

## portfolio BetaCoKurtosis BetaCoSkewness BetaCoVariance CoKurtosis CoSkewness

## <int> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 1 0.756 0.196 0.908 0 0

## 2 2 0.772 1.71 0.886 0 0

## 3 3 0.455 0.369 0.721 0 04.8 table.InformationRatio

Table of Tracking error, Annualized tracking error and Information ratio.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = Rb, performance_fun = table.InformationRatio)## # A tibble: 3 × 4

## # Groups: portfolio [3]

## portfolio AnnualisedTrackingError InformationRatio TrackingError

## <int> <dbl> <dbl> <dbl>

## 1 1 0.252 0.917 0.0728

## 2 2 0.271 0.809 0.0782

## 3 3 0.412 0.774 0.1194.9 table.Variability

Table of Mean absolute difference, Monthly standard deviation and annualized standard deviation.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = table.Variability)## # A tibble: 3 × 4

## # Groups: portfolio [3]

## portfolio AnnualizedStdDev MeanAbsolutedeviation monthlyStdDev

## <int> <dbl> <dbl> <dbl>

## 1 1 0.286 0.0658 0.0825

## 2 2 0.301 0.0679 0.0868

## 3 3 0.424 0.091 0.1224.10 VaR

Calculates Value-at-Risk (VaR) for univariate, component, and marginal cases using a variety of analytical methods.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = VaR)## # A tibble: 3 × 2

## # Groups: portfolio [3]

## portfolio VaR

## <int> <dbl>

## 1 1 -0.111

## 2 2 -0.123

## 3 3 -0.1634.11 SharpeRatio

The Sharpe ratio is simply the return per unit of risk (represented by variability). In the classic case, the unit of risk is the standard deviation of the returns.

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra, Rb = NULL, performance_fun = SharpeRatio)## # A tibble: 3 × 2

## # Groups: portfolio [3]

## portfolio `SharpeRatio(Rf=0%,p=95%)`

## <int> <dbl>

## 1 1 0.355

## 2 2 0.334

## 3 3 0.3175.0 Customizing using the …

One of the best features of tq_portfolio and

tq_performance is to be able to pass features through to

the underlying functions. After all, these are just wrappers for

PerformanceAnalytics, so you probably want to be able

to make full use of the underlying functions. Passing

through parameters using the ... can be incredibly useful,

so let’s see how.

5.1 Customizing tq_portfolio

The tq_portfolio function is a wrapper for

Return.portfolio. This means that during the portfolio

aggregation process, we can make use of most of the

Return.portfolio arguments such as

wealth.index, contribution,

geometric, rebalance_on, and

value. Here’s the arguments of the underlying function:

args(Return.portfolio)## function (R, weights = NULL, wealth.index = FALSE, contribution = FALSE,

## geometric = TRUE, rebalance_on = c(NA, "years", "quarters",

## "months", "weeks", "days"), value = 1, verbose = FALSE,

## ..., rebal_cost = 0, full_investment = FALSE)

## NULLLet’s see an example of passing parameters to the ....

Suppose we want to instead see how our money is grows for a $10,000

investment. We’ll use the “Single Portfolio” example, where our

portfolio mix was 50% AAPL, 0% GOOG, and 50% NFLX.

Method 3A, Aggregating Portfolio Returns, showed us two methods to aggregate for a single portfolio. Either will work for this example. For simplicity, we’ll examine the first.

Here’s the original output, without adjusting parameters.

wts <- c(0.5, 0.0, 0.5)

portfolio_returns_monthly <- stock_returns_monthly %>%

tq_portfolio(assets_col = symbol,

returns_col = Ra,

weights = wts,

col_rename = "Ra")

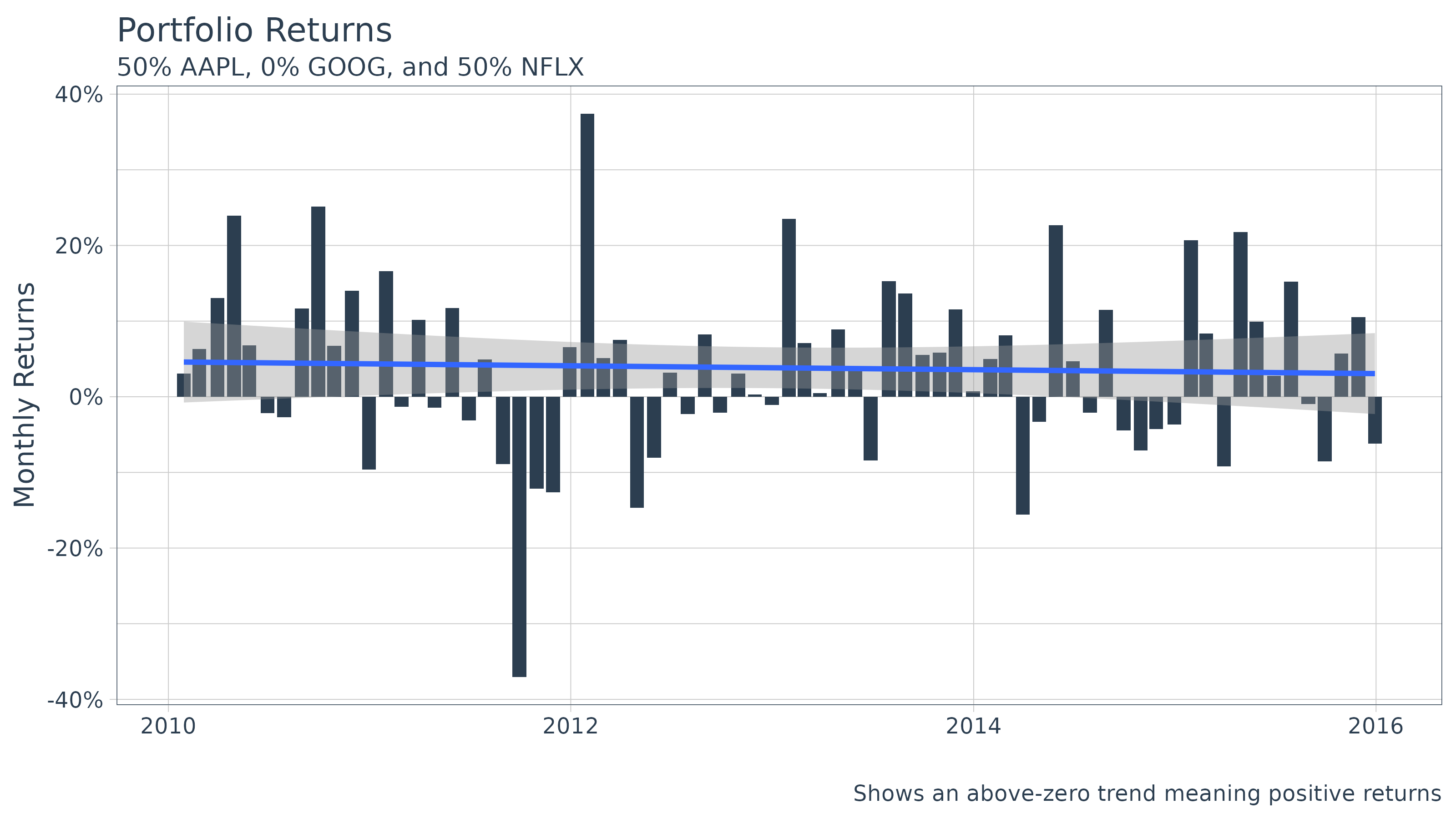

portfolio_returns_monthly %>%

ggplot(aes(x = date, y = Ra)) +

geom_bar(stat = "identity", fill = palette_light()[[1]]) +

labs(title = "Portfolio Returns",

subtitle = "50% AAPL, 0% GOOG, and 50% NFLX",

caption = "Shows an above-zero trend meaning positive returns",

x = "", y = "Monthly Returns") +

geom_smooth(method = "lm") +

theme_tq() +

scale_color_tq() +

scale_y_continuous(labels = scales::percent)

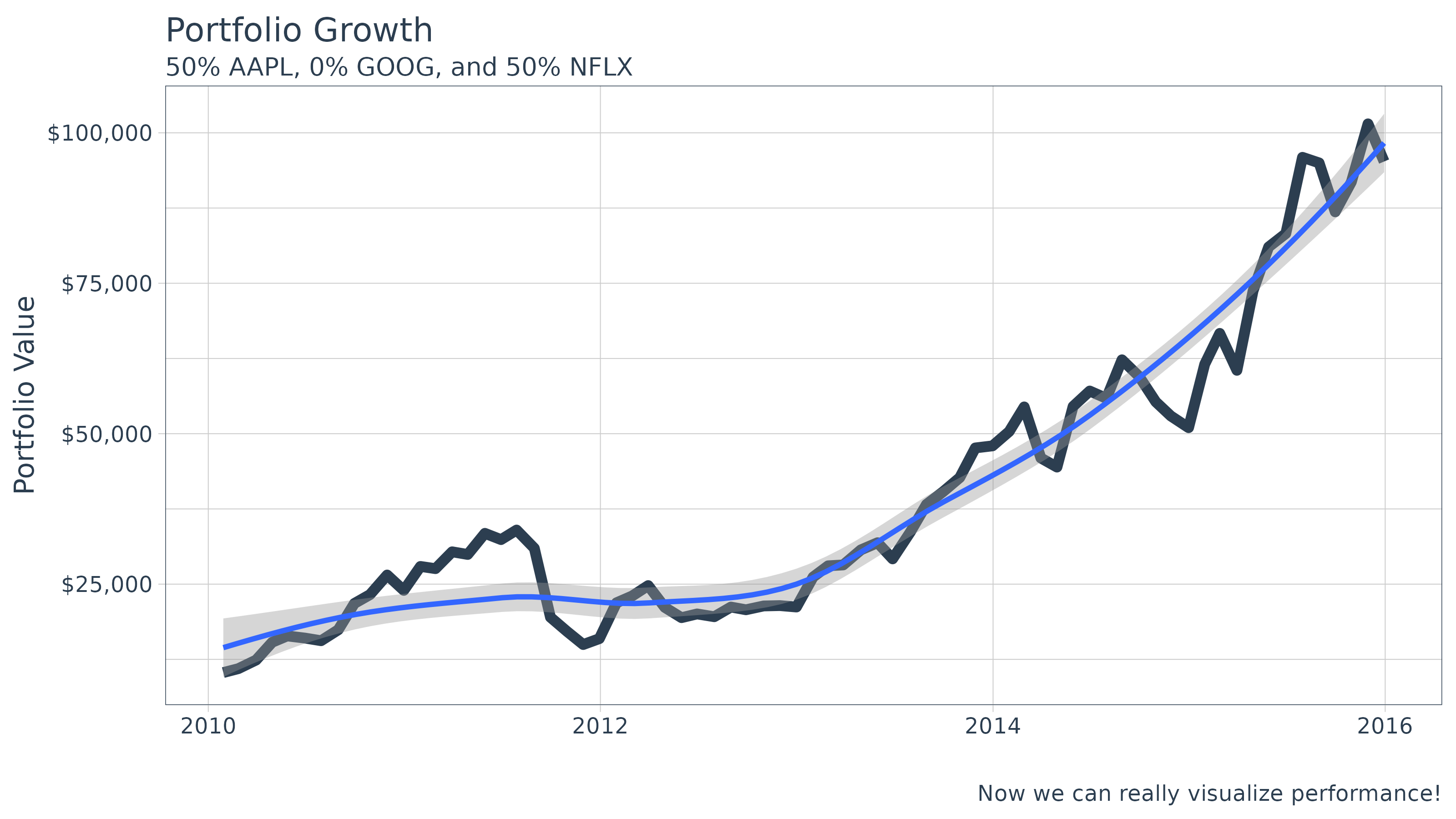

This is good, but we want to see how our $10,000 initial investment

is growing. This is simple with the underlying

Return.portfolio argument,

wealth.index = TRUE. All we need to do is add these as

additional parameters to tq_portfolio!

wts <- c(0.5, 0, 0.5)

portfolio_growth_monthly <- stock_returns_monthly %>%

tq_portfolio(assets_col = symbol,

returns_col = Ra,

weights = wts,

col_rename = "investment.growth",

wealth.index = TRUE) %>%

mutate(investment.growth = investment.growth * 10000)

portfolio_growth_monthly %>%

ggplot(aes(x = date, y = investment.growth)) +

geom_line(linewidth = 2, color = palette_light()[[1]]) +

labs(title = "Portfolio Growth",

subtitle = "50% AAPL, 0% GOOG, and 50% NFLX",

caption = "Now we can really visualize performance!",

x = "", y = "Portfolio Value") +

geom_smooth(method = "loess") +

theme_tq() +

scale_color_tq() +

scale_y_continuous(labels = scales::dollar)

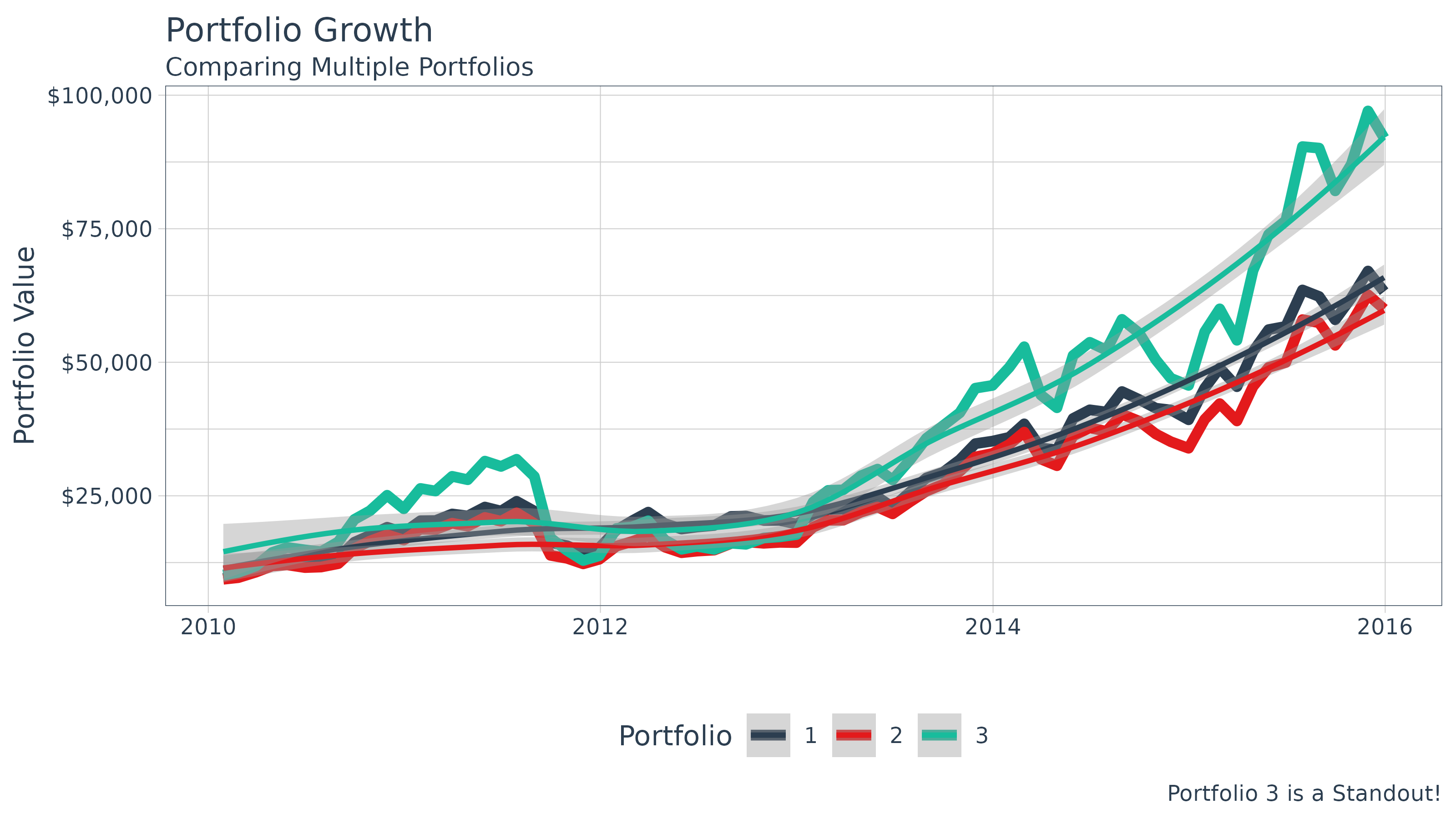

Finally, taking this one step further, we apply the same process to the “Multiple Portfolio” example:

- 50% AAPL, 25% GOOG, 25% NFLX

- 25% AAPL, 50% GOOG, 25% NFLX

- 25% AAPL, 25% GOOG, 50% NFLX

portfolio_growth_monthly_multi <- stock_returns_monthly_multi %>%

tq_portfolio(assets_col = symbol,

returns_col = Ra,

weights = weights_table,

col_rename = "investment.growth",

wealth.index = TRUE) %>%

mutate(investment.growth = investment.growth * 10000)

portfolio_growth_monthly_multi %>%

ggplot(aes(x = date, y = investment.growth, color = factor(portfolio))) +

geom_line(linewidth = 2) +

labs(title = "Portfolio Growth",

subtitle = "Comparing Multiple Portfolios",

caption = "Portfolio 3 is a Standout!",

x = "", y = "Portfolio Value",

color = "Portfolio") +

geom_smooth(method = "loess") +

theme_tq() +

scale_color_tq() +

scale_y_continuous(labels = scales::dollar)

5.2 Customizing tq_performance

Finally, the same concept of passing arguments works with all the

tidyquant functions that are wrappers including

tq_transmute, tq_mutate,

tq_performance, etc. Let’s use a final example with the

SharpeRatio, which has the following arguments.

args(SharpeRatio)## function (R, Rf = 0, p = 0.95, FUN = c("StdDev", "VaR", "ES",

## "SemiSD"), weights = NULL, annualize = FALSE, geometric = FALSE,

## SE = FALSE, SE.control = NULL, ...)

## NULLWe can see that the parameters Rf allows us to apply a

risk-free rate and p allows us to vary the confidence

interval. Let’s compare the Sharpe ratio with an annualized risk-free

rate of 3% and a confidence interval of 0.99.

Default:

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra,

performance_fun = SharpeRatio)## # A tibble: 3 × 2

## # Groups: portfolio [3]

## portfolio `SharpeRatio(Rf=0%,p=95%)`

## <int> <dbl>

## 1 1 0.355

## 2 2 0.334

## 3 3 0.317With Rf = 0.03 / 12 (adjusted for monthly

periodicity):

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra,

performance_fun = SharpeRatio,

Rf = 0.03 / 12)## # A tibble: 3 × 2

## # Groups: portfolio [3]

## portfolio `SharpeRatio(Rf=0.2%,p=95%)`

## <int> <dbl>

## 1 1 0.325

## 2 2 0.305

## 3 3 0.296And, with both Rf = 0.03 / 12 (adjusted for monthly

periodicity) and p = 0.99:

RaRb_multiple_portfolio %>%

tq_performance(Ra = Ra,

performance_fun = SharpeRatio,

Rf = 0.03 / 12,

p = 0.99)## # A tibble: 3 × 2

## # Groups: portfolio [3]

## portfolio `SharpeRatio(Rf=0.2%,p=99%)`

## <int> <dbl>

## 1 1 0.325

## 2 2 0.305

## 3 3 0.296