GluonTS Deep Learning in R.

GluonTS Deep Learning in R

Modeltime GluonTS integrates the Python GluonTS Deep Learning Library, making it easy to develop forecasts using Deep Learning for those that are comfortable with the Modeltime Forecasting Workflow.

Installation Requirements

Important: This package is being maintained on GitHub (not CRAN). Please install the GitHub version, which is updated with the latest features:

# Install GitHub Version

remotes::install_github("business-science/modeltime.gluonts")

# Install Python Dependencies

modeltime.gluonts::install_gluonts()For more detailed installation instructions and troubleshooting guidance, visit our Installation Guide.

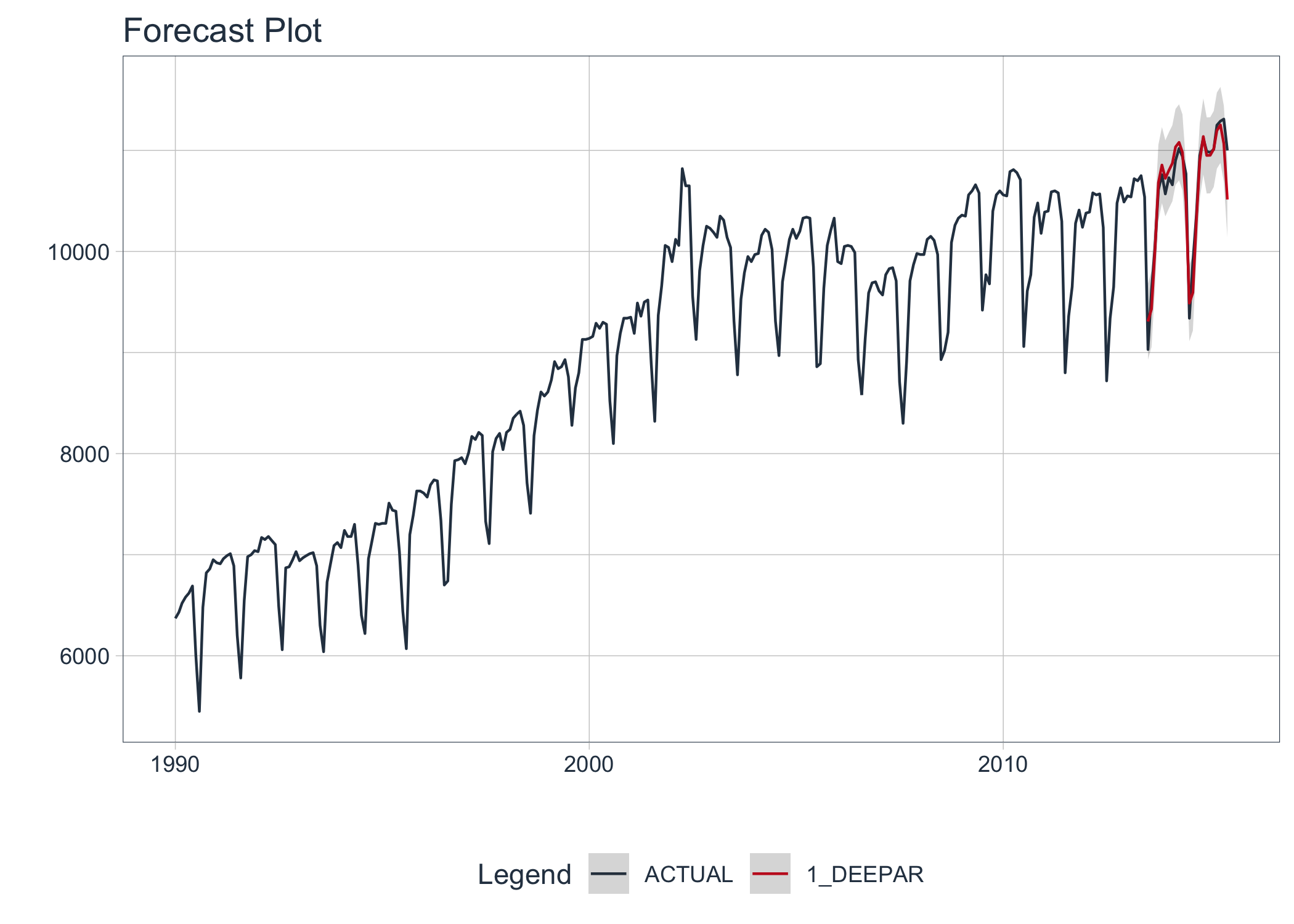

Make Your First DeepAR Model

Make your first deep_ar() model, which connects to the GluonTS DeepAREstimator(). For a more detailed walkthough, visit our Getting Started Guide.

library(modeltime.gluonts)

library(tidymodels)

library(tidyverse)

# Fit a GluonTS DeepAR Model

model_fit_deepar <- deep_ar(

id = "id",

freq = "M",

prediction_length = 24,

lookback_length = 48,

epochs = 5

) %>%

set_engine("gluonts_deepar") %>%

fit(value ~ ., training(m750_splits))

# Forecast with 95% Confidence Interval

modeltime_table(

model_fit_deepar

) %>%

modeltime_calibrate(new_data = testing(m750_splits)) %>%

modeltime_forecast(

new_data = testing(m750_splits),

actual_data = m750,

conf_interval = 0.95

) %>%

plot_modeltime_forecast(.interactive = FALSE)

Meet the modeltime ecosystem

Learn a growing ecosystem of forecasting packages

The modeltime ecosystem is growing

Modeltime is part of a growing ecosystem of Modeltime forecasting packages.

Take the High-Performance Forecasting Course

Become the forecasting expert for your organization

High-Performance Time Series Course

Time Series is Changing

Time series is changing. Businesses now need 10,000+ time series forecasts every day. This is what I call a High-Performance Time Series Forecasting System (HPTSF) - Accurate, Robust, and Scalable Forecasting.

High-Performance Forecasting Systems will save companies by improving accuracy and scalability. Imagine what will happen to your career if you can provide your organization a “High-Performance Time Series Forecasting System” (HPTSF System).

How to Learn High-Performance Time Series Forecasting

I teach how to build a HPTFS System in my High-Performance Time Series Forecasting Course. You will learn:

-

Time Series Machine Learning (cutting-edge) with

Modeltime- 30+ Models (Prophet, ARIMA, XGBoost, Random Forest, & many more) -

Deep Learning with

GluonTS(Competition Winners) - Time Series Preprocessing, Noise Reduction, & Anomaly Detection

- Feature engineering using lagged variables & external regressors

- Hyperparameter Tuning

- Time series cross-validation

- Ensembling Multiple Machine Learning & Univariate Modeling Techniques (Competition Winner)

- Scalable Forecasting - Forecast 1000+ time series in parallel

- and more.

Become the Time Series Expert for your organization.