![]()

Forecasting with modeltime.h2o made easy! This short

tutorial shows how you can use:

H2O AutoML for forecasting implemented via

automl_reg(). This function trains and cross-validates multiple machine learning and deep learning models (XGBoost GBM, GLMs, Random Forest, GBMs…) and then trains two Stacked Ensembled models, one of all the models, and one of only the best models of each kind. Finally, the best model is selected based on a stopping metric. And we take care of all this for you!Save & Load Models functionality to ensure the persistence of your models.

Collect data and split into training and test sets

Next, we load the walmart_sales_weekly data containing 7

time series and visualize them using the

timetk::plot_time_series() function.

data_tbl <- walmart_sales_weekly %>%

select(id, Date, Weekly_Sales)

data_tbl %>%

group_by(id) %>%

plot_time_series(

.date_var = Date,

.value = Weekly_Sales,

.facet_ncol = 2,

.smooth = F,

.interactive = F

)

Then, we separate the data with the time_series_split()

function and generate a training dataset and a test one.

splits <- time_series_split(data_tbl, assess = "3 month", cumulative = TRUE)

recipe_spec <- recipe(Weekly_Sales ~ ., data = training(splits)) %>%

step_timeseries_signature(Date)

train_tbl <- training(splits) %>% bake(prep(recipe_spec), .)

test_tbl <- testing(splits) %>% bake(prep(recipe_spec), .)Model specification, training and prediction

In order to correctly use modeltime.h2o, it is necessary to connect

to an H2O cluster through the h2o.init() function. You can

find more information on how to set up the cluster by typing

?h2o.init or by visiting the official

site.

# Initialize H2O

h2o.init(

nthreads = -1,

ip = 'localhost',

port = 54321

)

#>

#> H2O is not running yet, starting it now...

#>

#> Note: In case of errors look at the following log files:

#> /tmp/RtmpD7NvJJ/file217c797e529f/h2o_runner_started_from_r.out

#> /tmp/RtmpD7NvJJ/file217c77a3486f/h2o_runner_started_from_r.err

#>

#>

#> Starting H2O JVM and connecting: .... Connection successful!

#>

#> R is connected to the H2O cluster:

#> H2O cluster uptime: 1 seconds 919 milliseconds

#> H2O cluster timezone: UTC

#> H2O data parsing timezone: UTC

#> H2O cluster version: 3.42.0.2

#> H2O cluster version age: 5 months and 10 days

#> H2O cluster name: H2O_started_from_R_runner_wle394

#> H2O cluster total nodes: 1

#> H2O cluster total memory: 3.90 GB

#> H2O cluster total cores: 4

#> H2O cluster allowed cores: 4

#> H2O cluster healthy: TRUE

#> H2O Connection ip: localhost

#> H2O Connection port: 54321

#> H2O Connection proxy: NA

#> H2O Internal Security: FALSE

#> R Version: R version 4.3.2 (2023-10-31)

# Optional - Set H2O No Progress to remove progress bars

h2o.no_progress()Now comes the fun part! We define our model specification with the

automl_reg() function and pass the arguments through the

engine:

model_spec <- automl_reg(mode = 'regression') %>%

set_engine(

engine = 'h2o',

max_runtime_secs = 5,

max_runtime_secs_per_model = 3,

max_models = 3,

nfolds = 5,

exclude_algos = c("DeepLearning"),

verbosity = NULL,

seed = 786

)

model_spec

#> H2O AutoML Model Specification (regression)

#>

#> Engine-Specific Arguments:

#> max_runtime_secs = 5

#> max_runtime_secs_per_model = 3

#> max_models = 3

#> nfolds = 5

#> exclude_algos = c("DeepLearning")

#> verbosity = NULL

#> seed = 786

#>

#> Computational engine: h2oNext, let’s train the model with fit()!

model_fitted <- model_spec %>%

fit(Weekly_Sales ~ ., data = train_tbl)

#> model_id rmse mse

#> 1 XGBoost_1_AutoML_1_20240104_204414 6368.842 40562143

#> 2 StackedEnsemble_BestOfFamily_1_AutoML_1_20240104_204414 6371.445 40595317

#> 3 GBM_1_AutoML_1_20240104_204414 7607.165 57868955

#> 4 GLM_1_AutoML_1_20240104_204414 36255.636 1314471115

#> mae rmsle mean_residual_deviance

#> 1 4175.752 0.1753395 40562143

#> 2 4107.600 0.1690209 40595317

#> 3 5125.090 0.2115567 57868955

#> 4 31032.413 0.8352711 1314471115

#>

#> [4 rows x 6 columns]

model_fitted

#> parsnip model object

#>

#>

#> H2O AutoML - Xgboost

#> --------

#> Model: Model Details:

#> ==============

#>

#> H2ORegressionModel: xgboost

#> Model ID: XGBoost_1_AutoML_1_20240104_204414

#> Model Summary:

#> number_of_trees

#> 1 44

#>

#>

#> H2ORegressionMetrics: xgboost

#> ** Reported on training data. **

#>

#> MSE: 8905205

#> RMSE: 2984.159

#> MAE: 2011.225

#> RMSLE: 0.09321704

#> Mean Residual Deviance : 8905205

#>

#>

#>

#> H2ORegressionMetrics: xgboost

#> ** Reported on cross-validation data. **

#> ** 5-fold cross-validation on training data (Metrics computed for combined holdout predictions) **

#>

#> MSE: 40562143

#> RMSE: 6368.842

#> MAE: 4175.752

#> RMSLE: 0.1753395

#> Mean Residual Deviance : 40562143

#>

#>

#> Cross-Validation Metrics Summary:

#> mean sd cv_1_valid

#> mae 4175.762000 272.333200 3890.696000

#> mean_residual_deviance 40559876.000000 11151054.000000 28802630.000000

#> mse 40559876.000000 11151054.000000 28802630.000000

#> r2 0.969156 0.008390 0.977998

#> residual_deviance 40559876.000000 11151054.000000 28802630.000000

#> rmse 6320.693400 872.290200 5366.808000

#> rmsle 0.174745 0.016217 0.153008

#> cv_2_valid cv_3_valid cv_4_valid

#> mae 4450.958500 4100.722700 4473.589400

#> mean_residual_deviance 54395072.000000 37792108.000000 49844588.000000

#> mse 54395072.000000 37792108.000000 49844588.000000

#> r2 0.958720 0.971498 0.962121

#> residual_deviance 54395072.000000 37792108.000000 49844588.000000

#> rmse 7375.302000 6147.529000 7060.070000

#> rmsle 0.189853 0.171167 0.191813

#> cv_5_valid

#> mae 3962.845000

#> mean_residual_deviance 31964988.000000

#> mse 31964988.000000

#> r2 0.975442

#> residual_deviance 31964988.000000

#> rmse 5653.759000

#> rmsle 0.167883The best models are stored in the leaderbord and by

default the one with the best metric with which you have decided to sort

the leaderbord is selected (this behavior can be controlled with the

sort_metric parameter passed through set_engine. For more

information see ?h2o.automl. By default, it is sorted by the

mean_residual_deviance). To list the models created during training that

have finally been stored in the leaderbord you can use the

automl_leaderbord function as follows:

automl_leaderboard(model_fitted)

#> # A tibble: 4 × 6

#> model_id rmse mse mae rmsle mean_residual_deviance

#> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

#> 1 XGBoost_1_AutoML_1_20240104… 6369. 4.06e7 4176. 0.175 40562143.

#> 2 StackedEnsemble_BestOfFamil… 6371. 4.06e7 4108. 0.169 40595317.

#> 3 GBM_1_AutoML_1_20240104_204… 7607. 5.79e7 5125. 0.212 57868955.

#> 4 GLM_1_AutoML_1_20240104_204… 36256. 1.31e9 31032. 0.835 1314471115.To change the default selected model (remember, the first one sorted

according to the selected metric) you can do it with the

automl_update_model() function as follows (do not run the

following example as the model id name will have changed as there is

randomness in the process):

automl_update_model(model_fitted, model_id = "StackedEnsemble_AllModels_AutoML_20210319_204825")Finally, we predict() on the test dataset:

predict(model_fitted, test_tbl)

#> # A tibble: 84 × 1

#> .pred

#> <dbl>

#> 1 19484.

#> 2 33369.

#> 3 37997.

#> 4 40721.

#> 5 70083.

#> 6 81469.

#> 7 136557.

#> 8 14242.

#> 9 34078.

#> 10 35966.

#> # ℹ 74 more rowsModeltime Workflow

Once we have our fitted model, we can follow the Modeltime Workflow:

Add fitted models to a Model Table.

Calibrate the models to a testing set.

Perform Testing Set Forecast Evaluation & Accuracy Evaluation.

Refit the models to Full Dataset & Forecast Forward

Add fitted models to a Model Table

First, we create the model table:

modeltime_tbl <- modeltime_table(

model_fitted

)

modeltime_tbl

#> # Modeltime Table

#> # A tibble: 1 × 3

#> .model_id .model .model_desc

#> <int> <list> <chr>

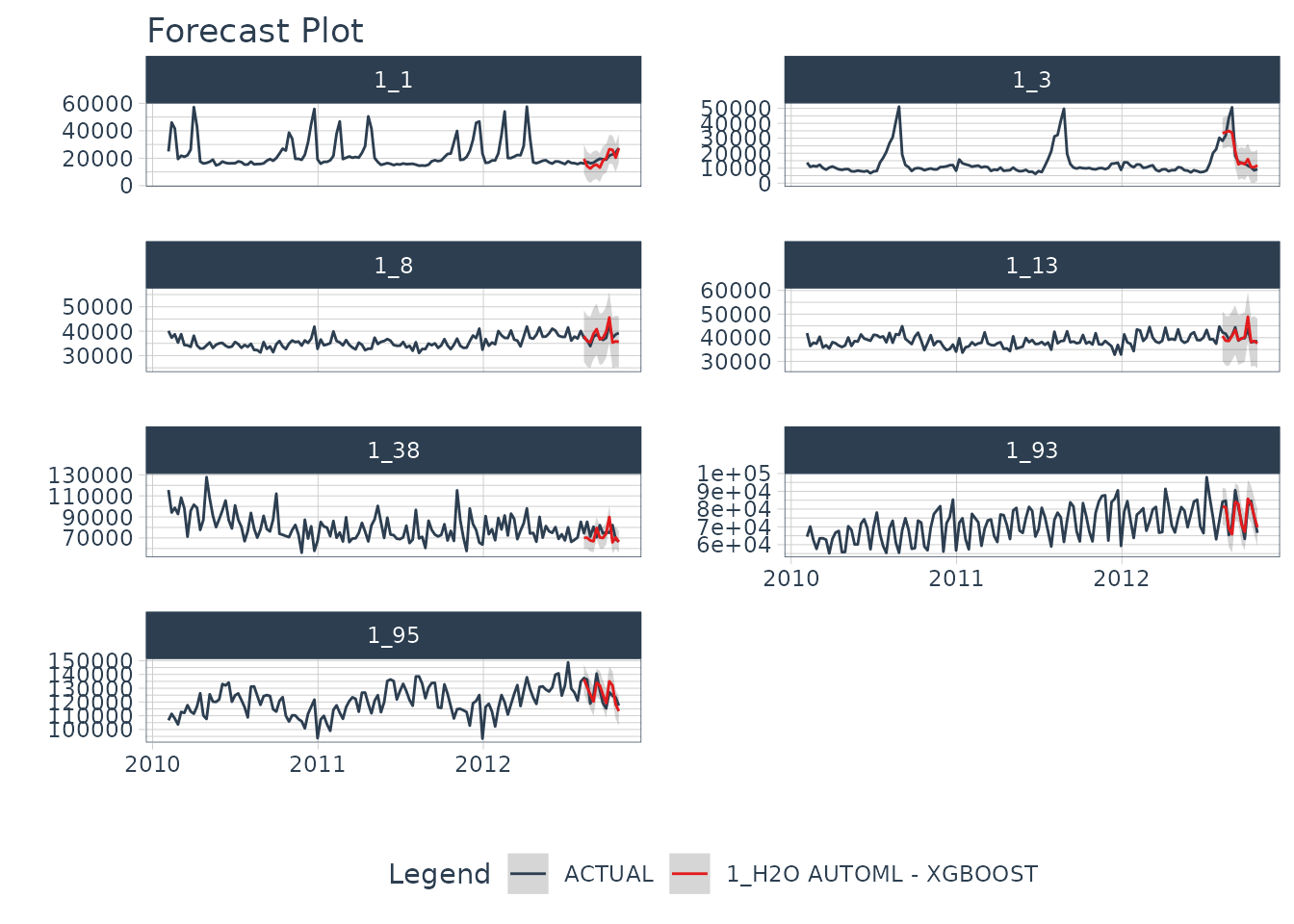

#> 1 1 <fit[+]> H2O AUTOML - XGBOOSTCalibrate & Testing Set Forecast & Accuracy Evaluation

Next, we calibrate to the testing set and visualize the forecasts:

modeltime_tbl %>%

modeltime_calibrate(test_tbl) %>%

modeltime_forecast(

new_data = test_tbl,

actual_data = data_tbl,

keep_data = TRUE

) %>%

group_by(id) %>%

plot_modeltime_forecast(

.facet_ncol = 2,

.interactive = FALSE

)

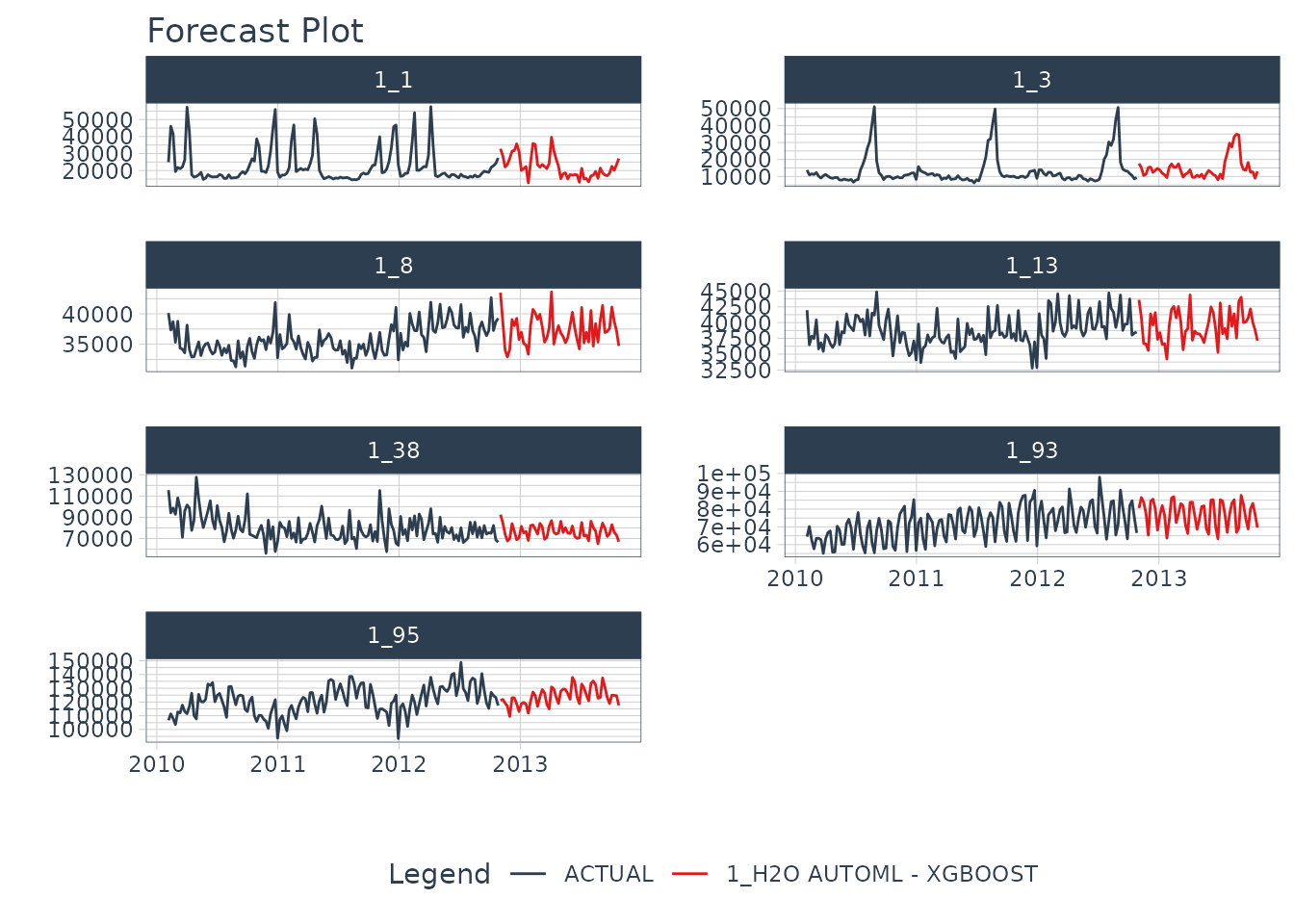

Refit to Full Dataset & Forecast Forward

Before using refit on our dataset, let’s prepare our

data. We create data_prepared_tbl which represents the

complete dataset (the union of train and test) with the variables

created with the recipe named recipe_spec. Subsequently, we create the

dataset future_prepared_tbl that represents the dataset

with the future data to one year and the required variables.

data_prepared_tbl <- bind_rows(train_tbl, test_tbl)

future_tbl <- data_prepared_tbl %>%

group_by(id) %>%

future_frame(.length_out = "1 year") %>%

ungroup()

future_prepared_tbl <- bake(prep(recipe_spec), future_tbl)Finally, we use forecast in our future dataset and visualize the results once we had reffited.

refit_tbl <- modeltime_tbl %>%

modeltime_refit(data_prepared_tbl)

#> model_id rmse mse

#> 1 XGBoost_1_AutoML_2_20240104_204427 6060.518 36729882

#> 2 StackedEnsemble_BestOfFamily_1_AutoML_2_20240104_204427 6061.512 36741927

#> 3 GBM_1_AutoML_2_20240104_204427 7524.808 56622738

#> 4 GLM_1_AutoML_2_20240104_204427 36259.518 1314752625

#> mae rmsle mean_residual_deviance

#> 1 4075.988 0.1677377 36729882

#> 2 3998.426 0.1604279 36741927

#> 3 5163.899 0.2088567 56622738

#> 4 31017.107 0.8289850 1314752625

#>

#> [4 rows x 6 columns]

refit_tbl %>%

modeltime_forecast(

new_data = future_prepared_tbl,

actual_data = data_prepared_tbl,

keep_data = TRUE

) %>%

group_by(id) %>%

plot_modeltime_forecast(

.facet_ncol = 2,

.interactive = FALSE

)

We can likely do better than this if we train longer but really good for a quick example!

Saving and Loading Models

H2O models will need to “serialized” (a fancy word for saved to a

directory that contains the recipe for recreating the models). To save

the models, use save_h2o_model().

- Provide a directory where you want to save the model.

- This saves the model file in the directory.

model_fitted %>%

save_h2o_model(path = "../model_fitted", overwrite = TRUE)You can reload the model into R using

load_h2o_model().

model_h2o <- load_h2o_model(path = "../model_fitted/")Shut down H2O when finished

Finally, once we have saved the specific models that we want to keep, we shutdown the H2O cluster.

h2o.shutdown(prompt = FALSE)Need to learn high-performance time series forecasting?

Take the High-Performance Forecasting Course

Become the forecasting expert for your organization

High-Performance Time Series Course

Time Series is Changing

Time series is changing. Businesses now need 10,000+ time series forecasts every day. This is what I call a High-Performance Time Series Forecasting System (HPTSF) - Accurate, Robust, and Scalable Forecasting.

High-Performance Forecasting Systems will save companies by improving accuracy and scalability. Imagine what will happen to your career if you can provide your organization a “High-Performance Time Series Forecasting System” (HPTSF System).

How to Learn High-Performance Time Series Forecasting

I teach how to build a HPTFS System in my High-Performance Time Series Forecasting Course. You will learn:

-

Time Series Machine Learning (cutting-edge) with

Modeltime- 30+ Models (Prophet, ARIMA, XGBoost, Random Forest, & many more) -

Deep Learning with

GluonTS(Competition Winners) - Time Series Preprocessing, Noise Reduction, & Anomaly Detection

- Feature engineering using lagged variables & external regressors

- Hyperparameter Tuning

- Time series cross-validation

- Ensembling Multiple Machine Learning & Univariate Modeling Techniques (Competition Winner)

- Scalable Forecasting - Forecast 1000+ time series in parallel

- and more.

Become the Time Series Expert for your organization.