Anomalize Methods

Business Science

2023-12-28

Source:vignettes/anomalize_methods.Rmd

anomalize_methods.RmdAnomaly detection is critical to many disciplines, but possibly none

more important than in time series analysis. A time

series is the sequential set of values tracked over a time duration. The

definition we use for an anomaly is simple: an anomaly

is something that happens that (1) was unexpected or (2) was caused by

an abnormal event. Therefore, the problem we intend to solve with

anomalize is providing methods to accurately detect these

“anomalous” events.

The methods that anomalize uses can be separated into

two main tasks:

- Generating Time Series Analysis Remainders

- Detecting Anomalies in the Remainders

1. Generating Time Series Analysis Remainders

Anomaly detection is performed on remainders from a time series analysis that have had removed both:

- Seasonal Components: Cyclic pattern usually occurring on a daily cycle for minute or hour data or a weekly cycle for daily data

- Trend Components: Longer term growth that happens over many observations.

Therefore, the first objective is to generate remainders from a time series. Some analysis techniques are better for this task then others, and it’s probably not the ones you would think.

There are many ways that a time series can be deconstructed to produce residuals. We have tried many including using ARIMA, Machine Learning (Regression), Seasonal Decomposition, and so on. For anomaly detection, we have seen the best performance using seasonal decomposition. Most high performance machine learning techniques perform poorly for anomaly detection because of overfitting, which downplays the difference between the actual value and the fitted value. This is not the objective of anomaly detection wherein we need to highlight the anomaly. Seasonal decomposition does very well for this task, removing the right features (i.e. seasonal and trend components) while preserving the characteristics of anomalies in the residuals.

The anomalize package implements two techniques for

seasonal decomposition:

- STL: Seasonal Decomposition of Time Series by Loess

- Twitter: Seasonal Decomposition of Time Series by Median

Each method has pros and cons.

1.A. STL

The STL method uses the stl() function from the

stats package. STL works very well in circumstances where a

long term trend is present. The Loess algorithm typically does a very

good job at detecting the trend. However, it circumstances when the

seasonal component is more dominant than the trend, Twitter tends to

perform better.

1.B. Twitter

The Twitter method is a similar decomposition method to that used in

Twitter’s AnomalyDetection package. The Twitter method

works identically to STL for removing the seasonal component. The main

difference is in removing the trend, which is performed by removing the

median of the data rather than fitting a smoother. The median works well

when a long-term trend is less dominant that the short-term seasonal

component. This is because the smoother tends to overfit the

anomalies.

1.C. Comparison of STL and Twitter Decomposition Methods

Load two libraries to perform the comparison.

library(tidyverse)

library(anomalize)

# NOTE: timetk now has anomaly detection built in, which

# will get the new functionality going forward.

anomalize <- anomalize::anomalize

plot_anomalies <- anomalize::plot_anomaliesCollect data on the daily downloads of the lubridate

package. This comes from the data set,

tidyverse_cran_downloads that is part of

anomalize package.

# Data on `lubridate` package daily downloads

lubridate_download_history <- tidyverse_cran_downloads %>%

filter(package == "lubridate") %>%

ungroup()

# Output first 10 observations

lubridate_download_history %>%

head(10) %>%

knitr::kable()| date | count | package |

|---|---|---|

| 2017-01-01 | 643 | lubridate |

| 2017-01-02 | 1350 | lubridate |

| 2017-01-03 | 2940 | lubridate |

| 2017-01-04 | 4269 | lubridate |

| 2017-01-05 | 3724 | lubridate |

| 2017-01-06 | 2326 | lubridate |

| 2017-01-07 | 1107 | lubridate |

| 2017-01-08 | 1058 | lubridate |

| 2017-01-09 | 2494 | lubridate |

| 2017-01-10 | 3237 | lubridate |

We can visualize the differences between the two decomposition methods.

# STL Decomposition Method

p1 <- lubridate_download_history %>%

time_decompose(count,

method = "stl",

frequency = "1 week",

trend = "3 months") %>%

anomalize(remainder) %>%

plot_anomaly_decomposition() +

ggtitle("STL Decomposition")

#> Converting from tbl_df to tbl_time.

#> Auto-index message: index = date

#> frequency = 7 days

#> trend = 91 days

#> Registered S3 method overwritten by 'quantmod':

#> method from

#> as.zoo.data.frame zoo

# Twitter Decomposition Method

p2 <- lubridate_download_history %>%

time_decompose(count,

method = "twitter",

frequency = "1 week",

trend = "3 months") %>%

anomalize(remainder) %>%

plot_anomaly_decomposition() +

ggtitle("Twitter Decomposition")

#> Converting from tbl_df to tbl_time.

#> Auto-index message: index = date

#> frequency = 7 days

#> median_span = 85 days

# Show plots

p1

p2

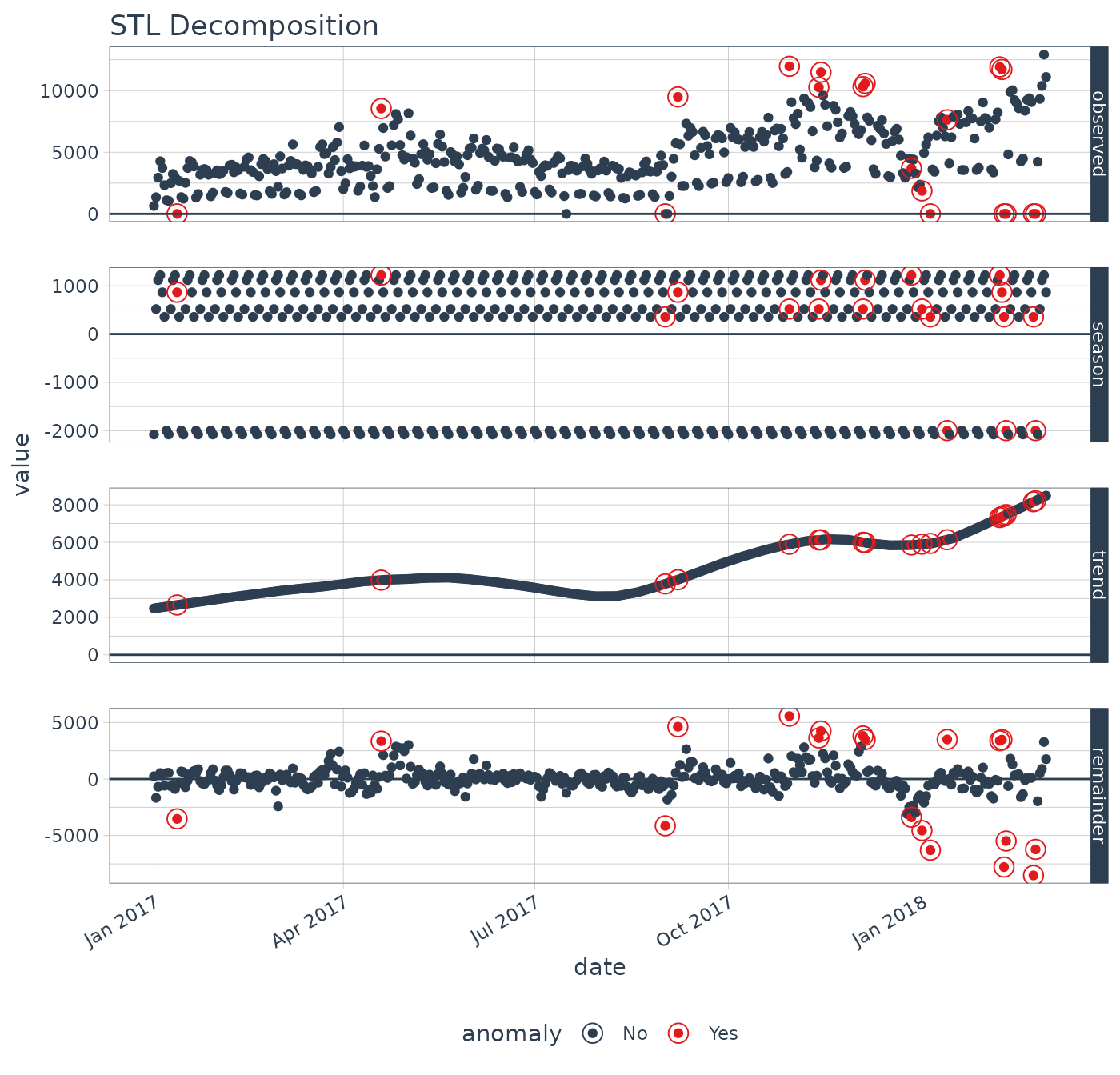

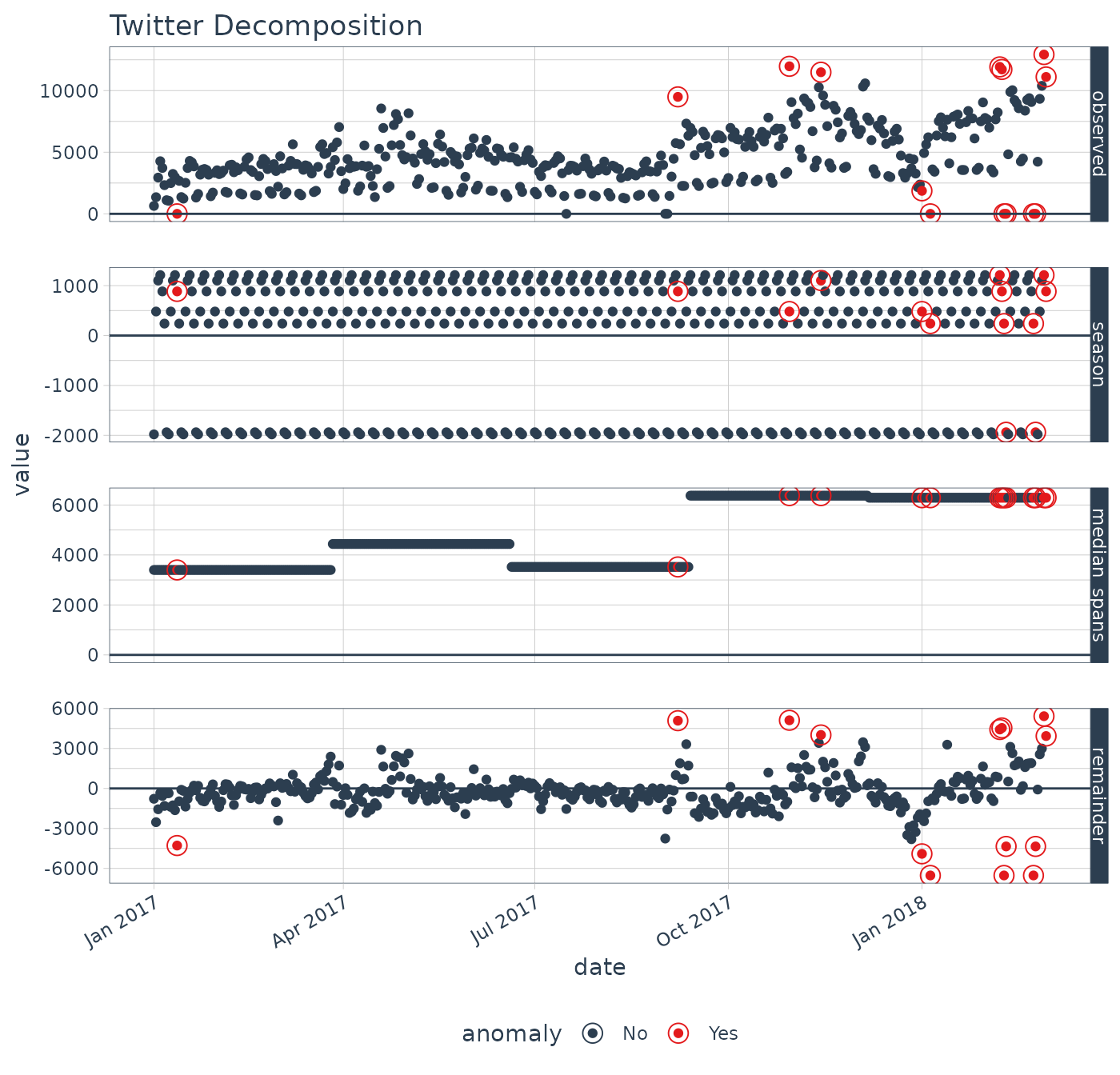

We can see that the season components for both STL and Twitter decomposition are exactly the same. The difference is the trend component:

STL: The STL trend follows a smoothed Loess with a Loess trend window at 91 days (as defined by

trend = "3 months"). The remainder of the decomposition is centered.Twitter: The Twitter trend is a series of medians that are removed. The median span logic is such that the medians are selected to have equal distribution of observations. Because of this, the trend span is 85 days, which is slightly less than the 91 days (or 3 months).

1.D. Transformations

In certain circumstances such as multiplicative trends in which the

residuals (remainders) have heteroskedastic properties, which is when

the variance changes as the time series sequence progresses (e.g. the

remainders fan out), it becomes difficult to detect anomalies in

especially in the low variance regions. Logarithmic or power

transformations can help in these situations. This is beyond the scope

of the methods and is not implemented in the current version of

anomalize. However, these transformations can be performed

on the incoming target and the output can be inverse-transformed.

2. Detecting Anomalies in the Remainders

Once a time series analysis is completed and the remainder has the

desired characteristics, the remainders can be analyzed. The challenge

is that anomalies are high leverage points that distort the

distribution. The anomalize package implements two methods

that are resistant to the high leverage points:

- IQR: Inner Quartile Range

- GESD: Generalized Extreme Studentized Deviate Test

Both methods have pros and cons.

2.A. IQR

The IQR method is a similar method to that used in the

forecast package for anomaly removal within the

tsoutliers() function. It takes a distribution and uses the

25% and 75% inner quartile range to establish the distribution of the

remainder. Limits are set by default to a factor of 3X above and below

the inner quartile range, and any remainders beyond the limits are

considered anomalies.

The alpha parameter adjusts the 3X factor. By default,

alpha = 0.05 for consistency with the GESD method. An

alpha = 0.025, results in a 6X factor, expanding the limits

and making it more difficult for data to be an anomaly. Conversely, an

alpha = 0.10 contracts the limits to a factor of 1.5X

making it more easy for data to be an anomaly.

The IQR method does not depend on any loops and is therefore faster and more easily scaled than the GESD method. However, it may not be as accurate in detecting anomalies since the high leverage anomalies can skew the centerline (median) of the IQR.

2.B. GESD

The GESD method is used in Twitter’s AnomalyDetection

package. It involves an iterative evaluation of the Generalized Extreme

Studentized Deviate test, which progressively evaluates anomalies,

removing the worst offenders and recalculating the test statistic and

critical value. The critical values progressively contract as more high

leverage points are removed.

The alpha parameter adjusts the width of the critical

values. By default, alpha = 0.05.

The GESD method is iterative, and therefore more expensive that the IQR method. The main benefit is that GESD is less resistant to high leverage points since the distribution of the data is progressively analyzed as anomalies are removed.

2.C Comparison of IQR and GESD Methods

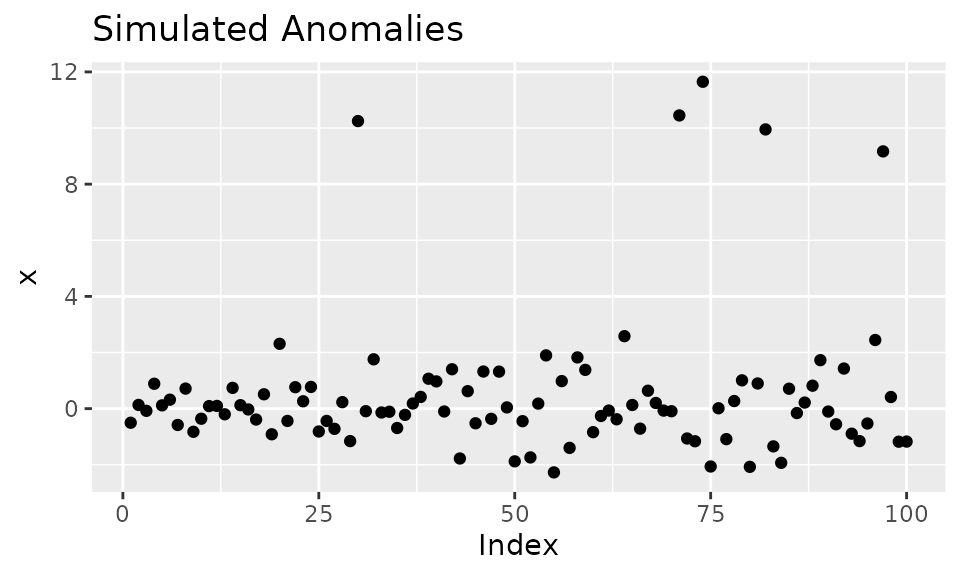

We can generate anomalous data to illustrate how each method work compares to each other.

# Generate anomalies

set.seed(100)

x <- rnorm(100)

idx_outliers <- sample(100, size = 5)

x[idx_outliers] <- x[idx_outliers] + 10

# Visualize simulated anomalies

qplot(1:length(x), x,

main = "Simulated Anomalies",

xlab = "Index")

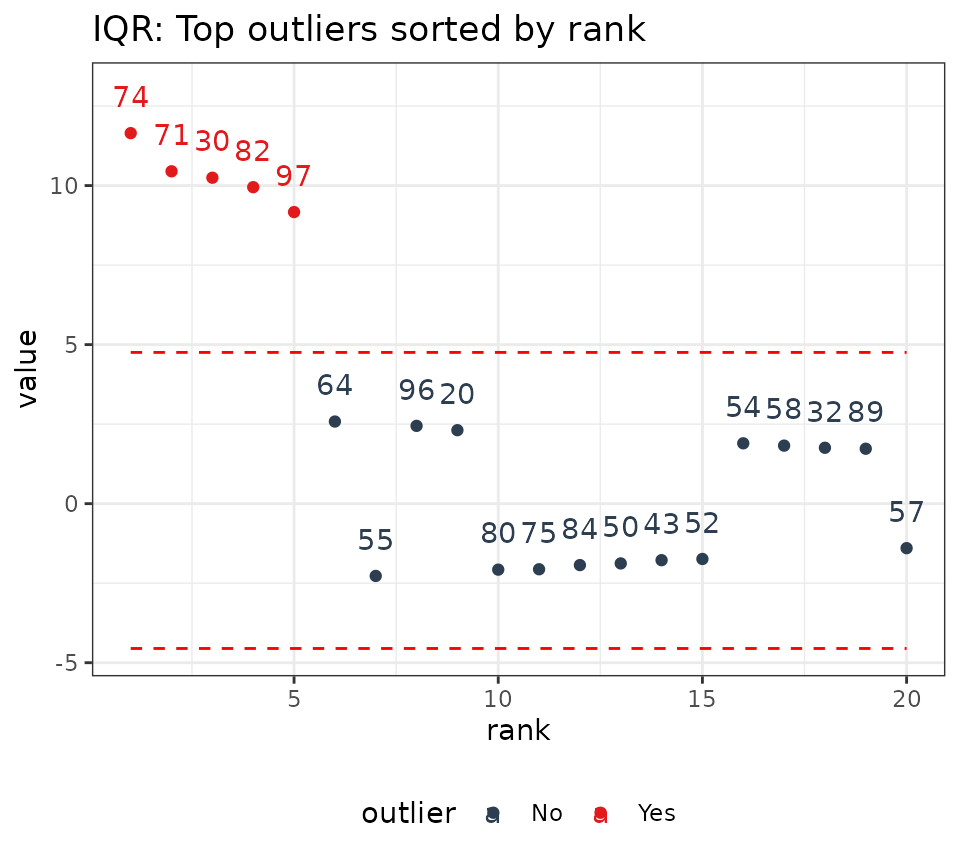

Two functions power anomalize(), which are

iqr() and gesd(). We can use these

intermediate functions to illustrate the anomaly detection

characteristics.

# Analyze outliers: Outlier Report is available with verbose = TRUE

iqr_outliers <- iqr(x, alpha = 0.05, max_anoms = 0.2, verbose = TRUE)$outlier_report

gesd_outliers <- gesd(x, alpha = 0.05, max_anoms = 0.2, verbose = TRUE)$outlier_report

# ploting function for anomaly plots

ggsetup <- function(data) {

data %>%

ggplot(aes(rank, value, color = outlier)) +

geom_point() +

geom_line(aes(y = limit_upper), color = "red", linetype = 2) +

geom_line(aes(y = limit_lower), color = "red", linetype = 2) +

geom_text(aes(label = index), vjust = -1.25) +

theme_bw() +

scale_color_manual(values = c("No" = "#2c3e50", "Yes" = "#e31a1c")) +

expand_limits(y = 13) +

theme(legend.position = "bottom")

}

# Visualize

p3 <- iqr_outliers %>%

ggsetup() +

ggtitle("IQR: Top outliers sorted by rank")

p4 <- gesd_outliers %>%

ggsetup() +

ggtitle("GESD: Top outliers sorted by rank")

# Show plots

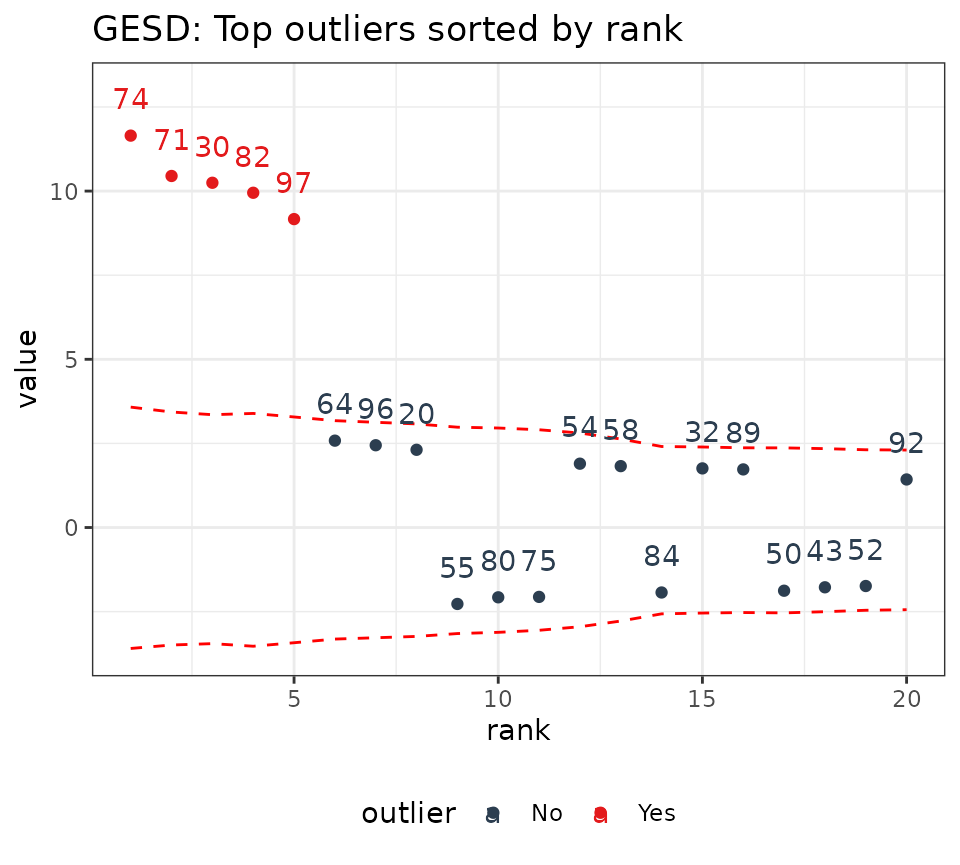

p3

p4

We can see that the IQR limits don’t vary whereas the GESD limits get more stringent as anomalies are removed from the data. As a result, the GESD method tends to be more accurate in detecting anomalies at the expense of incurring more processing time for the looped anomaly removal. This expense is most noticeable with larger data sets (many observations or many time series).

3. Conclusion

The anomalize package implements several useful and

accurate techniques for implementing anomaly detection. The user should

now have a better understanding of how the algorithms work along with

the strengths and weaknesses of each method.

4. References

Alex T.C. Lau (November/December 2015). GESD - A Robust and Effective Technique for Dealing with Multiple Outliers. ASTM Standardization News. www.astm.org/sn

Interested in Learning Anomaly Detection?

Business Science offers two 1-hour courses on Anomaly Detection:

Learning Lab 18 - Time Series Anomaly Detection with

anomalizeLearning Lab 17 - Anomaly Detection with

H2OMachine Learning