Forecasting Using Multiple Models

Matt Dancho

2026-03-17

Source:vignettes/SW02_Forecasting_Multiple_Models.Rmd

SW02_Forecasting_Multiple_Models.RmdExtending

broomto time series forecasting

One of the most powerful benefits of sweep is that it

helps forecasting at scale within the “tidyverse”. There are two common

situations:

- Applying a model to groups of time series

- Applying multiple models to a time series

In this vignette we’ll review how sweep can help the

second situation: Applying multiple models to a

time series.

Forecasting Bike Sales Revenue

To start, we’ll build a monthly revenue series from the

bike_sales data set that ships with sweep. To

keep the missing-value cleanup step in the example, we’ll intentionally

blank a few monthly observations.

sales_monthly_raw <- bike_sales %>%

dplyr::mutate(date = lubridate::floor_date(order.date, unit = "month")) %>%

dplyr::group_by(date) %>%

dplyr::summarise(price = sum(price.ext), .groups = "drop") %>%

dplyr::mutate(price = dplyr::if_else(dplyr::row_number() %in% c(7L, 19L, 38L), NA_real_, price))

sales_monthly_raw## # A tibble: 60 × 2

## date price

## <date> <dbl>

## 1 2011-01-01 1165365

## 2 2011-02-01 5794945

## 3 2011-03-01 6811655

## 4 2011-04-01 14097770

## 5 2011-05-01 8488650

## 6 2011-06-01 14725405

## 7 2011-07-01 NA

## 8 2011-08-01 4456670

## 9 2011-09-01 3505000

## 10 2011-10-01 1548640

## # ℹ 50 more rowsUpon a brief inspection, the data contains 3 NA values

that will need to be dealt with.

summary(sales_monthly_raw$price)## Min. 1st Qu. Median Mean 3rd Qu. Max. NA's

## 1165365 4204590 6394690 7928688 10331390 25227175 3We can use the fill() from the tidyr

package to help deal with these data. We first fill down and then fill

up to use the previous and then post days prices to fill in the missing

data.

sales_monthly <- sales_monthly_raw %>%

fill(price, .direction = "down") %>%

fill(price, .direction = "up")We can now visualize the data.

sales_monthly %>%

ggplot(aes(x = date, y = price)) +

geom_line(color = palette_light()[[1]]) +

labs(title = "Bike Sales Revenue, Monthly", x = "", y = "Revenue") +

scale_y_continuous(labels = scales::label_dollar(scale = 1 / 1000000, suffix = "M")) +

theme_tq()

Monthly periodicity might be a bit granular for model fitting. We can

easily switch periodicity to quarterly using tq_transmute()

from the tidyquant package along with the periodicity

aggregation function to.period from the xts

package. We’ll convert the date to yearqtr class which is

regularized.

sales_quarterly <- sales_monthly %>%

tq_transmute(mutate_fun = to.period, period = "quarters")

sales_quarterly## # A tibble: 20 × 2

## date price

## <date> <dbl>

## 1 2011-03-01 6811655

## 2 2011-06-01 14725405

## 3 2011-09-01 3505000

## 4 2011-12-01 4081460

## 5 2012-03-01 25227175

## 6 2012-06-01 6394690

## 7 2012-09-01 9678210

## 8 2012-12-01 2711705

## 9 2013-03-01 15584435

## 10 2013-06-01 15182715

## 11 2013-09-01 5358180

## 12 2013-12-01 3953565

## 13 2014-03-01 3678090

## 14 2014-06-01 6596090

## 15 2014-09-01 10907310

## 16 2014-12-01 7190935

## 17 2015-03-01 19645635

## 18 2015-06-01 11146845

## 19 2015-09-01 6377295

## 20 2015-12-01 7740870Another quick visualization to show the reduction in granularity.

sales_quarterly %>%

ggplot(aes(x = date, y = price)) +

geom_line(color = palette_light()[[1]], linewidth = 1) +

labs(title = "Bike Sales Revenue, Quarterly", x = "", y = "Revenue") +

scale_y_continuous(labels = scales::label_dollar(scale = 1 / 1000000, suffix = "M")) +

scale_x_date(date_breaks = "5 years", date_labels = "%Y") +

theme_tq()

Performing Forecasts Using Multiple Models

In this section we will use three models to forecast bike sales revenue:

- ARIMA

- ETS

- BATS

Multiple Models Concept

Before we jump into modeling, let’s take a look at the multiple model process from R for Data Science, Chapter 25 Many Models. We first create a data frame from a named list. The example below has two columns: “f” the functions as text, and “params” a nested list of parameters we will pass to the respective function in column “f”.

df <- tibble(

f = c("runif", "rpois", "rnorm"),

params = list(

list(n = 10),

list(n = 5, lambda = 10),

list(n = 10, mean = -3, sd = 10)

)

)

df## # A tibble: 3 × 2

## f params

## <chr> <list>

## 1 runif <named list [1]>

## 2 rpois <named list [2]>

## 3 rnorm <named list [3]>We can also view the contents of the df$params column to

understand the underlying structure. Notice that there are three primary

levels and then secondary levels containing the name-value pairs of

parameters. This format is important.

df$params## [[1]]

## [[1]]$n

## [1] 10

##

##

## [[2]]

## [[2]]$n

## [1] 5

##

## [[2]]$lambda

## [1] 10

##

##

## [[3]]

## [[3]]$n

## [1] 10

##

## [[3]]$mean

## [1] -3

##

## [[3]]$sd

## [1] 10Next we apply the functions to the parameters using a special

function, invoke_map(). The parameter lists in the “params”

column are passed to the function in the “f” column. The output is in a

nested list-column named “out”.

# FIXME invoke_map is deprecated

df_out <- df %>%

mutate(out = invoke_map(f, params))## Warning: There were 2 warnings in `mutate()`.

## The first warning was:

## ℹ In argument: `out = invoke_map(f, params)`.

## Caused by warning:

## ! `invoke_map()` was deprecated in purrr 1.0.0.

## ℹ Please use map() + exec() instead.

## ℹ Run `dplyr::last_dplyr_warnings()` to see the 1 remaining warning.

df_out## # A tibble: 3 × 3

## f params out

## <chr> <list> <list>

## 1 runif <named list [1]> <dbl [10]>

## 2 rpois <named list [2]> <int [5]>

## 3 rnorm <named list [3]> <dbl [10]>And, here’s the contents of “out”, which is the result of mapping a list of functions to a list of parameters. Pretty powerful!

df_out$out## [[1]]

## [1] 0.080750138 0.834333037 0.600760886 0.157208442 0.007399441 0.466393497

## [7] 0.497777389 0.289767245 0.732881987 0.772521511

##

## [[2]]

## [1] 13 4 7 9 8

##

## [[3]]

## [1] 3.289820 17.650249 -19.309894 2.124269 -21.630115 -8.220125

## [7] -3.526019 2.429963 -12.140748 1.681544Take a minute to understand the conceptual process of the

invoke_map function and specifically the parameter setup.

Once you are comfortable, we can move on to model implementation.

Multiple Model Implementation

We’ll need to take the following steps to in an actual forecast model implementation:

- Coerce the data to time series

- Build a model list using nested lists

- Create the the model data frame

- Invoke a function map

This is easier than it sounds. Let’s start by coercing the univariate

time series with tk_ts().

sales_quarterly_ts <- sales_quarterly %>%

tk_ts(select = -date, start = c(2011, 1), freq = 4)

sales_quarterly_ts## Qtr1 Qtr2 Qtr3 Qtr4

## 2011 6811655 14725405 3505000 4081460

## 2012 25227175 6394690 9678210 2711705

## 2013 15584435 15182715 5358180 3953565

## 2014 3678090 6596090 10907310 7190935

## 2015 19645635 11146845 6377295 7740870Next, create a nested list using the function names as the first-level keys (this is important as you’ll see in the next step). Pass the model parameters as name-value pairs in the second level.

models_list <- list(

auto.arima = list(

y = sales_quarterly_ts

),

ets = list(

y = sales_quarterly_ts,

damped = TRUE

),

bats = list(

y = sales_quarterly_ts

)

)Now, convert to a data frame using the function,

enframe() that turns lists into tibbles. Set the arguments

name = "f" and value = "params". In doing so

we get a bonus: the model names are the now conveniently located in

column “f”.

models_tbl <- tibble::enframe(models_list, name = "f", value = "params")

models_tbl## # A tibble: 3 × 2

## f params

## <chr> <list>

## 1 auto.arima <named list [1]>

## 2 ets <named list [2]>

## 3 bats <named list [1]>We are ready to invoke the map. Combine mutate() with

invoke_map() as follows. Bada bing, bada boom, we now have

models fitted using the parameters we defined previously.

models_tbl_fit <- models_tbl %>%

mutate(fit = purrr::invoke_map(f, params))

models_tbl_fit## # A tibble: 3 × 3

## f params fit

## <chr> <list> <list>

## 1 auto.arima <named list [1]> <fc_model>

## 2 ets <named list [2]> <fc_model>

## 3 bats <named list [1]> <fc_model>Inspecting the Model Fit

It’s a good point to review and understand the model output. We can

review the model parameters, accuracy measurements, and the residuals

using sw_tidy(), sw_glance(), and

sw_augment().

sw_tidy

The tidying function returns the model parameters and estimates. We

use the combination of mutate and map to

iteratively apply the sw_tidy() function as a new column

named “tidy”. Then we unnest and spread to review the terms by model

function.

models_tbl_fit %>%

mutate(tidy = map(fit, sw_tidy)) %>%

unnest(tidy) %>%

spread(key = f, value = estimate)## # A tibble: 13 × 6

## params fit term auto.arima bats ets

## <list> <list> <chr> <dbl> <dbl> <dbl>

## 1 <named list [1]> <fc_model> intercept 9324863. NA NA

## 2 <named list [1]> <fc_model> alpha NA -0.01000 NA

## 3 <named list [1]> <fc_model> ar.coefficients NA NA NA

## 4 <named list [1]> <fc_model> beta NA NA NA

## 5 <named list [1]> <fc_model> damping.parameter NA NA NA

## 6 <named list [1]> <fc_model> gamma.values NA NA NA

## 7 <named list [1]> <fc_model> lambda NA 0.00000521 NA

## 8 <named list [1]> <fc_model> ma.coefficients NA NA NA

## 9 <named list [2]> <fc_model> alpha NA NA 1.00e-4

## 10 <named list [2]> <fc_model> b NA NA 4.57e+5

## 11 <named list [2]> <fc_model> beta NA NA 1.00e-4

## 12 <named list [2]> <fc_model> l NA NA 8.67e+6

## 13 <named list [2]> <fc_model> phi NA NA 8.00e-1sw_glance

Glance is one of the most powerful tools because it yields the model accuracies enabling direct comparisons between the fit of each model. We use the same process for used for tidy, except theres no need to spread to perform the comparison. We can see that the ARIMA model has the lowest AIC by far.

## Warning: The `.drop` argument of `unnest()` is deprecated as of tidyr 1.0.0.

## ℹ All list-columns are now preserved.

## Call `lifecycle::last_lifecycle_warnings()` to see where this warning was

## generated.## # A tibble: 3 × 15

## f params fit model.desc sigma logLik AIC BIC ME

## <chr> <list> <list> <chr> <dbl> <dbl> <dbl> <dbl> <dbl>

## 1 auto.ar… <named list> <fc_model> ARIMA(0,0… 6.02e+6 -340. 684. 686. 0

## 2 ets <named list> <fc_model> ETS(A,Ad,… 6.86e+6 -342. 696. 702. -8.06e5

## 3 bats <named list> <fc_model> BATS(0, {… 6.02e-1 674. 680. 682. 1.64e6

## # ℹ 6 more variables: RMSE <dbl>, MAE <dbl>, MPE <dbl>, MAPE <dbl>, MASE <dbl>,

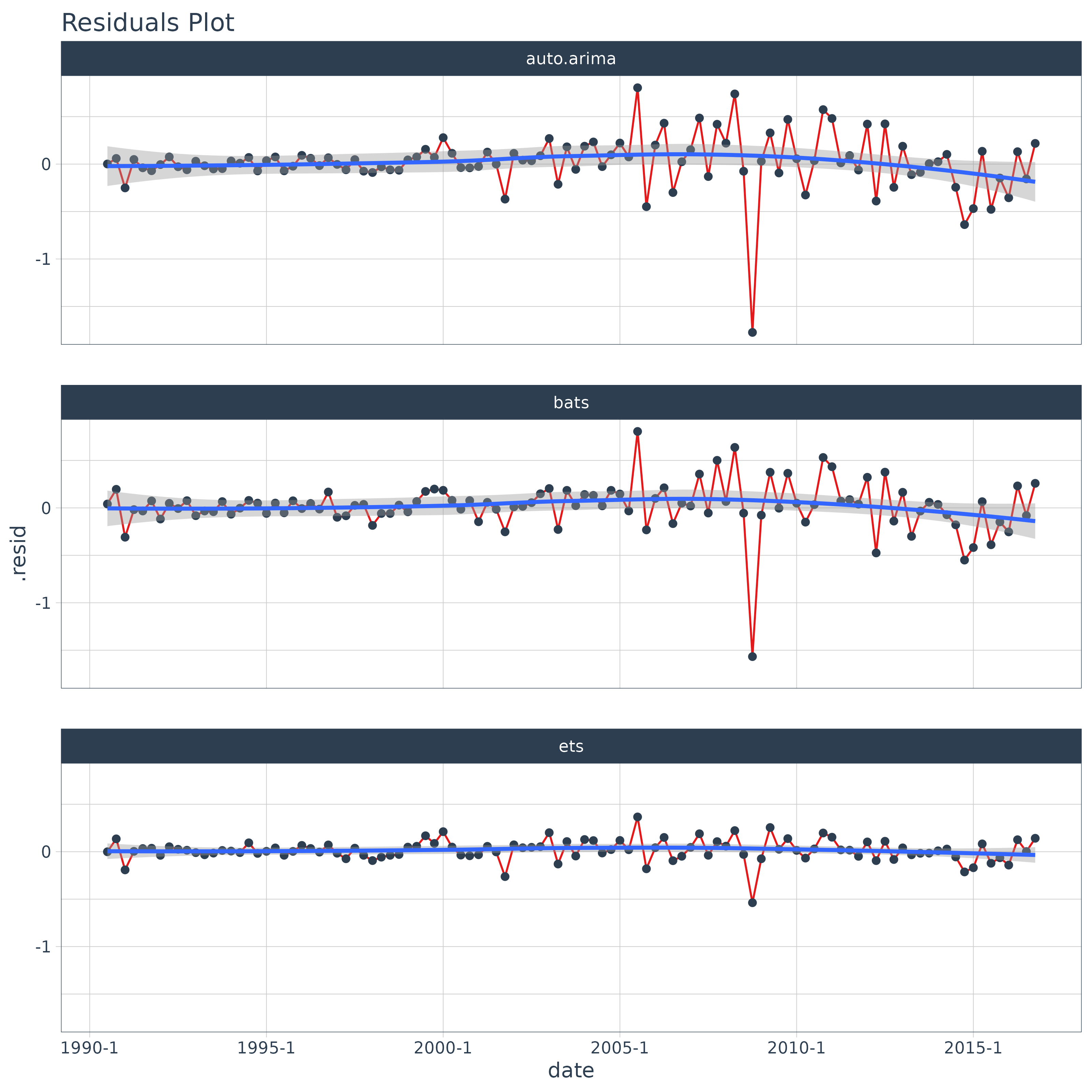

## # ACF1 <dbl>sw_augment

We can augment the models to get the residuals following the same

procedure. We can pipe (%>%) the results right into

ggplot() for plotting. Notice the ARIMA model has the

largest residuals especially as the model index increases whereas the

bats model has relatively low residuals.

models_tbl_fit %>%

mutate(augment = map(fit, sw_augment, rename_index = "date")) %>%

unnest(augment) %>%

ggplot(aes(x = date, y = .resid, group = f)) +

geom_line(color = palette_light()[[2]]) +

geom_point(color = palette_light()[[1]]) +

geom_smooth(method = "loess") +

facet_wrap(~ f, nrow = 3) +

labs(title = "Residuals Plot") +

theme_tq()## `geom_smooth()` using formula = 'y ~ x'

Forecasting the model

Creating the forecast for the models is accomplished by mapping the

forecast function. The next six quarters are forecasted

withe the argument h = 6.

## # A tibble: 3 × 4

## f params fit fcast

## <chr> <list> <list> <list>

## 1 auto.arima <named list [1]> <fc_model> <forecast>

## 2 ets <named list [2]> <fc_model> <forecast>

## 3 bats <named list [1]> <fc_model> <forecast>Tidying the forecast

Next, we map sw_sweep, which coerces the forecast into

the “tidy” tibble format. We set fitted = FALSE to remove

the model fitted values from the output. We set

timetk_idx = TRUE to use dates instead of numeric values

for the index.

models_tbl_fcast_tidy <- models_tbl_fcast %>%

mutate(sweep = map(fcast, sw_sweep, fitted = FALSE, timetk_idx = TRUE, rename_index = "date"))## Warning: There were 3 warnings in `mutate()`.

## The first warning was:

## ℹ In argument: `sweep = map(fcast, sw_sweep, fitted = FALSE, timetk_idx = TRUE,

## rename_index = "date")`.

## Caused by warning in `.check_tzones()`:

## ! 'tzone' attributes are inconsistent

## ℹ Run `dplyr::last_dplyr_warnings()` to see the 2 remaining warnings.

models_tbl_fcast_tidy## # A tibble: 3 × 5

## f params fit fcast sweep

## <chr> <list> <list> <list> <list>

## 1 auto.arima <named list [1]> <fc_model> <forecast> <tibble [26 × 7]>

## 2 ets <named list [2]> <fc_model> <forecast> <tibble [26 × 7]>

## 3 bats <named list [1]> <fc_model> <forecast> <tibble [26 × 7]>We can unnest the “sweep” column to get the results of all three models.

## # A tibble: 78 × 11

## f params fit fcast date key price lo.80 lo.95

## <chr> <list> <list> <list> <date> <chr> <dbl> <dbl> <dbl>

## 1 auto.… <named list> <fc_model> <forecast> 2011-03-01 actu… 6.81e6 NA NA

## 2 auto.… <named list> <fc_model> <forecast> 2011-06-01 actu… 1.47e7 NA NA

## 3 auto.… <named list> <fc_model> <forecast> 2011-09-01 actu… 3.51e6 NA NA

## 4 auto.… <named list> <fc_model> <forecast> 2011-12-01 actu… 4.08e6 NA NA

## 5 auto.… <named list> <fc_model> <forecast> 2012-03-01 actu… 2.52e7 NA NA

## 6 auto.… <named list> <fc_model> <forecast> 2012-06-01 actu… 6.39e6 NA NA

## 7 auto.… <named list> <fc_model> <forecast> 2012-09-01 actu… 9.68e6 NA NA

## 8 auto.… <named list> <fc_model> <forecast> 2012-12-01 actu… 2.71e6 NA NA

## 9 auto.… <named list> <fc_model> <forecast> 2013-03-01 actu… 1.56e7 NA NA

## 10 auto.… <named list> <fc_model> <forecast> 2013-06-01 actu… 1.52e7 NA NA

## # ℹ 68 more rows

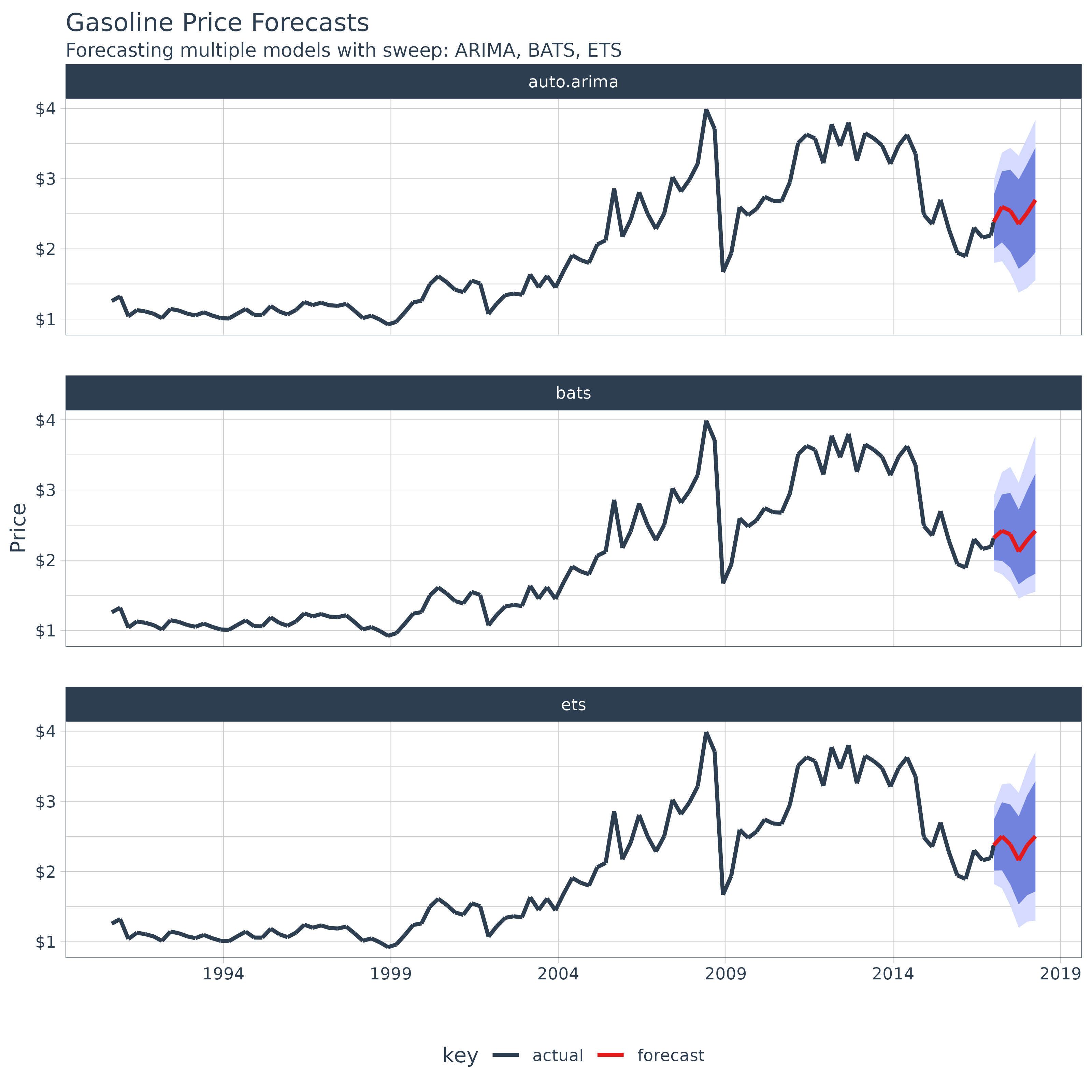

## # ℹ 2 more variables: hi.80 <dbl>, hi.95 <dbl>Finally, we can plot the forecasts by unnesting the “sweep” column

and piping to ggplot().

models_tbl_fcast_tidy %>%

unnest(sweep) %>%

ggplot(aes(x = date, y = price, color = key, group = f)) +

geom_ribbon(aes(ymin = lo.95, ymax = hi.95),

fill = "#D5DBFF", color = NA, linewidth = 0) +

geom_ribbon(aes(ymin = lo.80, ymax = hi.80, fill = key),

fill = "#596DD5", color = NA, linewidth = 0, alpha = 0.8) +

geom_line(linewidth = 1) +

facet_wrap(~f, nrow = 3) +

labs(title = "Bike Sales Revenue Forecasts",

subtitle = "Forecasting multiple models with sweep: ARIMA, BATS, ETS",

x = "", y = "Revenue") +

scale_y_continuous(labels = scales::label_dollar(scale = 1 / 1000000, suffix = "M")) +

scale_x_date(date_breaks = "5 years", date_labels = "%Y") +

theme_tq() +

scale_color_tq()## Warning: Removed 60 rows containing missing values or values outside the scale range

## (`geom_ribbon()`).

## Removed 60 rows containing missing values or values outside the scale range

## (`geom_ribbon()`).