Making an DeepAR Model

Let’s get started by making a DeepAR Model. In a matter of minutes, you’ll generate the 7 forecasts shown below. If you’d like to improve your time series forecasting abilities, then please take my High-Performance Time Series Course.

Installation

Next, set up the Python Environment with

install_gluonts(). You only need to run this one time, and

then you are good to go.

We have a more detailed installation instructions and troubleshooting guidance in our Installation Guide.

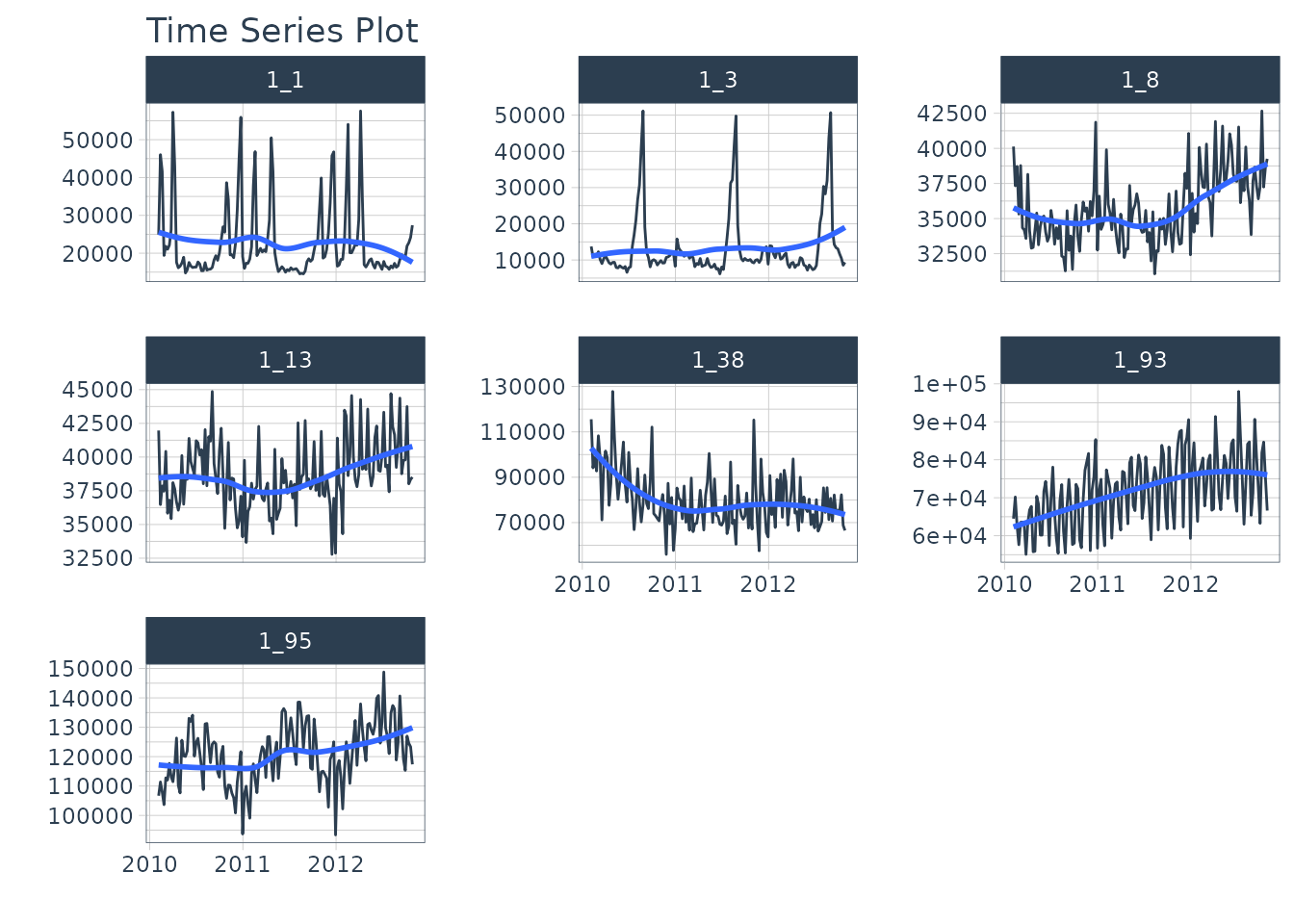

Time Series Data

We’ll use the walmart_sales_weekly dataset, which

contains 7 weekly time series of sales data for various departments in a

Walmart Store.

data <- walmart_sales_weekly %>%

select(id, Date, Weekly_Sales) %>%

set_names(c("id", "date", "value"))

data %>%

group_by(id) %>%

plot_time_series(

date,

value,

.facet_ncol = 3,

.interactive = FALSE

)

We’ll create the forecast region using future_frame().

We are forecasting 1 week (24x7 timestamps) into the future.

HORIZON <- 52

new_data <- data %>%

group_by(id) %>%

future_frame(.length_out = HORIZON) %>%

ungroup()

new_data

#> # A tibble: 364 × 2

#> id date

#> <fct> <date>

#> 1 1_1 2012-11-02

#> 2 1_1 2012-11-09

#> 3 1_1 2012-11-16

#> 4 1_1 2012-11-23

#> 5 1_1 2012-11-30

#> 6 1_1 2012-12-07

#> 7 1_1 2012-12-14

#> 8 1_1 2012-12-21

#> 9 1_1 2012-12-28

#> 10 1_1 2013-01-04

#> # ℹ 354 more rowsMaking a DeepAR Model

We’ll create a DeepAR model using the deep_ar()

function.

- This is a univariate modeling algorithm that uses Deep Learning and Autoregression.

- We select the GluonTS version by setting the engine to

gluonts_deepar.

Forecasting

With a model in hand, we can simply follow the Modeltime Workflow to generate a forecast for the multiple time series groups.

modeltime_forecast_tbl <- modeltime_table(

model_fit_deepar

) %>%

modeltime_forecast(

new_data = new_data,

actual_data = data,

keep_data = TRUE

) %>%

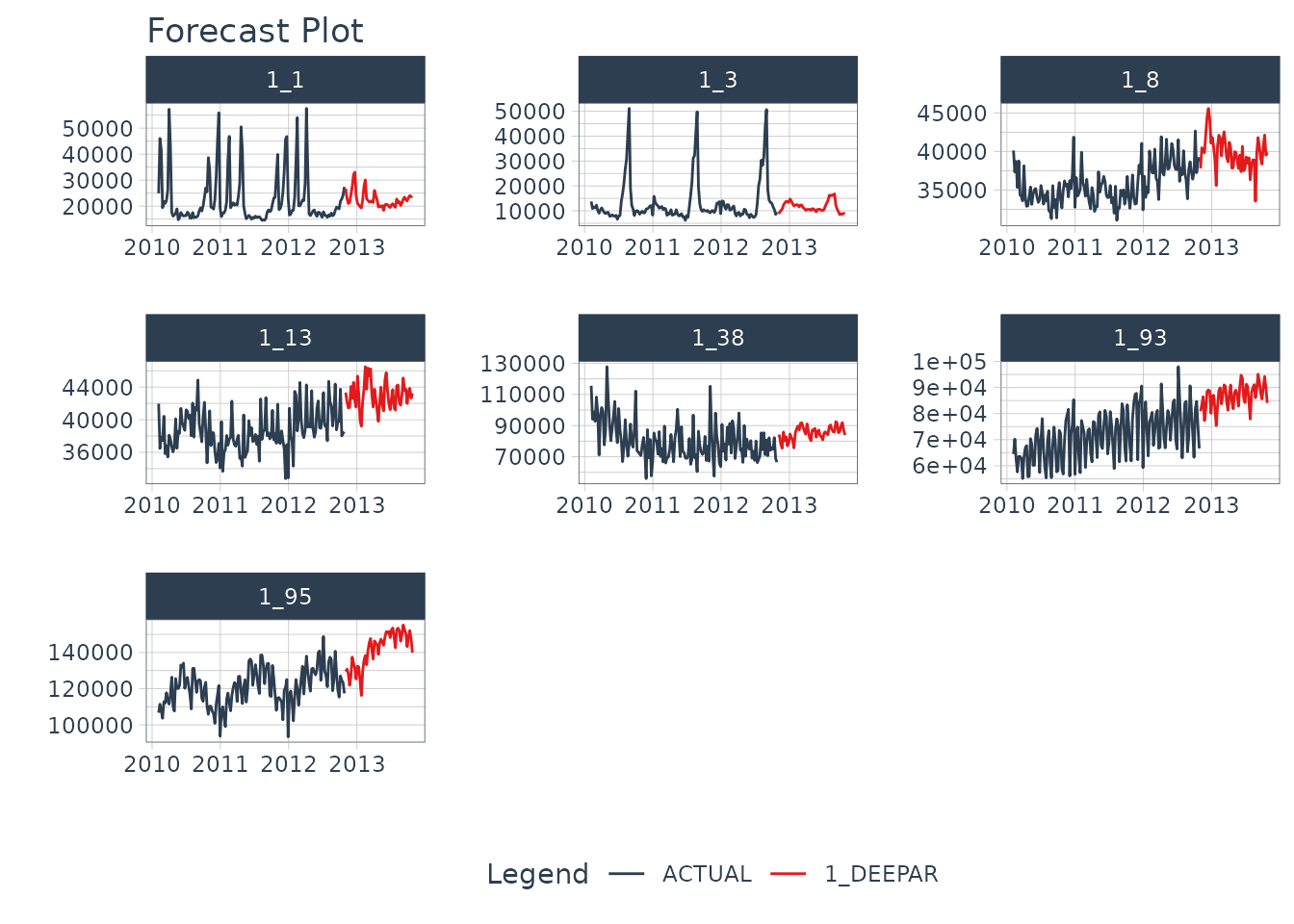

group_by(id) We can visualize the forecast with

plot_modeltime_forecast().

modeltime_forecast_tbl %>%

plot_modeltime_forecast(

.conf_interval_show = FALSE,

.facet_ncol = 3,

.facet_scales = "free",

.interactive = FALSE

)

Saving and Loading Models

GluonTS models will need to “serialized” (a fancy word for saved to a

directory that contains the recipe for recreating the models). To save

the models, use save_gluonts_model().

- Provide a directory where you want to save the model.

- This saves all of the model files in the directory.

model_fit_deepar %>%

save_gluonts_model(path = "deepar_model", overwrite = TRUE)You can reload the model into R using

load_gluonts_model().

model_fit_deepar <- load_gluonts_model("deepar_model")Take the High-Performance Forecasting Course

Become the forecasting expert for your organization

High-Performance Time Series Course

Time Series is Changing

Time series is changing. Businesses now need 10,000+ time series forecasts every day. This is what I call a High-Performance Time Series Forecasting System (HPTSF) - Accurate, Robust, and Scalable Forecasting.

High-Performance Forecasting Systems will save companies by improving accuracy and scalability. Imagine what will happen to your career if you can provide your organization a “High-Performance Time Series Forecasting System” (HPTSF System).

How to Learn High-Performance Time Series Forecasting

I teach how to build a HPTFS System in my High-Performance Time Series Forecasting Course. You will learn:

-

Time Series Machine Learning (cutting-edge) with

Modeltime- 30+ Models (Prophet, ARIMA, XGBoost, Random Forest, & many more) -

Deep Learning with

GluonTS(Competition Winners) - Time Series Preprocessing, Noise Reduction, & Anomaly Detection

- Feature engineering using lagged variables & external regressors

- Hyperparameter Tuning

- Time series cross-validation

- Ensembling Multiple Machine Learning & Univariate Modeling Techniques (Competition Winner)

- Scalable Forecasting - Forecast 1000+ time series in parallel

- and more.

Become the Time Series Expert for your organization.